Washington, DC – As the last of the W-2s flood the mailboxes of Americans, two leading consumer groups issued a new report documenting how fast tax refund loans continue to skim over a billion dollars from the pockets of Americans and out of the U.S. Treasury. These loans cost American workers $1.14 billion in loan fees in 2002, plus an additional $406 million in other fees.

The report, entitled “All Drain, No Gain: Refund Anticipation Loans Continue to Sap the Hard-Earned Tax Dollars of Low-Income Americans,” provides an annual update from the National Consumer Law Center and Consumer Federation of America on refund anticipation loans (RALs). About 1 in 10 American taxpayers took out RALs in 2002, over half of them lowwage workers receiving the Earned Income Tax Credit.

The report discusses how a growing recognition of the harm caused by RALs has prompted some state and local governments to pass laws or take action against RALs. “States and cities can and should have a role in preventing RALs,” stated Chi Chi Wu, NCLC attorney. “They can protect their consumers by regulating the tax preparers who broker these usurious loans.” Ms. Wu noted that there is a model statute available from NCLC for those interested in these efforts.

Cost of RALs

RALs are extremely high cost bank loans secured by the taxpayer’s expected tax refund, and that last about 10 days until the IRS refund repays the loan. They cost from $30 to $105 in loan fees and $28 to $59 in “administrative” fees (with an average of $32). Some consumers will also pay an extra $15 to $30 for “instant” products that give them a loan on the same day. This year, a RAL for an average refund of around $2,100 will cost a total of $132 (on top of tax preparation fees averaging $120) and bears an effective annual interest rate (APR) of about 180% (or 240% if administrative fees are included).

The effective APR for a RAL can range from about 70% to over 700% — and if administrative fees are included, the range is 94% to 1,837%. Some tax preparation chains and RAL lenders have been reporting lower APRs by “unbundling” charges from the loan fees. These lower APRs give a less accurate picture of the true “cost of credit” for RALs.

“Banks and tax preparers making quickie tax loans hide their true cost,” criticized Jean Ann Fox, CFA Director of Consumer Protection, “By breaking the cost of a loan into a finance charge, a bank account fee, and administrative fees, then calculating the APR based on only one of these fees, banks and preparers make it difficult to understand what these loans really cost.” RAL volume increased moderately from 2001 to 2002, with approximately 12.7 million RALs taken out during the 2002 tax-filing season, compared to 12.1 million in 2001. H&R Block is still the largest tax preparation chain offering RALs, processing 5.2 million RAL applications in 2002. Household Bank, the largest RAL lender, processed 7 million RALs in 2002. In a victory for consumers, Intuit Corporation discontinued marketing RALs through TurboTax, the nation’s best-selling do-it-yourself tax software program.

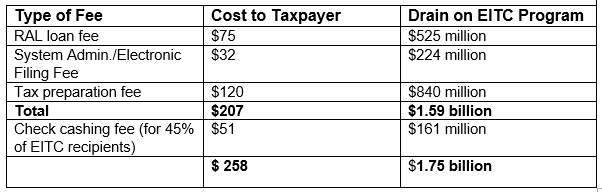

Impact on EITC

The NCLC/CFA report found that over half of consumers, or 55%, who got RALs in 2002 were low-wage workers who received the Earned Income Tax Credit (EITC), even though EITC recipients are only 15% of taxpayers. Seven million working poor families spent $1.75 billion on RAL fees, commercial tax preparation, and (for some of them) check cashing fees, all in order to get their tax refund monies less than two weeks sooner than they could from the IRS. These families paid about $525 million in RAL loan fees, $224 million in administrative fees, and $840 million in tax preparation fees. About 45% of them spent approximately $161 million to cash their RAL checks with check cashers.

Total with check cashing

“Each of these fees undermines the effectiveness of the EITC in supporting low-wage workers,” stated Chi Chi Wu, NCLC attorney, “These fees transfer billions in wealth, paid out of the U.S. Treasury, from working poor families to multi-million dollar corporations.”

Regulatory Action and Inaction

States and cities taking action to protect their consumers from RALs include Illinois, Minnesota, and New York City, all of which passed RAL regulation during the past few years requiring mandatory disclosures about RALs. Regulators in California, Illinois and Oklahoma issued advisories cautioning consumers about RALs. The Massachusetts Commissioner of Banks warned tax preparers that they are required to abide by the Massachusetts small loan cap and obtain a license if they are brokering RALs.

In contrast, the Internal Revenue Service (IRS) continues to tacitly promote RALs under Congressional pressure to have 80% of tax returns filed electronically by 2007. To bolster electronic tax filing, the IRS reduces the risk for RAL lenders by screening loan applicants for tax refund offsets. The IRS for the second year permits commercial preparers to market RALs and other paid products through the IRS Free File program.

Better Disclosures But How Effective?

The NCLC/CFA report noted a bit of progress in the effort to inform consumers of the true nature and costs of RALs. In addition to the new laws requiring mandatory warnings, H &R Block recently announced improved written disclosures, including a cost comparison between RALs and other refund options. The IRS issued a statement that taxpayers are not required to buy RALs sold through its Free File program.

However, disclosure alone is not enough, and the effect of these new disclosures remains to be seen. The report noted there are signs that many consumers remain unaware of the basic fact that RALs are loans. The report includes the results of a small survey of 22 RAL consumers taken in late 2003, in which 18 of the consumers (over 80%) did not realize that they had gotten a loan.

NCLC has produced its own brochure warning consumers about RALs, but improved disclosures do not take the place of substantive protections. The report includes suggestions for protections, such as limiting RAL fees to state usury caps, opening bank accounts for EITC recipients so they can get direct deposit of their refunds, licensing tax preparers, prohibiting tax preparer-fringe financial provider partnerships, and prohibiting RAL lenders from unbundling charges in their interest rate disclosures.

Tax Preparers and High Cost Financial Providers Form New Partnerships

Commercial tax preparation chains have formed new partnerships with high-cost financial service providers, including rent-to-own companies and purveyors of costly stored value cards. The old partnerships with check cashers also appear to be flourishing. In addition, car dealers and payday lenders continue to get their piece of the tax refund pie by preparing taxes and brokering RALs.

Jackson Hewitt, the nation’s second largest tax preparation chain, announced a partnership with Rent-A-Center, the nation’s largest rent-to-own company. Rent-to-own companies are essentially furniture and appliance dealers that offer supposed “leases” masking disguised sales made at astronomical and undisclosed effective interest rates. Jackson Hewitt has also partnered with the Rush Prepaid Visa Card, a stored value card offered by a hip-hop mogul. Stored value cards come with high costs, and the Rush Card appears to be targeted mostly at minority communities.

“Instead of helping their customers open bank accounts to speed up tax refunds without high cost loans, some tax preparers are stranding low-wage workers in the fringe market of check cashers, rent-to-own stores, and stored value cards,” stated Jean Ann Fox, CFA.