Washington, D.C. – Insurers selling personal auto insurance reaped windfall profits of at least $29 billion in 2020 as miles driven, vehicle crashes and auto insurance claims dropped because of the pandemic and related government actions. Analyzing insurers’ 2020 premium and claims results – and the limited “premium relief” offered by insurers – the Consumer Federation of America (CFA) and Center for Economic Justice (CEJ) show that insurers collected $42 billion in excess premiums while providing only $13 billion in “premium relief.”[1] Instead of returning the COVID windfall to consumers, insurers increased payouts to senior management and stockholders.

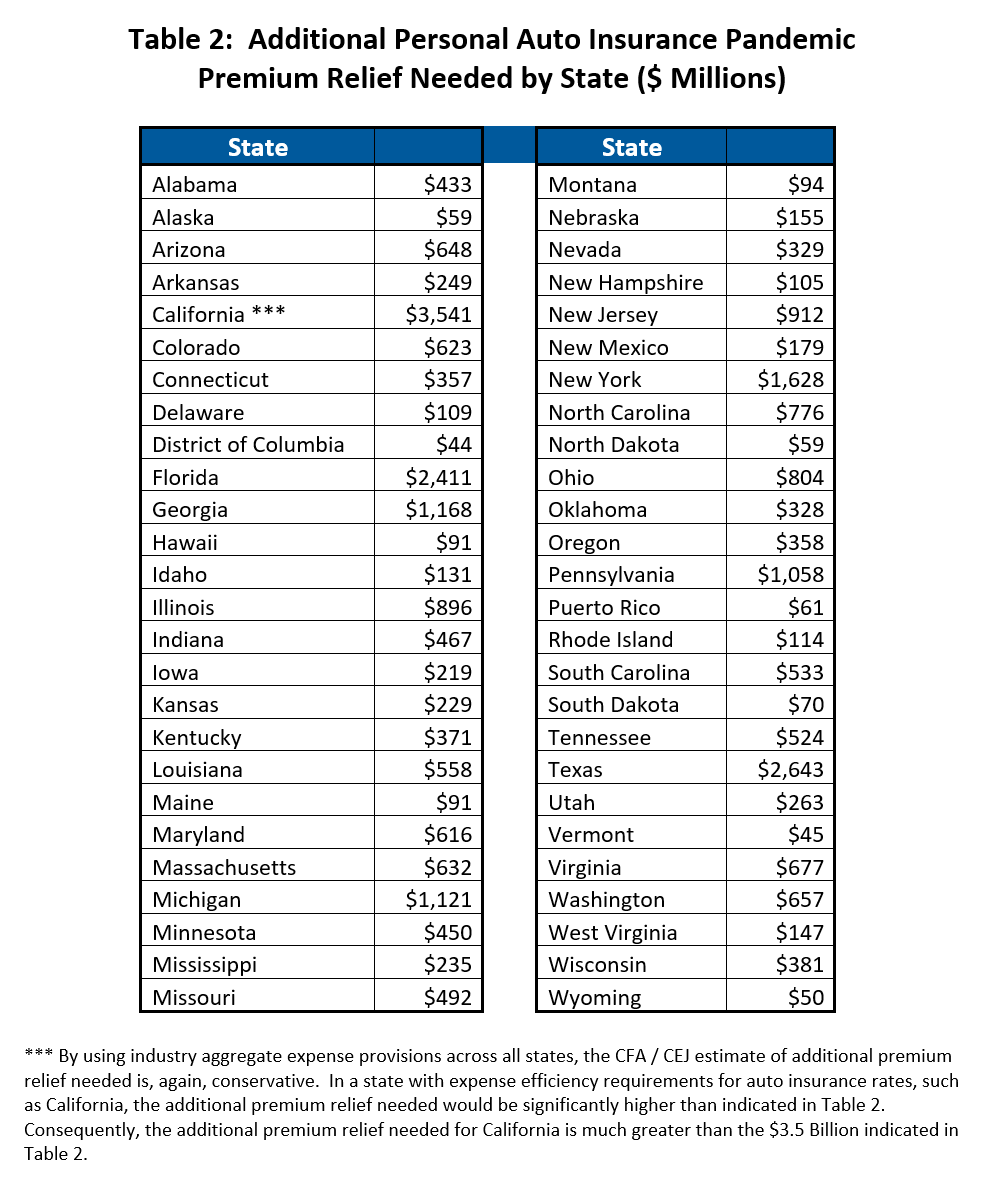

State-by-state required additional auto insurance pandemic relief is itemized in Table 2 attached to this release.

Despite analyses and warnings from CFA and CEJ starting in March 2020, when it was clear that the reduction in driving had made then-current insurance prices excessive – and in violation of the law in almost every state – the vast majority of insurance regulators took no action to compel insurers to return the illegal profits. Relying on insurers’ financial statement data for premiums and losses and additional analysis by A.M. Best regarding insurers’ “premium relief,” CFA and CEJ show insurers should have returned $42 billion of premium overcharges to consumers, but actually returned just one-third of that amount.

“In virtually every state, auto insurance premiums – by law – cannot be excessive. The inability or unwillingness of almost all state insurance regulators to enforce the law and protect consumers raises serious questions,” said J. Robert Hunter, CFA’s Director of Insurance. “As we pointed out in letter after letter to insurance regulators throughout 2020, it was crystal clear that insurers’ premium relief was woefully inadequate. The attached document lists, with links and thumbnail descriptions, all of the letters and press releases we issued urging states to take action to reduce illegally excessive auto premiums in their jurisdictions.”

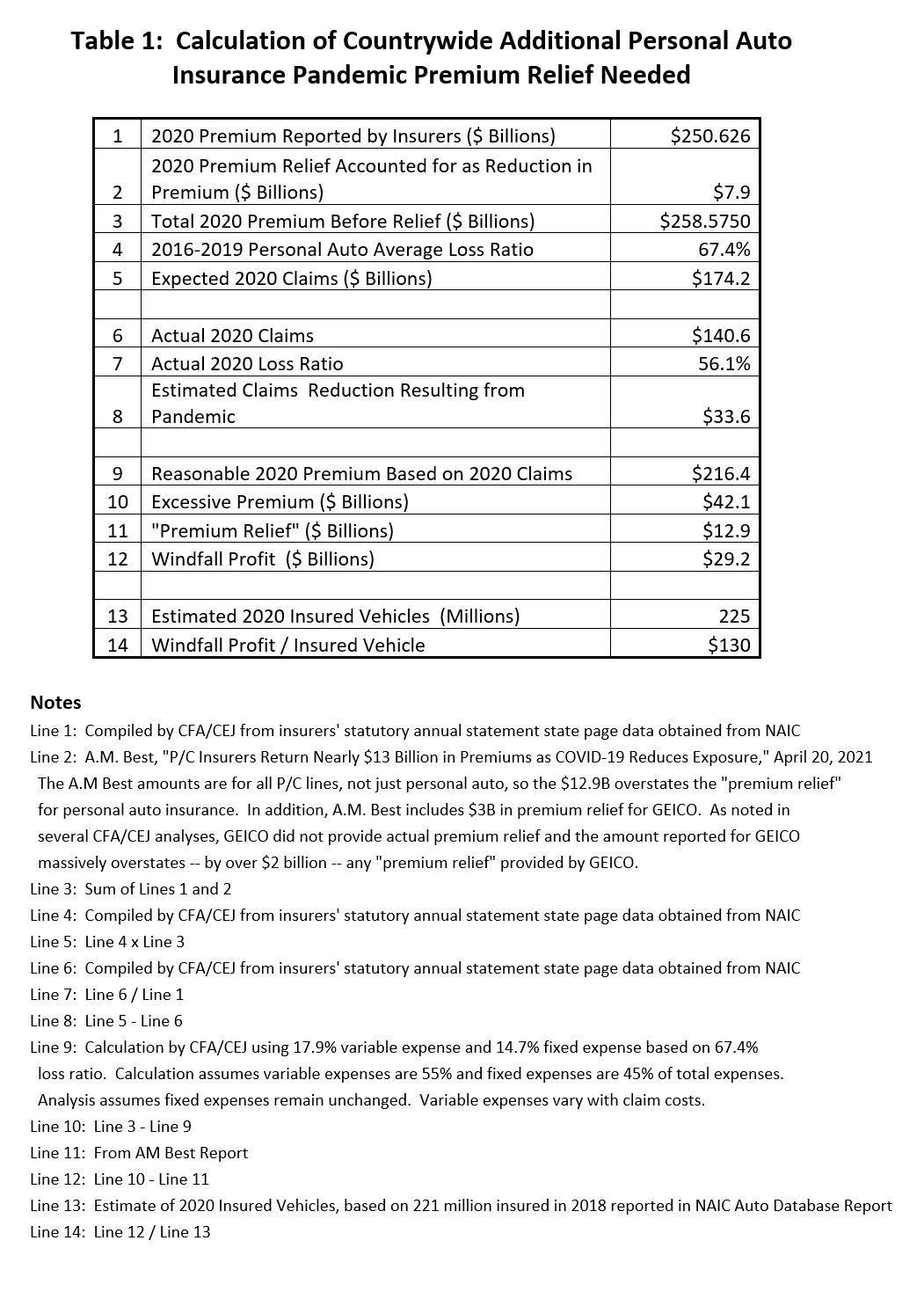

According to the insurers’ financial reports reviewed by CFA and CEJ, between 2016 and 2019, auto insurers paid 67.4 cents of every premium dollar for claims. The remaining 32.6 cents – plus investment income earned from holding policyholders’ money – covered insurer expenses and profit. In 2020, the amount spent on claims dropped to 56.1 cents per dollar of total premium reported. Total premium of $250.6 billion reported by insurers is net of $7.9 billion in premium relief accounted for by some insurers as a reduction in premium.

Table 1 shows that from 2016 through 2019, insurers paid 67.4 cents of every premium dollar for claims. But claim payouts in 2020 were just 56.1 cents per net premium dollar – or $33.6 billion less than if insurers had continued to pay 67.4 cents in claims per dollar in premium. To provide some perspective, a reduction in claim payments of $33.6 billion is a per-vehicle reduction in claims of about $150.

Table 1 shows that the $33.6 billion reduction in claim payouts by insurers translates into $42.1 billion of excess premium charges out of a total of about $258.6 billion in total personal auto insurance premium.[2] Yet, according to A.M. Best, insurers returned just $13 billion in premium relief[3] – less than one-third of their pandemic windfall – while pocketing the remaining two-thirds. As a result, insurers shortchanged policyholders by an average of over $125 premium per insured vehicle.

State Insurance Commissioners Have Statutory Responsibility to Protect Consumers from Excessive Auto Insurance Premiums – But Most Failed to Act

As a result of the sudden change in exposure covered by auto insurance, premiums became excessive virtually overnight in mid-March 2020. However, most regulators did not take – and have still not taken — action to require the necessary premium relief from auto insurers. Table 2 shows the additional premium relief needed in each state.[4]

In April and May of 2020, most of the nation’s large insurers did provide refunds or credits to consumers in response to the pandemic, but very little of the excess premium was given back after last spring and our research showed that even this two-month payback to policyholders was only about half of what should have been refunded.[5]

California, Michigan, New Jersey, and New Mexico were the only states to require premium refunds during the spring of 2020. But only California continued requiring refunds beyond the first few months of the pandemic. In March 2021, California’s Insurance Commissioner Ricardo Lara determined that auto insurers still overcharged California drivers during the pandemic and ordered them to return additional premium to consumers. In June and July, respectively, Washington State and New Mexico announced industry data calls about auto insurance losses during the pandemic that will hopefully lead to additional premium refunds for consumers, but other regulators have not taken initial steps, let alone further steps, to recoup money for drivers by enforcing their states’ laws against excessive rates..

In addition to little or no action by most states, there has been no action at the National Association of Insurance Commissioners (NAIC) to examine the issue of auto insurers’ pandemic windfall profits, to collect data during 2020 to monitor the situation or to develop guidance for states to bring needed relief to consumers – again despite repeated calls by CFA and CEJ.

As the NAIC conducts its national meeting this week, CFA and CEJ call on state insurance regulators to take action to address the $30 billion overcharge to auto insurance consumers. This news release has been sent to the President and other top officials of the NAIC urging them to act immediately to begin the process of returning pandemic premium overcharges to customers.

CFA AND CEJ LETTERS AND RELEASES CALLING ON STATE REGULATORS TO ENFORCE THEIR LAWS FORBIDDING EXCESSIVE RATES DURING COVID-19

March 18, 2020 letter to Commissioners: “We write to urge you to direct auto insurers in your state to provide premium offset payments to policyholders whose driving has been affected by COVID-19.” https://consumerfed.org/wp-content/uploads/2020/03/COVID-19-Auto-Premium-Relief-Letter.pdf

March 30, 2020 letter to Commissioners: “We urge you to take action on key P&C insurance consumer protection issues arising from COVID-19 and federal and local government responses to the pandemic, particularly the excessive premiums being charged to individuals and businesses for lines of insurance that base rates on factors such as miles driven, payroll, and receipts.” https://consumerfed.org/wp-content/uploads/2020/03/COVID-19-Auto-Premium-Relief-Letter-3-30-20.pdf

April 6, 2020 Press Release: After praising Allstate and American Family for their shelter-in-place paybacks, “The groups noted that they had sent a letter to state insurance commissioners on March 18 urging the regulators to act to get industry wide premium relief for auto insurance consumers – and have seen virtually no action to date other than suggestions to insurers by the insurance commissioners in Alaska and Pennsylvania. https://consumerfed.org/press_release/consumer-groups-applaud-allstates-and-american-familys-shelter-in-place-paybacks-urge-other-auto-insurers-to-follow/

April 13, 2020 Press Release: Issued a Report Card on insurer actions in granting paybacks due to COVID. The release said: “Given that hundreds of millions of Americans pay for auto insurance and spend more on auto insurance than any other type of insurance other than health insurance – $250 billion in 2019 – we are puzzled by the lack of activity to date by insurance commissioners.” “There is still a need for the regulators to step up, as critical guidance for current and future relief is needed,” said CEJ’s Birny Birnbaum, Executive Director of the Center for Economic Justice. https://consumerfed.org/press_release/report-card-to-date-on-the-6-5-billion-promised-to-auto-insurance-customers-as-people-drive-less-due-to-covid-19/

April 23, 2020 Press Release updating the payback situation. “For those insurers providing premium relief, the relief ranges from just over 10% to 35% of two months premium with the vast majority of insurers providing only 15%. With some data showing motor vehicle accidents down 50% or more, more relief is needed for March, April and May from nearly all insurers,” said Douglas Heller, CFA’s Insurance Expert. “It’s clear that premium relief of 30% or more will be needed for these months.” But we also pointed out the failure of state regulators to act. https://consumerfed.org/press_release/auto-insurance-premium-relief-update-more-insurers-to-return-premium-as-refunds-and-credits-top-7-billion-through-may/

On May 7, 2020, CFA and CEJ issued a letter to all Commissioners, “Auto Insurance Premiums are Excessive in Your State.” The letter stated, “Consumer Federation of America and the Center for Economic Justice just released a major report detailing the current situation in auto insurance in America and the fact that, throughout every state in the country, consumers are still paying excessive premiums even after the recent voluntary relief granted by most auto insurance companies.” https://consumerfed.org/wp-content/uploads/2020/05/COVID-19-Auto-Premium-Relief-Letter-5-7-20.pdf The report attached to the letter, “Personal Auto Insurance Premium Relief in the COVID-19 Era” made clear that “State insurance regulators have largely been absent from personal auto insurance relief and the state auto insurance regulatory system has proven to be unprepared for an event like COVID- 19…Motor vehicle accident data indicate a minimum average 30% premium relief payment starting March 18, 2020 through the end of May, even after accounting for offsetting cost factors.” https://consumerfed.org/wp-content/uploads/2021/07/Auto-Insurance-Refunds-COVID-19-Update-Report-5-7-20.pdf

On May 21, 2020, we sent a letter to all Commissioners, “More State Action Needed to Address Excessive Auto Insurance rates. In it we pointed out that “other than the commissioners in California and New Jersey, no other state regulators have ordered insurers to provide any relief, let alone a minimum amount of relief… Whatever the cause of this regulatory inaction to date, consumers need – and your statutory duties demand – action now.” https://consumerfed.org/wp-content/uploads/2020/05/Auto-Insurance-Commissioner-Letter.pdf

On May 26, 2020, our Press Release stated, “While commissioners in California and New Jersey have ordered premium relief and are collecting data to ensure relief is adequate, most state insurance regulators have done nothing to secure auto insurance premium relief, even as they have often inappropriately taken credit for insurers’ actions. The inaction by state insurance regulators has particularly harmed those low-income and minority consumers forced to purchase insurance from so-called “non-standard” carriers.” https://consumerfed.org/press_release/allstate-and-usaa-show-how-insurers-should-provide-ongoing-covid-19-premium-relief/

In a June 25, 2020 letter to all Commissioners we said, “Our review of company announcements indicates that many insurers who offered premium relief for April and May are not continuing to offer relief for June and beyond – despite the reduction in miles driven and crashes from the levels assumed for rates in effect on March 1. It is no less urgent for you to take action now as it was in mid-March to meet your statutory requirements to ensure consumers do not pay excessive premiums.” https://consumerfed.org/testimonial/consumer-groups-urge-insurance-commissioners-to-follow-californias-lead-on-insurance-premium-refunds/

On July 15, 2020 we specifically called on Arizona and Texas to extend the paybacks beyond the insurer’s voluntary paybacks of April and May 2020. https://consumerfed.org/wp-content/uploads/2020/07/Arizona-Insurance-Commissioner-Letter-7-15-20.pdf https://consumerfed.org/wp-content/uploads/2020/07/Texas-Insurance-Commissioner-Letter-7-23-20.pdf

On August 6, 2020, we issued a Press Release, “Consumers Still Being Overcharged for Auto Insurance as Pandemic Continues to Reduce Claims.” We said, “While a couple of states took action to order premium relief, most state insurance commissioners took no action. As predicted, auto insurers are now reporting windfall profits.” https://consumerfed.org/press_release/consumers-still-being-overcharged-for-auto-insurance-as-the-pandemic-continues-to-reduce-claims/

On August 11, 2020 our Press Release pointed out that GEICO was pocketing windfall auto insurance profits on billions of dollars from COVID. We said, “According to CFA and CEJ, state insurance commissioners need to do more to ensure that auto insurers return more of their excess income to their policyholders and former customers. At this time California, New Mexico, Michigan and New Jersey are the only states requiring auto insurers to return pandemic-driven excess premium to customers.” https://consumerfed.org/press_release/consumer-advocates-call-on-geico-to-give-back-much-more-after-2-1-billion-earnings-bonanza-due-to-covid-19-pandemic-impacts/

On September 21, 2020, we again wrote to all Commissioners in which we said: “The pandemic has shown once again how systemic racism permeates personal auto insurance and penalizes minority consumers. Millions of Americans are currently struggling and facing economic hardship, whether due to unemployment, reduced hours and wages, business closures, or a decline in business activity. This makes it all the more important that you ensure that the insurance companies you monitor and regulate are returning consumers’ excess premium on an ongoing basis.” https://consumerfed.org/wp-content/uploads/2020/09/COVID-19-Auto-Premium-Relief.pdf

September 22, 2020 Press Release subtitled, “Insurance Commissioners are Asleep at the Wheel When It Comes to Putting this Money Back in Consumer Pocketbooks Where It Belongs.” https://consumerfed.org/press_release/auto-insurers-reap-tens-of-billions-in-covid-windfall-profits-due-to-reduction-in-miles-driven-and-crashes/

December 22, 2020 letter to all Commissioners, “Extremely High Insurer Profits and New Accident Data Show that Auto Insurance Companies Need to Provide More Pandemic Refunds; Your Constituents are Suffering by Your Inaction.” We stated: “With the economic pain that has accompanied this pandemic, the fact that most Insurance Commissioners allowed insurers to set the terms for refunds and have not ordered more has been a failure of leadership. But action on behalf of consumers today is still much better than none at all.” https://consumerfed.org/wp-content/uploads/2020/12/Auto-Insurance-Commissioner-Letter.pdf

March 11, 2021 Press Release, “California Insurance Department Ends Auto Insurers’ COVID Windfall Profits; Consumer Groups Ask Why Other States Don’t Keep Insurance Companies from Raiding Consumer Pocketbooks with their Windfall COVID Profits.” “Consumers rely on their state insurance commissioners to protect them from being ripped off by insurers, but most have let auto insurers collect massive windfall profits, while the millions of Americans struggled through the pandemic,” said CEJ Executive Director Birny Birnbaum. https://consumerfed.org/press_release/california-insurance-department-ends-auto-insurers-covid-windfall-profits/

[1] See Table 1 for analysis, methodology and data sources. The “premium relief” amounts come from the insurer rating agency A.M. Best in an April 20, 2021 report. A.M. Best compiled the “premium relief” from statutory financial statements in which insurers self-reported the amount of “premium relief.” The $13 billion of “premium relief” reported by A.M. Best includes $3 billion in claimed “premium relief” from GEICO. In fact, GEICO never paid any premium relief to existing policyholders. Rather, GEICO promised a 15% reduction upon renewal and even to new customers – an action which simply reflected lower expected claims in the future. GEICO never provided premium relief to consumers who paid premium for March, April or May 2020. In contrast, State Farm provided real premium relief though policyholder dividends to offset premiums paid by policyholders in March, April and May, 2020. State Farm also filed a prospective rate reduction in expectation of lower claims in the future which averaged nationally was 11%. Despite GEICO not providing any premium relief, we included all the amounts reported in the A.M. Best analysis, including GEICO.

[2] The $250.626 Billion in reported earned premium after premium relief plus $7.949 Billion in premium relief treated by insurers as a reduction in premium equals $258.575 Billion

[3] A portion of the $13 billion in refunds was provided to policyholders with coverage other than personal auto insurance, but Best’s does not break out the refunds by line, so our calculation likely overstates the personal auto premium relief provided by insurers and understates the additional relief due for policyholders.

[4] By using industry aggregate expense provisions across all states, the CFA / CEJ estimate of additional premium relief needed is, again, conservative. In a state with expense efficiency requirements for auto insurance rates, such as California, the additional premium relief needed would be significantly higher than indicated in Table 2. Consequently, the additional premium relief needed for California is much greater than the $3.5 Billion indicated in Table 2.

[5] “Personal Auto Insurance Premium Relief in the COVID-19 Era: A Report By the Center for Economic Justice and the Consumer Federation of America.” Center for Economic Justice and Consumer Federation of America. May 2020. Available at https://consumerfed.org/wp-content/uploads/2021/07/Auto-Insurance-Refunds-COVID-19-Update-Report-5-7-20.pdf.

Contacts:

Robert Hunter, CFA, 703-528-0062

Birny Birnbaum, CEJ, 512-912-1327

Michael DeLong, CFA, 925-708-1135