Without access to mortgages, homeownership would be out of reach for most people. The American invention of the 30-year mortgage has made homeownership possible for millions of families. But even today, mortgage credit is not equally available everywhere.

In lower-income rural communities, where good jobs are scarce and credit scores are low, families often struggle to qualify for a mortgage. And in housing markets where many real-estate investors are active, even pre-approved homebuyers lose out to cash offers. Mortgages also remain hard to get for homes priced under $150,000, for fixer-upper properties, and for manufactured housing. As a result, mortgage access is uneven across communities, shaping exclusion and unequal opportunities.

In lower-income rural communities, where good jobs are scarce and credit scores are low, families often struggle to qualify for a mortgage. And in housing markets where many real-estate investors are active, even pre-approved homebuyers lose out to cash offers. Mortgages also remain hard to get for homes priced under $150,000, for fixer-upper properties, and for manufactured housing. As a result, mortgage access is uneven across communities, shaping exclusion and unequal opportunities.

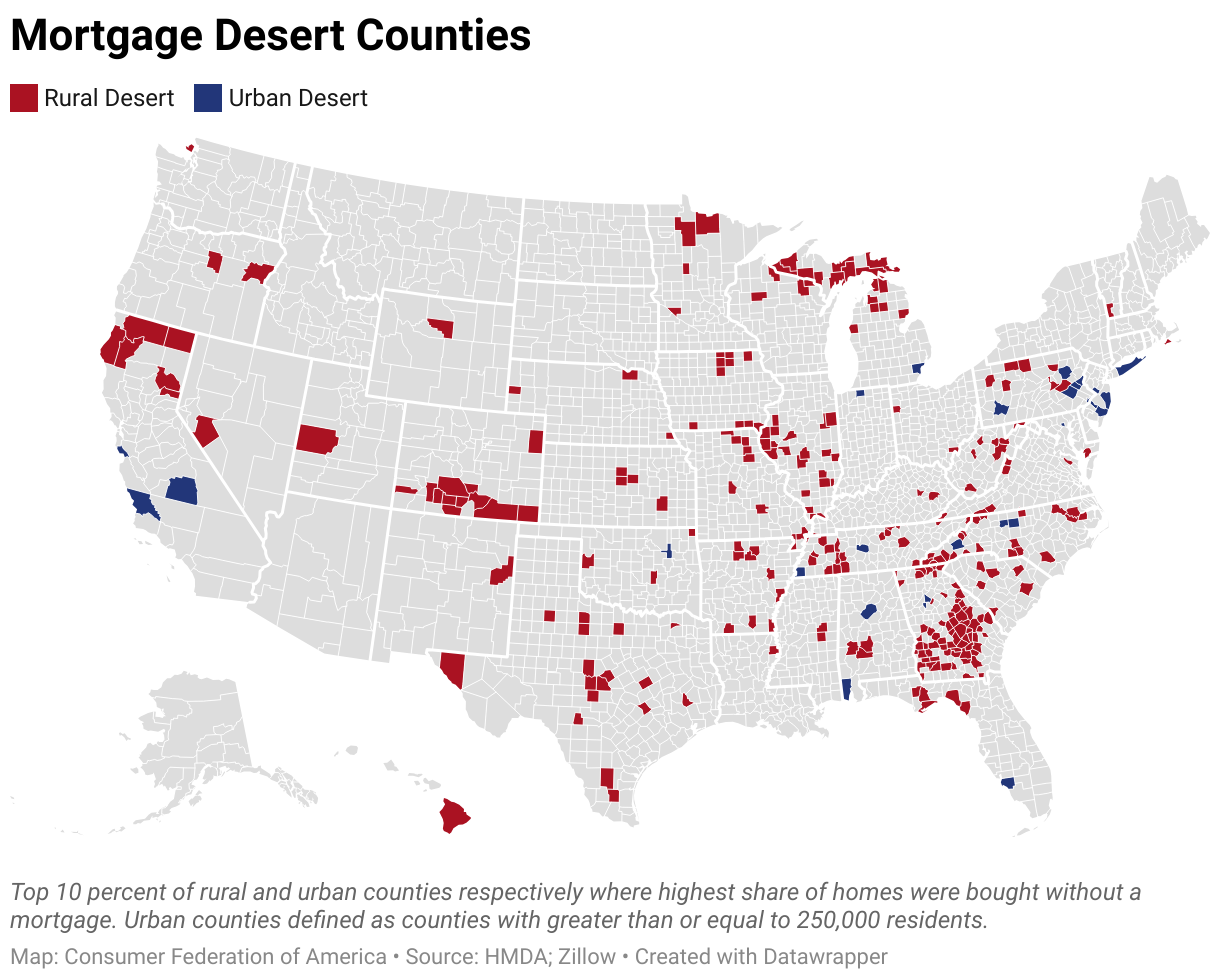

This report introduces the new idea of “mortgage deserts,” which are places where relatively few homes are purchased with a mortgage. Mortgage deserts are defined as the bottom ten percent of rural areas and the bottom

ten percent of urban areas nationwide where the lowest shares of homes are bought with a mortgage. Mortgages remain scarce in these communities, even as people still buy and sell homes.

This report answers three key questions:

1. In what U.S. counties are few homes bought with a mortgage?

2. Why are mortgages rarer in these rural and urban communities?

3. What can policymakers do to expand financing access and better support homeownership in mortgage deserts?