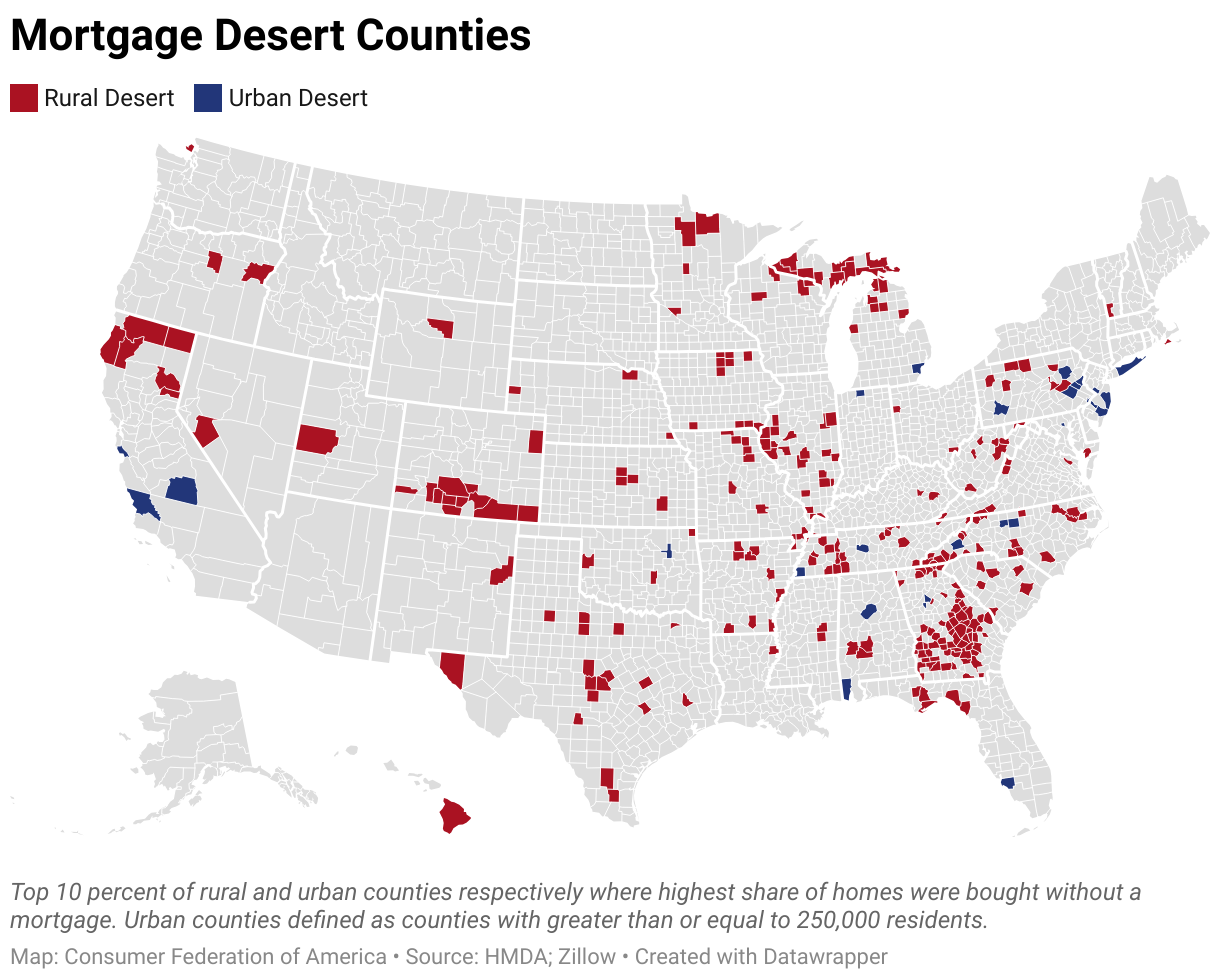

WASHINGTON, D.C. – A new report from the Consumer Federation of America, Mortgage Deserts: Mapping Which Rural and Urban Communities Remain Left Behind by Mortgage Finance, shows that despite decades of federal policy efforts to reach historically excluded and underserved housing markets, mortgage access and use remains deeply uneven across the country. Mortgage deserts, as established by this report, describe the bottom ten percent of urban counties and the bottom ten percent of rural counties nationwide, where the greatest share of homes are bought without a mortgage. The report found mortgage deserts exist throughout the country and are most often located in rural and urban disinvested communities, with low household incomes and a higher-than-average share of Black residents.

“Mortgages remain scarce in too many places: a modern-day redlining that has very real consequences for people and communities,” said Sharon Cornelissen, Director of Housing and author of the report. “From rural Georgia to rural Texas and from Baltimore to Detroit, without mortgages, families cannot become homeowners, cash investors have free reign, and communities struggle to build wealth.”

While journalists have invoked the idea of mortgage deserts before, it has never been studied and mapped. This report analyzed data on all originated home purchase mortgages in 2022 and 2023 using Home Mortgage Disclosure Act (HMDA) data, alongside data from Zillow on total number of home sales.

In doing so, the report found Black residents make up twice the share of the population in rural mortgage deserts compared to other rural areas (15 percent vs. 7 percent), and a larger share in urban mortgage deserts than in other urban communities (21 percent vs. 13 percent). States with the most rural mortgage deserts include Georgia, North Carolina, Tennessee, and Illinois. Meanwhile, Baltimore city and Clayton County in suburban Atlanta are our nation’s most excluded urban mortgage deserts: half of all homes (49%) are sold without a mortgage. The report also finds that in some parts of rural Georgia, over 7 in 10 homes are bought without a mortgage, while in some Detroit neighborhoods, mortgages remain an anomaly even as hundreds of homes are bought and sold.

“The evidence has been clear through many generations that Georgia’s rural residents, especially among Black families, are excluded from the wealth-building advantages that come with homes acquired through mortgages,” said Liz Coyle, Executive Director of the consumer advocacy nonprofit, Georgia Watch. “Having the data and analysis to confirm this reality will make a real difference in our ability to pursue policy solutions for the people in our state.”

Like the ideas of food deserts and banking deserts, mortgage deserts reveal where mortgages are underused or unavailable, even in places where homes still exchange hands and where banks may be present.

To tackle the problem of mortgage deserts, the report offers the following policy recommendations:

- Fannie Mae, Freddie Mac, and the Federal Home Loan Banks should expand access to small-dollar mortgages, which are mortgages smaller than $150,000.

- Federal and state lawmakers should direct investments to housing repair programs and mortgage financing for fixer-upper homes.

- Federal and state policymakers, and the Consumer Financial Protection Bureau (CFPB), should expand consumer protections on “mortgage-alternative” sources of financing, such as land contracts and rent-to-own agreements.