Washington, DC – The cost of getting quick cash during tax season went up almost $100 million for consumers last year, according to a new report issued today by two leading consumer groups. The report, “The High Cost of Quick Tax Money: Tax Preparation, ‘Instant Refund’ Loans, and Check Cashing Fees Target the Working Poor,” updates a comprehensive report issued last year on refund anticipation loans (RAL).

Fast tax refund loans cost borrowers from $34.95 to $89.95 in loan fees and about $40 in electronic filing fees for loans that last about ten days. A RAL for the average refund of $1980 bears an annual percent rate (APR) of 222.5%. The APRs for RALs can range from 97.4% to over 2000%, according to a new report issued by Consumer Federation of America and the National Consumer Law Center. The loans are repaid when the consumer’s refund is received in a temporary bank account set up by the lender.

“Quick tax loans cost consumers about $907 million, up almost $100 million from the year before,” Jean Ann Fox, director of consumer protection for CFA, stated. “When you add in the $484 million in electronic filing fees and $400 million in other charges, consumers are paying almost $2 billion just to get their own money faster than the IRS sends it.”

Instant tax loans are marketed by commercial tax preparers and their partner banks. In 2001, about 12.1 million RALs were taken out, up from about 11 million the year before. In 2002, industry leader H&R Block alone made 5.2 million RALs. The report estimates that Household Bank, the largest RAL lender, generated over $225 million in RAL income in 2002.

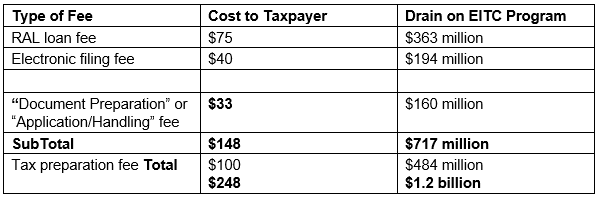

Working poor consumers who qualify for the Earned Income Tax Credit paid about $1.2 billion for commercial tax preparation, electronic filing, RAL fees and other charges to get immediate access to expected refunds, according to the report. The average EITC taxpayer who uses a commercial tax preparer and gets a RAL pays about $250. About 40% of RAL customers receive the EITC, the country’s largest anti-poverty program.

“The EITC is meant to give a boost to hard-working, low-income Americans. Tax preparers and banks are eating away the value of this program, taking money that could be otherwise used to pay bills or build a nest egg for a home or education,” stated Chi Chi Wu, NCLC staff attorney.

Impact on EITC

The report estimates that approximately 4.84 million EITC recipients paid $363 million in RAL loan fees. Tax preparation fees, which are typically about $100, and electronic filing fees added another $678 million to the drain. Adding the extra “document preparation” and “handling” fees, the total drain was $1.2 billion.

Growth in High Cost Tax Refund Financial Products

Tax preparers and their partner banks are promoting “Refund Anticipation Check” or “Refund Transfer” products that cost consumers about $28 just to get their refund from the IRS by way of a “dummy” bank account into which the IRS direct deposits the refund. The taxpayer then picks up a paper check at the tax preparers to receive their money and the bank account is closed. Some tax preparers take their fees for tax preparation out of the refund delivered by these checks, in effect loaning consumers the cost of tax preparation for the ten days it takes for the refund to arrive. Block sold 1.75 million of these last year, while Jackson Hewitt’s bank partner Santa Barbara Bank & Trust earned $14.3 million in gross revenue from refund transfers in 2001.

“As the IRS speeds up tax refunds, the RAL industry is looking for new ways to make money from low-income taxpayers who don’t have bank accounts,” stated Jean Ann Fox, CFA. “Instead of paying for a single-use bank account, taxpayers could have a savings account open for the entire year at about the same price and get their refunds directly from the IRS.”

Check Cashing Fees Surveyed

Check cashers take another bite out of tax refunds and EITC benefits especially for the 45% of EITC recipients who pay for check cashing. CFA member groups surveyed check cashing fees at 143 check cashers in nine states to find out the cost of cashing an IRS refund check, and a RAL check, using a Social Security check as comparison. The average rate to cash an IRS refund check ranged from 1.39% in New York to 4.47% in Arizona. In Florida fees ranged from 1% to 4% of the face value of the IRS refund check. In Virginia, the rates ranged from 3% to 6%. By comparison, the average rate to cash a Social Security check was 2.2%, with a range from 1.4% to 2.88%.

Some surveyed check cashers charged a higher rate to cash refund anticipation loan checks. The average rate for cashing a RAL check ranged from 1.39% in New York to 4.08% in Arizona, with the average rate in the nine states surveyed at 3.08% for RALs.

Paying a check casher takes a big bite out of tax refunds or RALs. The cost of cashing a $2,000 IRS check cost $56.60 on average, or as much as $89.40 at the most expensive check casher surveyed. The cost of cashing a $2,000 RAL check averaged $61.60, but could be as high as $139.80 at the most expensive check casher surveyed in Arizona.

Check Cashers, Payday Lenders, And Used Car Dealers Get a Piece of the Action

Check cashers not only cash RAL or IRS checks, but some of them actually make RALs. Used car dealers also offer RALs to use as down payments on vehicles. A few check cashers and payday lenders not only offer RALs, but have gotten into the business of providing tax services. They provide electronic filing and even appear to be preparing taxes.

Low Income Consumers Need Bank Accounts to Speed Up Refunds

Taxpayers are more likely to pay check cashing fees or buy tax refund check products if they don’t have an account to receive direct deposit from the IRS. The report noted the need for bank accounts as a major factor in helping low-income taxpayers avoid RALs.

“Ten million families do not have bank accounts. Without bank accounts, cashstrapped consumers cannot receive speedy refunds even if they file electronically,” Chi Chi Wu said. “We recommend that consumers open a savings account and go to a free tax preparation center to get help preparing and filing tax returns.”