BOSTON –With the opening of another tax season, consumer advocates at the National Consumer Law Center (NCLC) and Consumer Federation of America (CFA) are warning taxpayers to steer clear of refund anticipation loans (RALs), one of the most avoidable tax-time expenses. New figures reveal that RALs drained the refunds of nearly 9 million American taxpayers in 2006. This figure has declined from a high of 12.4 million in 2004, but still represents $900 million in loan fees, plus over $90 million in other fees. In addition, another 10.8 million taxpayers spent $324 million on other types of financial products to receive their refunds.

In other good news, the price of RALs has declined significantly for some of the biggest players in the industry, introducing new price competition. Even with lower prices, however, consumer advocates urged taxpayers to avoid RALs.

“Taxpayers can save themselves loan fees altogether by just saying ‘no’ to quick refund loans,” advised NCLC Staff Attorney Chi Chi Wu. “Taxpayers shouldn’t forget that these are loans, and they carry the risk of loans, including unmanageable debt if your refund doesn’t arrive as expected.”

RALs Examined

RALs are bank loans secured by the taxpayer’s expected refund — loans that last about 7-14 days until the actual IRS refund repays the loan. That’s the first indicator of just how unnecessary most RALs are: Most taxpayers could have their refund in two weeks or less even without the costly loan.

“For a free quick refund, file electronically and have your refund direct deposited to your own bank account,” says Jean Ann Fox, Director of Financial Services for CFA, “You’ll generally receive an efiled, direct deposit refund within 8 to 15 days.”

Using the most recent data available from the IRS, NCLC and CFA calculate that approximately 9 million taxpayers received RALs in the 2006 tax filing season (for tax year 2005). For that year alone, about 1 in 14 tax returns involved a RAL. Although high, that 9 million figure is much lower than the high of 12.4 million RALs reported for 2004. Part of the 2006 decline, however, is probably due to better reporting. In 2006, the IRS required tax preparers for the first time to separately report RALs versus non-loan refund anticipation check (RACs) products. Thus, prior data may have included RACs that were erroneously reported by tax preparers as RALs.

The IRS data for the first time helps us determine the amount taxpayers paid for RACs. In 2006, nearly 10.8 million taxpayers received a RAC, at a cost of about $324 million. Taxpayers who have a bank account can avoid the expense of a RAC (generally about $30) by having their refunds direct deposited into their account, which is just as fast. In addition, Block customers who received the Emerald Card last year can have their refunds direct deposited onto those cards, and avoid a RAL or RAC.

Price of RALs

The price of a RAL includes several components –

- A loan fee ranging from $32 to $130, which is usually broken down into a “Refund Account” fee and a “Bank Fee.”

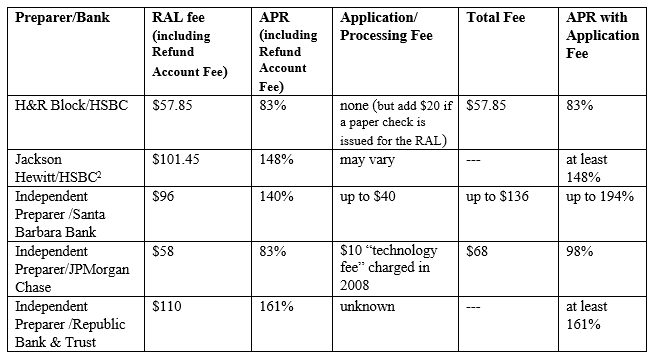

- A separate fee charged by the tax preparer, often called an “application” or “processing” fee, of about $40. This fee is not charged by H&R Block. Jackson Hewitt does not charge the fee in its company-owned stores, but some franchisees might charge a fee.

In general, the effective annual interest rate (APR) for a RAL can range from about 50% to nearly 500%. If application fees are charged and included in the calculation, the effective APRs range from about 80% to nearly 1,200%.

Block and JPMorgan Chase have lowered their RAL fees, claiming that these loans bear an effective APR of 36%, which is the traditional small loan rate cap in many states. However, these figures do not include the “Refund Account” fee, which they claim is for the temporary account into which the taxpayer’s refund is later deposited to repay the RAL. If the Refund Account Fee is included, it more than doubles the APR.

Nonetheless, Block and JPMorgan’s price reductions do represent a real and significant reduction in cost to consumers. For example, a RAL in the amount of $2,600, which is the average refund, costs from $57.85 to $110. Taxpayers should avoid RALs in the first place; but if they insist on getting one, they should shop around.

Tax preparers and their bank partners also offer an “instant” same day RAL for an additional fee, from $25 to $85. Some of the APRs for an instant RAL of about $1,500 are 168% (Block) and 192% (Chase). Santa Barbara Bank & Trust offers an instant RAL of $1,000, which if the taxpayer applies for a “traditional” RAL, may be repaid from the proceeds of the second loan. In that case, the instant RAL could be a 1 day loan that carries an APR of over 1400%.

The IRS Considers Restricting RALs

On January 3, 2008, the IRS issued a request for comments regarding whether it should develop rules restricting the sharing of tax return information to market RALs, RACs, audit insurance and other financial products typically sold to low-income taxpayers. It appears that the IRS has taken a modest, but positive step, toward RAL reform. However, the critical question is whether the IRS will actually take action after receiving comments, and write tough rules governing RALs.

The IRS is accepting comments on the issue until April 7, 2008, so interested parties have a significant opportunity to tell the IRS their thoughts on the issue.

Other Developments

Tax Season Delay

Because Congress was late in enacting its annual “fix” for the Alternative Minimum Tax, taxpayers had been the facing the possibility of a delay in tax season to early February. Fortunately, the IRS announced in late December that tax season would start on time for everyone, except about 13.5 million taxpayers (only 3 to 4 million of whom are early-season filers). The IRS has targeted Feb. 11, 2008 as the potential date for these taxpayers to start filing. For more information, see the National Community Tax Coalition’s website at http://www.tax-coalition.org/newsletter/2008/Tax_Buzz_Jan08.cfm#community.

End to Pay Stub and Holiday RALs

Another positive development on the RAL front is the near total elimination of “pay stub” and “holiday” RALs. These were RALs made prior to the tax filing season, before taxpayers received their IRS Form W-2s and could file their returns. These RALs presented additional costs and risks to taxpayers. NCLC and CFA had issued a report on pay stub RALs and were part of a coalition that called on the Comptroller of the Currency to prohibit national banks from making these loans. During the spring of 2007, all three of the major RAL banks –HSBC, SBBT and JPMorgan Chase — announced they would stop offering these loans.

While pay stub and holiday RALs are essentially gone, H&R Block through its own bank is now offering a credit product to its tax clients, the Emerald Advance Line of Credit. This loan is not explicitly tied to tax preparation, although we assume many borrowers will end up using their tax refund to repay it, since the loan is due in full on February 15. The Emerald Line of Credit carries an interest rate of 36% plus an annual fee of $30, which makes it much less expensive that fringe lending products such as payday or auto title loans.

RALs Off-Limits for Military Service Members

In 2006, Congress enacted the landmark Military Lending Act, protecting active duty Service members from predatory lending. These protections became effective October 1, 2007, under regulations adopted by the Department of Defense. RAL lenders are prohibited from making loans to Service members that cost more than 36% APR. Because the 36% APR cap set by the Military Lending Act is all-inclusive, most RALs exceed that cap when the refund account fees and application fees are included.

NCLC/CFA’s RAL Report from last year documented that tax preparers who market RALs cluster around large military bases. Service members, who almost all have bank accounts and access to free on-base tax preparation assistance, can get fast, direct-deposited tax refunds from the IRS without paying for tax preparation or loan fees.

Advice to Consumers on RALs

Taxpayers tempted by RALs should considered cheaper and better alternatives. For example, both the Volunteer Income Tax Assistance (VITA) program and AARP’s TaxAide offer free tax preparation for low-income taxpayers. The IRS Free File program is available for taxpayers who earn $52,000 or less, and RALs are no longer marketed through that program. (www.irs.gov)

Some of the free tax preparation programs can also help taxpayers open bank accounts, which allow them to take advantage of the speed of a direct-deposited refund using electronic filing. Taxpayers can electronically deposit their tax refunds in up to three accounts with Form 8888. Refunds can be split by depositing into both checking and savings accounts.

In addition to their costs, RALs can be a risky proposition. A RAL must be repaid even if the taxpayer’s refund is denied, is smaller than expected, or frozen. If the taxpayer cannot pay back the RAL, the lender may send the account to a debt collector. The unpaid RAL will also show up as a black mark on the taxpayer’s credit record. If the taxpayer applies for a RAL or RAC from a commercial preparer next year, she may find that her next year’s refund gets grabbed to repay this year’s unpaid RAL debt.

IRS Issues Final Privacy Rule

On January 3, 2008, the IRS issued final rules for tax preparers regarding privacy of their customer’s tax return information. Unfortunately, the IRS rejected recommendations by consumer groups to prohibit tax preparers from trafficking in tax information for cross-marketing purposes. Instead, the newly issued rule, which takes effect January 1, 2009, expands permission for sharing and use of tax return information to third-party companies as well as affiliate entities, so long as preparers get signed consent. Consumer advocates expressed concerns that preparers would easily obtain consent, since the forms would simply be another document in the stack of papers thrust upon taxpayers during the tax preparation session.

Consumer advocates advised taxpayers to watch out for any consent forms that would allow a tax preparer to share or even sell tax return information to marketers. “Don’t unwittingly sign a piece of paper that gives up your most sensitive financial information,” advised Jean Ann Fox of CFA.