BOSTON – Some of America’s most cash-strapped taxpayers – those from low- and moderate-income families – spent about $900 million in the latest year recorded for what is almost always an unnecessary product: the so-called “refund anticipation loan” at income tax time.

With the opening of another tax season, consumer advocates at the National Consumer Law Center (NCLC) and Consumer Federation of America (CFA) are warning taxpayers to steer clear of refund anticipation loans (RALs), one of the most avoidable tax-time expenses. New figures reveal that RALs drained the refunds of 8.67 million American taxpayers in 2007, costing them $833 million in loan fees, plus over $68 million in other fees. In addition, another 11.2 million taxpayers spent $336 million on related financial products to receive their refunds.

“In tough economic times, quick money may be tempting. But American taxpayers need every dollar of their refunds, and waiting just a week or two will put more money in their pockets,” advised NCLC Staff Attorney Chi Chi Wu.

RALs Examined

RALs are bank loans secured by the taxpayer’s expected refund — loans that last about 7-14 days until the actual IRS refund repays the loan. That’s a good indication of just how needless most RALs are: Most taxpayers could have their refund in two weeks or less even without the costly loan.

“If you want your refund fast, file electronically and have your refund direct deposited to your own bank account,” says Jean Ann Fox, Director of Financial Services for CFA, “You’ll generally receive your refund this way within 8 to 15 days.”

Using the most recent data available from the IRS, NCLC and CFA calculate that about 8.67 million taxpayers received RALs in the 2007 tax filing season (for tax year 2006). For that year alone, about 1 in 15 tax returns involved a RAL.

In addition, 11.2 million taxpayers received a refund anticipation check (RAC)[1] in 2007, at a cost of about $336 million. Taxpayers who have a bank account can avoid the expense of a RAC (generally about $30) by having their refunds direct deposited into their account, which is just as fast. H&R Block customers who received the Block Emerald Card in a prior year can have their refunds direct deposited onto those cards, and avoid a RAL or RAC.

Price of RALs

How much will taxpayers pay if they get a quickie tax loan? The price of a RAL includes several components –

- A loan fee ranging from $34 to $130, which is usually broken down into a “Refund Account” fee and a “Bank Fee.”

- Some tax preparers may charge one or more separate add-on fees, sometimes called “application,” “administrative,” “e-filing,” “service bureau,” “transmission,” or “processing” fees. Add-on fees can range from $25 to several hundred dollars. Add-on fees are not charged by H&R Block, Jackson Hewitt or Liberty Tax.

In general, the effective annual interest rate (APR) for a RAL can range from about 50% to nearly 500%. If a $40 add-on fee is charged and included in the calculation, the effective APRs range from about 85% to nearly 1,300%.

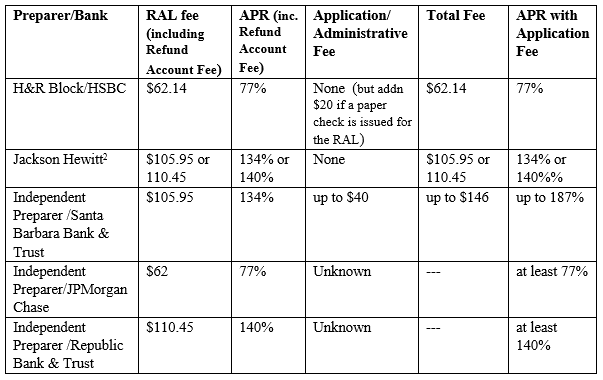

RAL loan fees can vary significantly. H&R Block and JPMorgan Chase generally have lower RAL fees. In fact, they claim that these loans bear an effective APR of 36%, which is the traditional small loan rate cap in many states. However, these figures do not include the “Refund Account” fee, which they claim is for the temporary account into which the taxpayer’s refund is later deposited to repay the RAL. If the Refund Account Fee is included, it more than doubles the APR.

Nonetheless, there are some real and significant price differences between various RAL outlets. For example, a RAL in the amount of $3,000, which is typical, costs from $62 to $110. Taxpayers should avoid RALs in the first place; but if they insist on getting one, they should shop around for RAL costs before selecting a commercial preparer.

Tax preparers and their bank partners also offer an “instant” same day RAL for an additional fee, from $25 to $55. Some of the APRs for an instant RAL of around $1,500 are 185% (Block) and 211% (Chase).

Finally, consumers who do not use one of the commercial chains should also ask if the preparer charges any add-on fees. Mystery shopper testing conducted during the 2008 tax season revealed that some independent preparers charge several add-on fees for both RALs and RACs. One preparer charged $324 in add-on fees; several others charged $45. Santa Barbara Bank & Trust allegedly limits tax preparers to $40 in add-on fees; however, the preparer that charged $324 in add-on fees used Santa Barbara as its lender.

Return of the Pay Stub RAL

Last year, we reported the demise of “pay stub” and “holiday” RALs. These were RALs made prior to the tax filing season, before taxpayers received their IRS Form W-2s and could file their returns. Unfortunately, this demise was short-lived. Both H&R Block and Jackson Hewitt are promoting loans made before the tax season based on anticipated refunds.

Jackson Hewitt’s version is called the iPower Line of Credit, up to $500, issued by MetaBank. MetaBank charges a 1.5% fee for the first advance from the line, and a 10% charge per advance thereafter, plus 18% periodic interest. If a taxpayer borrows the entire $500 in the first advance, she would be charged a $57.65 fee. If the iPower loan is repaid in one month, the total fee would be $65.15. A one month, closed-end loan with the same loan amount and fee would have an APR of 177%.

H&R Block’s version uses its Emerald Advance Line of Credit. This is a line of credit that Block had offered previously to its Emerald Card customers, and is available for some customers on a year-round basis, for up to $1,000. This year, however, Block explicitly promoted the Emerald Advance as a taxrelated pre-season loan and made it available to new customers. The Emerald Line of Credit carries an interest rate of 36% plus an annual fee of $45. For a $500 advance repaid in one month, the total fee is $60. A one month, closed-end loan with the same loan amount and fee would have an APR of 158%, if the annual fee were to be included in the finance charge (which Truth in Lending does not require). If however, the borrower keeps the line open after tax season, the interest rate is lowered to 9%, but requires either payroll direct deposit to Block’s Emerald Card or a savings account linked to the card.

RALs based on pay stubs present risks to taxpayers, because they are based on estimated tax returns before the taxpayer receives final tax information from a W-2. For example, before filing the tax return, the preparer will not have any information if the IRS is planning to seize all or part of the taxpayer’s refund to pay a child support or student loan debt. H&R Block does state that it conducts underwriting for its loans based on considerations other than the estimated refunds.

In addition, Jackson Hewitt in the past appeared to force pay stub RAL borrowers to return to the same office to have their taxes prepared, preventing these taxpayers from going to competitors or seeking free volunteer assistance. The MetaBank agreement appears to assume the taxpayer will return to Jackson Hewitt for tax preparation and requires the borrower to have her RAL, RAC or tax refund loaded onto the iPower card. In addition, Jackson Hewitt may be charging a $25 or $35 “tax planning fee” for iPower loans.

[1] With RACs, the bank opens a temporary bank account into which the IRS direct deposits the refund check. After the refund is deposited, the bank issues the consumer a check and closes the temporary account. Also, if a taxpayer’s RAL application is rejected, she is automatically given a RAC at a cost of $30 or so, even though the taxpayer may not have asked for it.