BOSTON – As tax season draws to a close, another year has passed in which tax preparers and their partner banks drained hundreds of millions of dollars from refunds by selling refund anticipation loans (RALs), mostly to millions of working families who get the Earned Income Tax Credit (EITC). The National Consumer Law Center (NCLC) and Consumer Federation of America (CFA) issued its annual report today on the RAL industry, entitled “Coming Down: Fewer Refund Anticipation Loans, Lower Prices from Some Providers, But Quickie Tax Refund Loans Still Burden the Working Poor.”

The report reveals that RALs drained the refunds of nearly 9 million American taxpayers in 2006, the last year on which the Internal Revenue Service provided data. The good news is that this figure has declined from a high of 12.4 million in 2004, but it still represents $900 million in loan fees, plus over $90 million in other fees. In addition, another 10.8 million taxpayers spent $324 million on other types of financial products to receive their refunds.

In other good news, both industry giant H&R Block and major RAL lender JP Morgan Chase have lowered their prices significantly. However, other players such as Jackson Hewitt and Republic Bank & Trust still make RALs with triple digit Annual Percentage Rates (APRs). Also, consumer advocates warned that even with lower prices, RALs pose a risk to taxpayers if the IRS denies or holds up their refunds.

“Taxpayers shouldn’t forget that these are loans,” advised NCLC Staff Attorney Chi Chi Wu. “They carry the risk of loans, including unmanageable debt if your refund doesn’t arrive as expected.”

RALs Examined

RALs are bank loans secured by the taxpayer’s expected refund — loans that last about 7-14 days until the actual IRS refund repays the loan. That’s the first indicator of just how unnecessary most RALs are: Most taxpayers could have their refund in two weeks or less even without the costly loan.

“For a free quick refund, file electronically and have your refund direct deposited to your own bank account,” says Jean Ann Fox, Director of Financial Services for CFA, “You’ll generally receive an efiled, direct deposit refund within 8 to 15 days.”

Using the most recent data available from the IRS, NCLC and CFA calculate that approximately 9 million taxpayers received RALs in the 2006 tax filing season (for tax year 2005). For that year alone, about 1 in 14 tax returns involved a RAL. Although high, that 9 million figure is much lower than the high of 12.4 million RALs reported for 2004. Part of the 2006 decline, however, is probably due to better reporting.

In 2006, the IRS required tax preparers for the first time to separately report RALs versus non-loan refund anticipation check (RACs) products.[1] Thus, prior data may have included RACs that were erroneously reported by tax preparers as RALs.

The biggest target for RALs are the low-wage workers who claim the EITC. Nearly two-thirds (63%) of all RAL borrowers in 2006 were EITC recipients, despite the fact that EITC recipients only make up 17% of taxpayers. About 5.7 million working poor families spent over $570 million in RAL fees in order to get their tax refund monies less than two weeks sooner than they otherwise could. Administrative or application fees added another $57 million to the drain.

The IRS data for the first time helps us determine the amount taxpayers paid for RACs. In 2006, nearly 10.8 million taxpayers received a RAC, at a cost of about $324 million. Taxpayers who have a bank account could have avoided the expense of a RAC (generally about $30) by having their refunds direct deposited into their account, which is just as fast. In addition, Block customers who received the Emerald Card last year could have had their refunds direct deposited onto those cards, and avoid a RAL or RAC.

Price of RALs

The price of a RAL includes several components –

- A loan fee ranging from $32 to $130, which is usually broken down into a “Refund Account” fee and a “Bank Fee.”

- A separate fee charged by the tax preparer, often called an “application” or “processing” fee, of about $40. This fee is not charged by H&R Block. Jackson Hewitt does not charge the fee in its company-owned stores, but some franchisees might charge a fee.

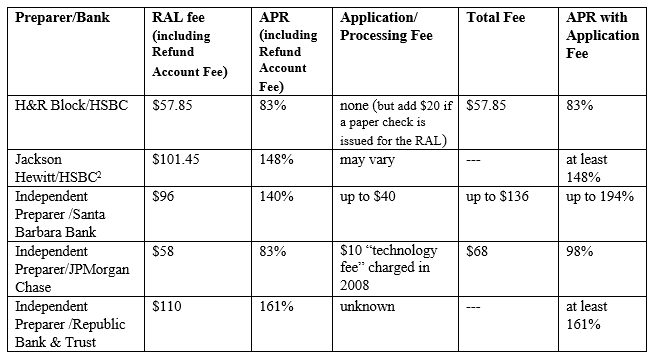

In general, the effective APR for a RAL can range from about 50% to nearly 500%. If application fees are charged and included in the calculation, the effective APRs range from about 80% to nearly 1,200%.

Block and JPMorgan Chase have lowered their RAL fees, claiming that these loans bear an effective APR of 36%, which is the traditional small loan rate cap in many states. However, these figures do not include the “Refund Account” fee, which they claim is for the temporary account into which the taxpayer’s refund is later deposited to repay the RAL. If the Refund Account Fee is included, it more than doubles the APR.

Nonetheless, Block and JPMorgan’s price reductions do represent a real and significant reduction in cost to consumers. For example, a RAL in the amount of $2,600, which is the average refund, costs from $57.85 to $110. Taxpayers should avoid RALs in the first place; but if they insist on getting one, they should shop around.

Tax preparers and their bank partners also offer an “instant” same day RAL for an additional fee, from $25 to $85. Some of the APRs for an instant RAL of about $1,500 are 168% (Block) and 192% (Chase). Santa Barbara Bank & Trust offers an instant RAL of $1,000, which if the taxpayer applies for a “traditional” RAL, may be repaid from the proceeds of the second loan. In that case, the instant RAL could be a 1 day loan that carries an APR of over 1400%.

The IRS Considers Restricting RALs

In January 2008, the IRS issued a request for comments regarding whether it should develop a rule restricting the sharing of tax return information to market RALs, RACs, audit insurance and other financial products typically sold to low-income taxpayers. A rule prohibiting information sharing could significantly hamper RAL lending and reduce the number of loans.

The IRS is specifically asking for feedback on two points: 1) Whether letting tax preparers share tax return information to sell RALs and other products provides an incentive to inflate tax refunds and 2) whether RALs and similar products exploit taxpayers. It appears that the IRS has taken a modest, but positive step, toward RAL reform. However, the critical question is whether the IRS will actually take action after receiving comments, and write tough rules governing RALs.

The IRS is accepting comments on the issue until April 7, 2008, so interested parties have a significant opportunity to tell the IRS their thoughts on the issue.

Other Developments

End to Pay Stub and Holiday RALs

Another positive development on the RAL front is the near total elimination of “pay stub” and “holiday” RALs. These were RALs made prior to the tax filing season, before taxpayers received their IRS Form W-2s and could file their returns. These RALs presented additional costs and risks to taxpayers. NCLC and CFA had issued a report on pay stub RALs and were part of a coalition that called on the Comptroller of the Currency to prohibit national banks from making these loans. During the spring of 2007, all three of the major RAL banks –HSBC, SBBT and JPMorgan Chase — announced they would stop offering these loans.

While pay stub and holiday RALs are essentially gone, H&R Block through its own bank is now offering a credit product prior to tax season to its tax clients, the Emerald Advance Line of Credit. This loan is not explicitly tied to tax preparation, although we assume many borrowers ended up using their tax refund to repay it, since the loans were due in full on February 15. The Emerald Line of Credit carries an interest rate of 36% plus an annual fee of $30, which makes it much less expensive than fringe lending products such as payday or auto title loans.

RALs Off-Limits for Military Service Members

In 2006, Congress enacted the landmark Military Lending Act, protecting active duty Service members from predatory lending. These protections became effective October 1, 2007, under regulations adopted by the Department of Defense. RAL lenders are prohibited from making loans to Service members that cost more than 36% APR. Because the 36% APR cap set by the Military Lending Act is all-inclusive, most RALs exceed that cap when the refund account fees and application fees are included. H&R Block is the sole exception, with a “military RAL” that is truly 36% APR.

NCLC/CFA’s RAL Report from last year documented that tax preparers who market RALs cluster around large military bases. Service members, who almost all have bank accounts and access to free on-base tax preparation assistance, can get fast, direct-deposited tax refunds from the IRS without paying for tax preparation or loan fees.

Government Enforcement Actions

RALs have attracted a great deal of scrutiny by federal and state enforcement agencies. The U.S. Department of Justice sued five Jackson Hewitt franchisees that operated 125 offices for their role in preparing fraudulent tax returns that falsely claimed $70 million in tax refunds; RALs were heavily promoted in those offices. The California Attorney General filed lawsuits against Jackson Hewitt and Liberty Tax Service over their promotion of RALs. Jackson Hewitt settled with the Attorney General, promising reforms of its practices and paying $4 million in consumer refunds plus $1 million in penalties and costs. The New Jersey Attorney General’s Office sued a local tax preparation chain, Malqui Corporation, for deceptive advertisement of RALs. The New York State Division of Human Rights sued both Jackson Hewitt and Liberty Tax Service for discriminatory targeting of minorities for RALs, in violation of New York Human Rights Law.