Washington, D.C. — At a time of both rising interest rates and rising purchases of adjustable rate mortgages (ARMs), a new survey commissioned by the Consumer Federation of America (CFA) suggests that lower-income and minority consumers are particularly vulnerable to the risks of these ARMs. The survey of 1015 representative adult Americans, undertaken earlier this month, reveals that lower-income and minority consumers are most likely to prefer ARMs yet misunderstand the interest rate risks of these mortgage loans.

The same survey, however, also revealed that a large majority of Americans, if they were going to purchase a home in the next month, would prefer a fixed rate mortgage (FRM). And, the reasons these consumers cited for preferring FRMs to ARMs suggest that they are very aware of the interest rate risks of ARMs, even those with a fixed rate for seven years that then converts to an adjustable rate.

“The good news is that about two-thirds of Americans not only prefer fixed rate mortgages but appear well-aware of the risks of ARMs,” said CFA Executive Director Stephen Brobeck. “The bad news is that lower-income and minority Americans are not only those most likely to prefer ARMS but also those with the poorest understanding of their risks,” he added.

Historically, ARMs were the most likely to be purchased by affluent consumers who could afford mortgage interest rate increases. But recently, ARMs, which are now the choice of more than 30 percent of mortgage purchasers, are being marketed by some lenders to all potential buyers, regardless of income or assets. More disturbingly, according to one report, subprime borrowers are more than twice as likely as those with high credit scores to purchase ARMs.

“Lenders who aggressively market ARMs to lower-income consumers and those with low credit scores are acting irresponsibly,” said Brobeck. “Given the high probability of interest rate increases, an adjustable rate loan made to a family which can barely afford the initial monthly payments represents a ticking time bomb,” he added.

The consumer survey was conducted for CFA by Opinion Research Corporation International on July 8-11, 2004. Its margin of error is plus or minus three percentage points.

Most Americans Prefer Fixed Rate Mortgages and Do So Because of Predictable Payments and No Downside Risk

To the question, “if you were going to purchase a home in the next month with a 30-year mortgage, which of the following types of mortgage would you prefer?”, 64 percent said one with a fixed rate for the entire term while only 25 percent said an adjustable rate mortgage or 7- year hybrid loan (fixed for 7 years then adjustable after that). (Eleven percent said none of these or didn’t know.)

Moreover, those preferring FRMs were quite clear about the reasons for their preference.

- For 92 percent, “the security of knowing how much my mortgage payments will be throughout the terms of the mortgage” is “very important.”

- For 88 percent, “with an ARM, I would be concerned that mortgage interest rates would rise, and I would end up paying more in interest” is “very important.”

- For 81 percent, “with an ARM, I would be concerned that mortgage interest rates would rise, and I would not be able to afford higher monthly payments” is “very important.”

Some experts believe that fixed rate mortgages are most likely to be preferred by the least affluent and sophisticated consumers. The CFA survey suggests that this is not the case. Fixed rate mortgages are preferred by 76 percent of those with incomes over $75,000, by 70 percent of college graduates, and by 75 percent of those between the ages of 45 and 64.

“Some economists chide consumers for preferring ‘overpriced’ fixed rate mortgage loans to ARMs,” said Brobeck. “But those consumers currently favoring FRMs probably do so because of their awareness of not only the likelihood of rising interest rates but also the huge potential downside risk of interest rate hikes — unaffordable mortgage payments, insolvency, and foreclosure,” he added.

Americans Who Prefer ARMs Are the Least Likely to Understand These Loans and Tolerate Their Risks

The 25 percent of Americans who say they prefer ARMs are younger, poorer, and less well-educated than those who prefer FRMs.

- 32 percent of those 18-24 years of age, but only 19 percent of those 45-64, prefer ARMs.

- 33 percent of those with incomes under $25,000, but only 20 percent of those with incomes over $50,000, prefer ARMs.

- 26 percent of those with only a high school degree, but only 21% of college grads, prefer ARMs.

In addition, 37 percent of Hispanics and 31 percent of African-Americans, but only 23 percent of whites, prefer ARMs.

The fact that Americans with the least experience in the marketplace and the least education are most likely to prefer ARMs suggests that lack of financial knowledge is associated with preference for ARMs. This hypothesis is reinforced by other data from the survey.

First, those preferring ARMs seem less clear about the reasons for their preference than do those preferring FRMs. Fewer than one-half of those favoring ARMs said any of the following reasons was “very important” — don’t think interest rates will rise much, would be likely to keep the loan for less than seven years so aren’t worried about rate hikes, and could afford a larger mortgage.

Second, those preferring ARMs are much less aware of the interest rate risks than are those preferring FRMs. All respondents were asked to estimate the annual increase in mortgage payments if the 6 percent interest rate on a $200,000, 30-year ARM — with annual payments of $14,400 — rose by two percentage points to 8 percent.

- A far higher percentage of young adults aged 18-24 (46 percent), Hispanics and African-Americans (43 percent), those with incomes under $25,000 (44 percent), and those without a high school degree (50 percent), than of all Americans (35 percent), could not estimate an increase (they said they “don’t know”).

- The members of these groups who gave a figure underestimated the increased cost far more than other Americans. Compared to an actual annual increase in payments of $3210, Hispanics said $1594 (average of their estimates), young adults said $1964, the poor said $1963, and those with no high school degrees said $1964 (though African-Americans said $2661). That is, these groups underestimated the actual increase in payments by about 40-50 percent. By comparison, all respondents (including these 3 groups) estimated an increase of $2248, an underestimate of only about 30 percent.

- One important reason for this disparity is, because members of these groups are less likely than the rest of the population to have ever purchased a home, they have not had as much experience with home mortgages.

Third, young adults, Hispanics, the poor, and the least educated are most attracted to highly risky interest-only mortgage loans, whose payments rise rapidly after 3-5 years when interest begins to be charged. When asked if this interest-only loan would be more attractive than other mortgage options, 27 percent of young adults (18-24), 30 percent of Hispanics, 24 percent of moderate income Americans ($25k-$35k), and 28 percent of those with no high school degree, but only 17 percent of all Americans, said yes.

Consumers Urged to Use Caution in Purchasing ARMs

Before purchasing an ARM, consumers should carefully analyze their own present and likely future financial condition, and the impact of rising mortgage payments on this condition. The assessment of their financial condition should not be done with the assistance of someone who has an interest in selling them a home or a mortgage. It should be done independently or with the assistance of an independent financial expert.

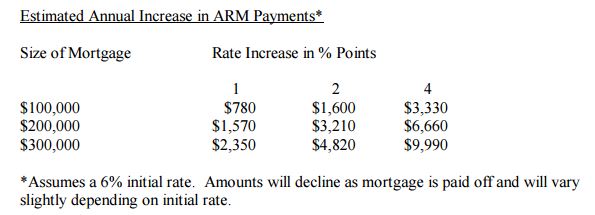

The financial impact of rising rates can be assessed with the aid of the following table, which indicates the change in annual mortgage payments resulting from different interest rate increases.

While some ARMs cap interest increases at 2 percentage points annually and 5 percentage points for the life of the mortgage, other ARMs do not. Thus, annual increases in mortgage payments could exceed $10,000.

“Who can say that, in the next decade or two, there will not be another world economic crisis, like the 1970s Arab oil embargo, which drove interest rates up over 10 percent,” said Brobeck. “And, if this occurs, there will certainly be homeowners who refinance to fixed rates much too late or not at all,” he added.

If consumers plan to pay off their mortgage completely in the first five years or so, either because they move or they want debt-free homeownership, then the financial risks of ARMs to them are much lower.

Lenders Urged to Use Caution in Selling ARMs

CFA urges lenders not to market ARMs to consumers with low incomes, low wealth, or low credit scores. CFA also urges lenders to clearly disclose to ARM purchasers the financial impacts of future interest rate increases. They should be taking into account not only borrowers’ ability to pay under the initial rate but also under the maximum payments allowed, should rates rise. Finally, CFA urges those purchasing securitized ARMs — GSEs and investors — to carefully consider the risks of purchasing ARMs held by high credit-risks.

“In a rising interest rate environment, investors should be particularly leery of purchasing subprime adjustable rate mortgages,” said Brobeck. “These high-priced ARMs have the potential to harm investors as well as borrowers,” he added.

Contact: Jack Gillis, 202-737-0766

CFA is a non-profit association of some 300 consumer groups which seeks to advance the consumer interest through research, education, and advocacy.