Washington, D.C. – The Consumer Federation of America (CFA) and the Center for Economic Justice (CEJ) called on insurers and insurance regulators to provide ongoing auto premium relief as auto claims remain up to 50% below normal levels due to the COVID-19 pandemic and related restrictions. The groups have monitored auto crashes in Texas and Massachusetts since March and continue to find that fewer miles driven translates into fewer auto accidents – but this hasn’t in turn translated into premium relief for many consumers.

“People are still out of work, staying home, and driving less,” said J. Robert Hunter, CFA’s Director of Insurance and former Texas Insurance Commissioner. “By failing to return the excess premiums that policyholders continue to pay, insurance companies are racking up huge unearned windfall profits while Americans are facing both financial devastation and a growing health crisis, while being in a state of general uncertainty.”

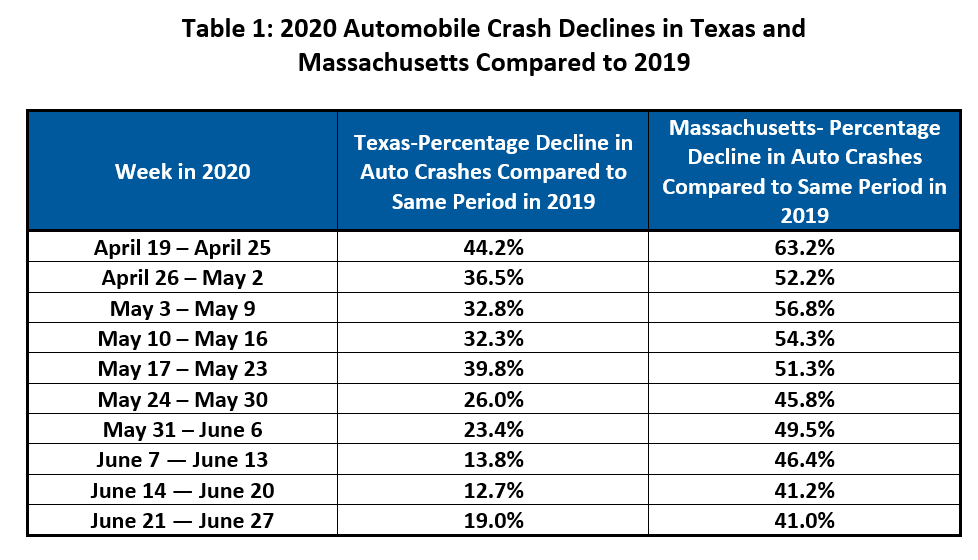

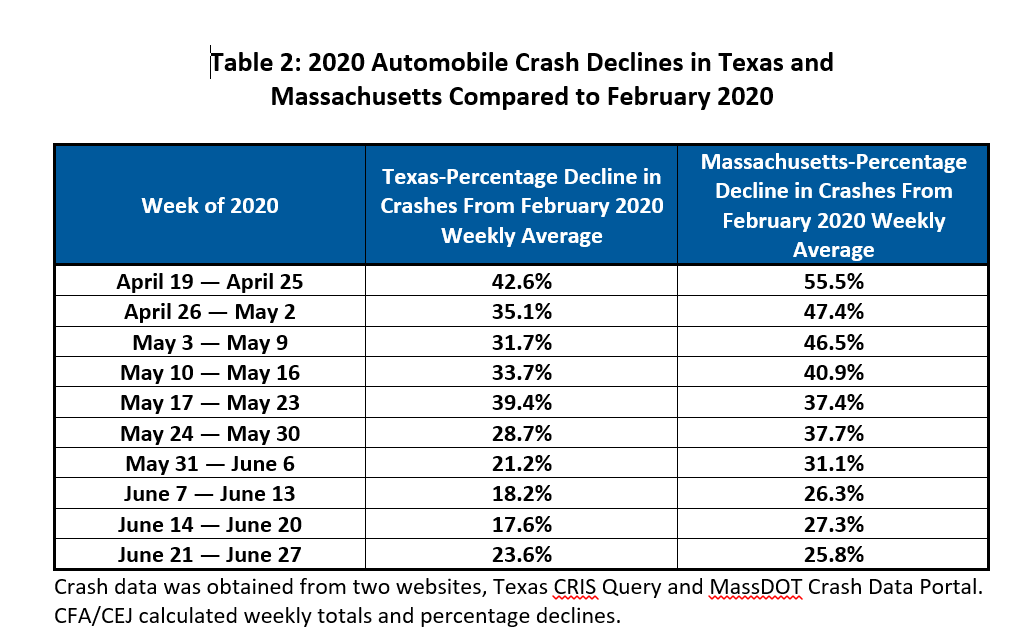

Building on their previous report, CFA and CEJ have monitored and analyzed crash data from various states’ Departments of Transportation. Tables 1 and 2 below show the results for Texas and Massachusetts. In both states, there was an increase in the frequency of accidents in June relative to the spring, but crashes are still floating between about 12% and 50% below June 2019, which is well outside of the range of any normal fluctuation and clearly indicates that drivers’ premiums remain excessive.

In mid-March, CFA and CEJ wrote to insurance regulators warning about windfall pandemic profits for auto insurers if regulators failed to act to protect consumers. While a couple of states took action to order premium relief, most state insurance commissioners took no action. As predicted, auto insurers are now reporting windfall profits. For example, Allstate reported a $1 billion reduction in claims for the second quarter of 2020 compared to the same period in 2019, despite an increase in vehicles insured and premiums. Its second quarter profits were $1.22 billion, compared to $821 million in the second quarter of 2019. And Progressive reported profits of $2.268 billion for the second quarter of 2020 compared to $1.243 billion for the second quarter of 2019.

Texas Department of Insurance Earns Its Place in the Hall of Shame

In Texas, a coalition of community groups wrote to Commissioner Kent Sullivan asking why the Texas Department of Insurance (TDI) had taken no action on auto premium relief. In response, the Department wrote, “We cannot determine an excessive long-term profit on a month by month basis with incomplete information.”

“The lack of action by Texas – and many other states – to protect consumers from excessive auto insurance premiums is inexplicable,” said Birny Birnbaum, Director of CEJ. “The Texas Insurance Commissioner seems to be the only person in Texas without the information needed for premium relief. The data on crash reductions and the actions by some insurers to provide premium relief would lead anyone who cared about consumers to take the types of actions that the Commissioners of California and Michigan have taken. It is cruel to tell consumers who need and deserve auto premium relief now that they have to wait for many months for TDI to get ‘complete’ data.”

California, Michigan, New Jersey, and New Mexico Insurance Commissioners Have Stepped Up

Only California, Michigan, New Jersey, and New Mexico have ordered insurers to make refunds during the spring due to the pandemic. California extended its order through June and required companies to make ongoing refunds should the reduced accident frequency persist. Texas’s failure to take action is especially inexcusable, given the ongoing decline in crashes and the persistence of the pandemic there. The Commissioner’s negligence reflects a profound misunderstanding of both rate standards and the current situation for consumers.

After Promising Start with Premium Relief for April and May, Most Insurers are Now Pocketing their COVID Windfalls

Although a few auto insurers have voluntarily continued their refund programs beyond May 31st, most companies have not. Table 3 details the refund programs the nation’s largest insurers have implemented since the COVID-19 pandemic began to close down the country in March.

The fact that insurers are reporting unfair, excessive profits in the second quarter of 2020 despite making paybacks shows that CFA/CEJ were right when they indicated in earlier releases that the March, April and May paybacks were too small. “We indicated that the paybacks of about $12 billion in the second quarter were too low and should be doubled, but most regulators did nothing, handing insurers about a $12 billion windfall in March, April and May at the expense of their constituents, many of whom were unemployed or otherwise financially stressed. Since May the windfall situation has gotten even worse,” said Hunter.

“Unfortunately, many insurance companies seem to think they did enough when they gave back a portion of the excess premium they collected this spring,” said CFA’s insurance expert Doug Heller. “But this pandemic persists across the country. The same reasons that made refunds necessary in the spring have continued into the summer, and state insurance commissioners should order insurers to return more premium rather than leave companies with another coronavirus windfall.”