Report Card to Date on the $6.5 Billion+ Promised To Auto Insurance Customers as People Drive Less Due To COVID-19

Washington, D.C. – Companies that sell more than 82 percent of the auto insurance in America have announced that they will be refunding or crediting drivers more than $6.5 billion over the next two months. The payments reflect the insurers’ savings from far fewer-than-anticipated auto insurance claims because of the radical reduction in cars on the road and miles driven due to Stay at Home orders and other COVID-19 precautions that have dramatically changed Americans’ daily lives.

Consumer Federation of America (CFA) and Center for Economic Justice (CEJ) first called on insurers and state insurance regulators to ensure this type of relief in letters to Commissioners sent on March 18 and March 30. Today, we thank those insurers who have taken action to make payments to consumers. We also provide a detailed assessment of the various insurer approaches to relief and outline a path for ensuring fairness over the coming months, with particular emphasis on the role of state insurance regulators.

As CFA and CEJ wrote on March 18, the premium pay-backs are reasonable and necessary to account for insurance rates that suddenly became excessive because assumptions about miles driven and claim frequency became obsolete once consumers were told to stay home and businesses were shuttered. Without such refunds, insurers would be charging excessive premiums in two ways.

- First, consumers whose premiums were based on driving 1,000 miles a month, but who are now driving 100 miles a month, for example, should get a lower premium because of that individual’s reduced risk exposure.

- Second, and the basis for the insurer refunds, is that overall insurance rates became excessive when the actual number of auto accidents dropped by 50% or more virtually overnight. Rates for all policyholders became excessive regardless of any individual’s change in driving.

“We applaud the many insurance companies that have recognized that they cannot sit on policyholder premium while their customers sit at home,” said J. Robert Hunter, Director of Insurance for CFA and former Texas Insurance Commissioner. “But consumers might need double this amount to balance how much they pay with how much they drive this year. We expect companies and commissioners to help make this right as Americans struggle through this crisis.”

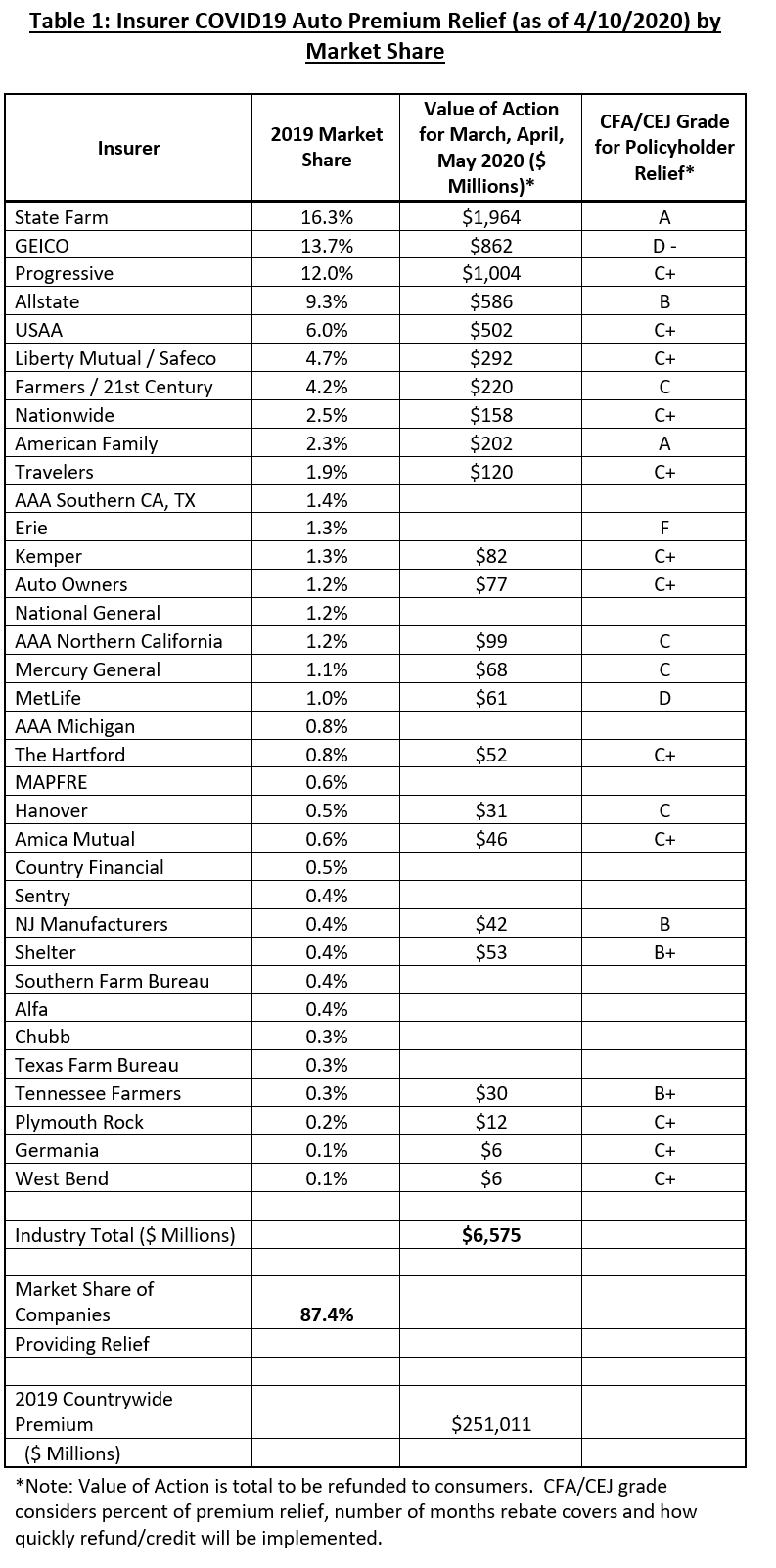

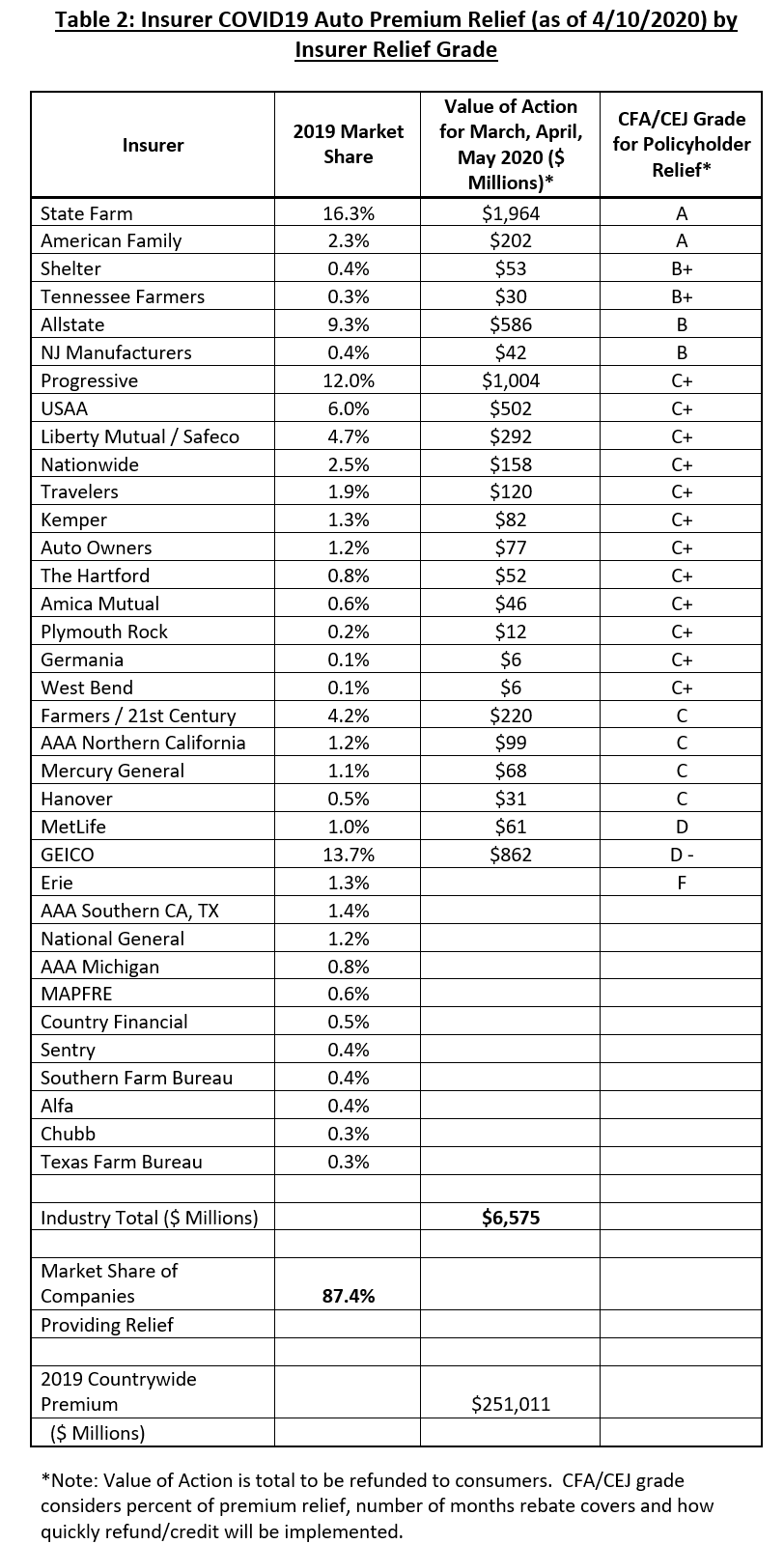

While most of the 35 largest insurers have announced some amount of refunds, credits, or reductions to account for COVID-19 changes, some have not made such promises as of Sunday April 12 at 3:00 pm ET. Those who have not offered meaningful relief include most regional Auto Clubs affiliated with AAA (only CSAA of Northern California has promised relief), National General, Mapfre, Country Financial, and Sentry. Additionally, Erie has promised a future rate cut but nothing to account for the current changes their customers have had to make. Table 1 details the relief provided or promised by each of the nation’s 35 largest auto insurers.

Grading the Refunds

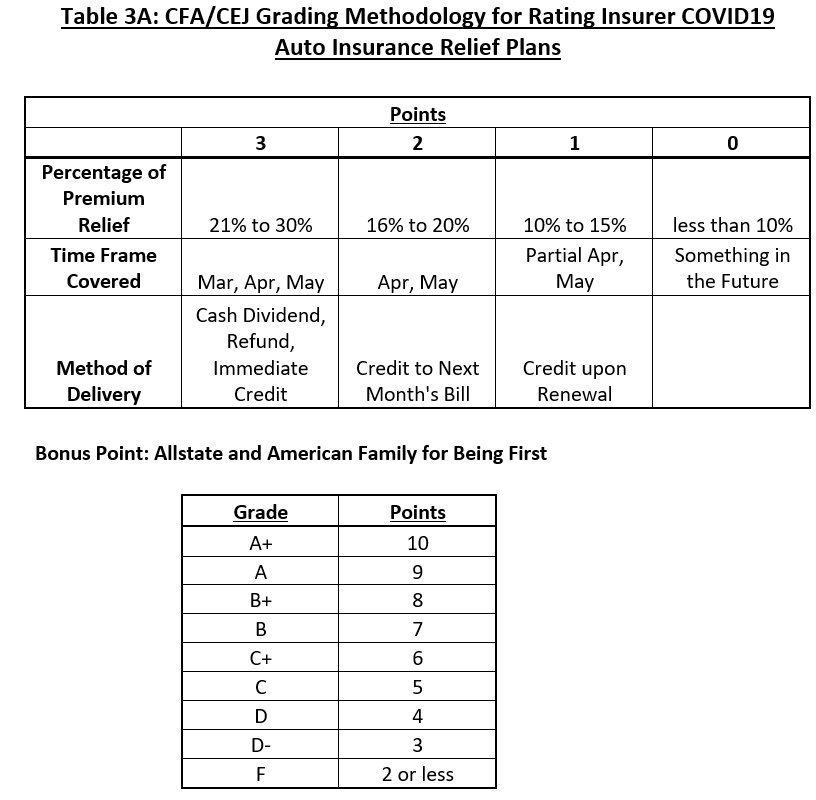

CFA and CEJ have evaluated each of the companies’ refunds according to a three-part assessment, with three possible points for each part, which is fully detailed in Table 3A:

- Amount of premium relief

- Time frame covered by relief

- Method of delivery of the relief

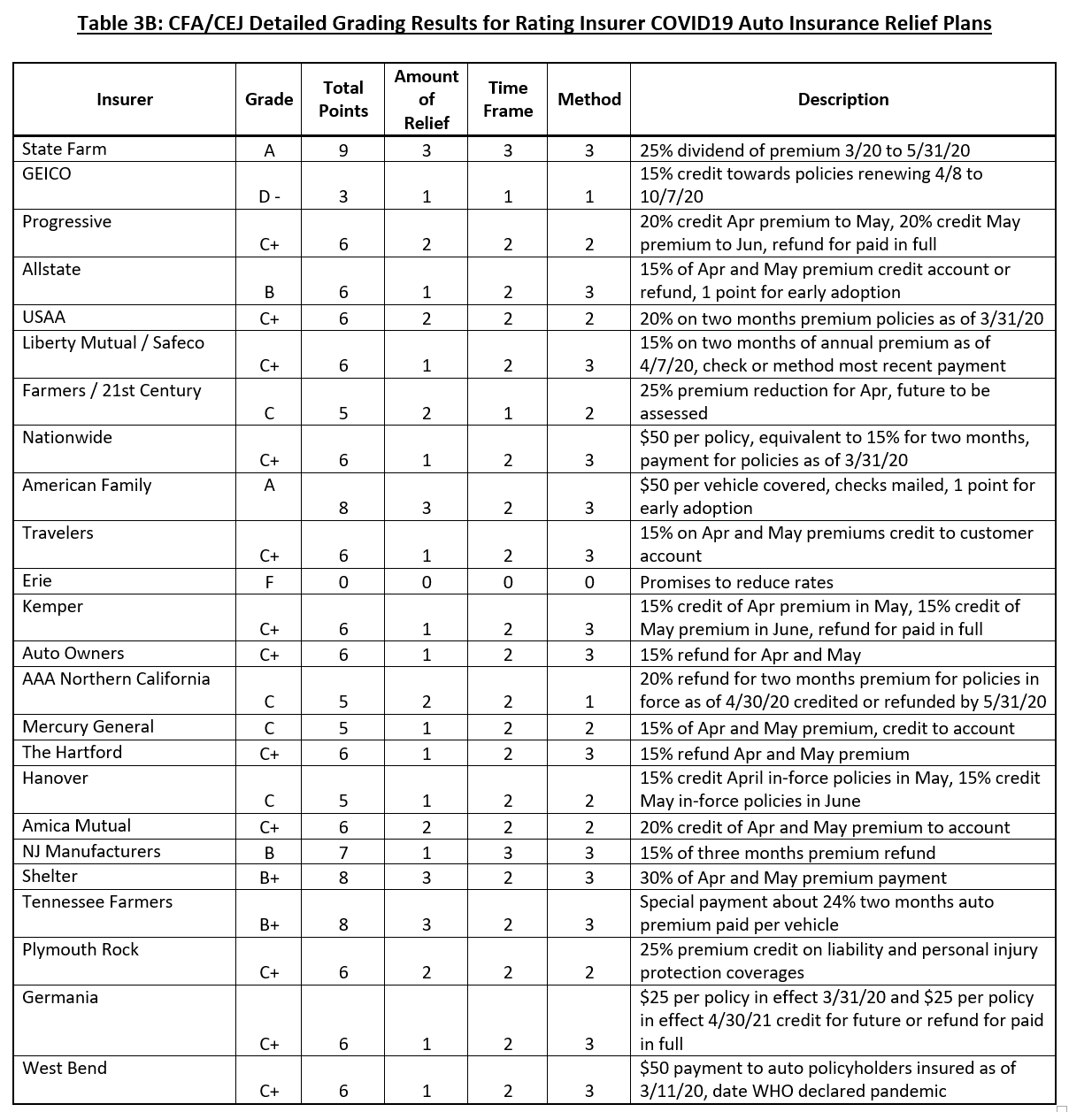

- State Farm (A), which has promised an immediate dividend to customers that accounts for about 25% of premium for the period of March 20 through May 31.

- American Family (A), which is providing an immediate $50 refund for each vehicle, equal to an average of 21% of premium for April and May. American Family also gets credit for early action.

- Shelter Insurance (B+), which is covering 30% of customers’ premium for April and May.

- Tennessee Farmers (B+), which is providing approximately 24% per vehicle covered for April and May.

- Allstate (B), which is providing 15% for April and May but gets credit for early action.

- Erie (F), which claims to be providing customers with $200 million in relief, but is actually only promising to cut rates sometime in the future.

- GEICO (D-), which has promised over $2 billion in relief is requiring customers to renew their policies before seeing savings, so only those renewing over the next two months, about one-third of GEICO’s policyholders, will see any savings during the Stay at Home orders currently in effect.

CFA and CEJ noted that, in addition to the few larger companies that have not provided relief, several smaller insurance companies, including many of the non-standard companies, that often serve poorer neighborhoods and communities of color, have not announced actions as of yet. Many of the customers of these smaller companies are Americans who have been the hardest hit by COVID-19 and statewide lockdowns.

Assessing the Response

In addition to the actions of individual insurers, CFA and CEJ are reporting on the response from state insurance regulators. The groups first apprised Insurance Commissioners of their concerns that rates were becoming excessive as mileage and claims fell precipitously in a March 18, 2020 letter. The groups urged commissioners to start collecting data and encourage companies to begin providing premium credits to customers who were staying at home or had lost their job. The groups followed up two weeks later with a March 30 letter to all commissioners.

Many states recommended or required, and many insurers responded with, an extended grace periods for non-payment of premium during the crisis. We are grateful for this crucial action to prevent loss of coverage for factors outside of consumers’ control. However, by the end of March, only commissioners from Alaska (on March 20), Maryland (March 23), and Pennsylvania (March 31) had urged insurers to provide premium relief due to reductions in miles driven and claims.

“In every state, consumers rely on their insurance commissioner to ensure that the auto insurance premiums are fair and not excessive. The regulators have worked tirelessly to respond to the COVID19 crisis, particularly on health insurance issues. Given that hundreds of millions of Americans pay for auto insurance and spend more on auto insurance than any other type of insurance other than health insurance – $250 billion in 2019 – we are puzzled by the lack of activity to date by insurance commissioners. There is still a need for the regulators to step up, as critical guidance for current and future relief is needed,” said CEJ’s Birnbaum.

A full timeline of the response to changes in the auto insurance market due to COVID-19 is provided in Table 4.

Premium Relief of More Than 50% May Still Be Needed and What Else Needs to Be Done

CFA and CEJ said that companies and regulators will need to review the impact of driving reductions on accidents and claims and, in most cases, provide additional relief. Further, companies that provides no relief should be required to immediately explain why their rates are not currently excessive and in violation of insurance rate laws in every state.

Insurance commissioners should also begin collecting data on accidents and claims activity on a weekly basis to assess insurers’ programs and determine, also, if the overall rates of companies will be excessive even after Americans start going back to work since it seems certain that America will not open up fully for some time and many small businesses may not ever come back. In their March 18, 2020 letter to Commissioners CFA and CEJ provided recommendations concerning data that should be gathered toward this end.

Table 5 provides a calculation that indicates how much premium relief should be made available depending upon different scenarios for accident reduction during the crisis. If claims drop by only one-third, premiums should drop by 26%. A more likely 50% drop in claims should lead to a 39.4% reduction in premiums, and in many regions a 67% drop should lower premiums by 52.8%, according to calculations produced by CEJ’s Birnbaum, an economist, and CFA’s Hunter, an actuary.

“Data are showing that around the country many cities and counties are seeing 80 to 90 percent less traffic on the roads,” said Birnbaum. “Accidents and claims have surely fallen by an unprecedented amount and the premiums that consumers are charged have to revised drastically to reflect this change.”

The groups also warned, as they did in their March 30, 2020 letter to Commissioners, that consumer credit sores are likely to fall in the wake of the COVID-19 crisis and massive increase in unemployment. Because credit history impacts premiums in all states except California, Massachusetts, and Hawaii, drivers could face premium increases due to the economic impact of COVID-19. Consumer groups say that there should be a moratorium on the use of credit in underwriting and pricing in the wake of this crisis.

“The continued use of credit scoring by insurers will penalize consumers who are the victims of COVID-19 and the massive economic and medical costs of the virus and government response,” said CFA’s insurance expert Doug Heller. “People’s credit score problems are coinciding with an undeniable reduction in their risk of causing an accident, so insurance credit scoring has become a clearly unfairly discriminatory underwriting, tier placement, and rating factor and should not be allowed when Americans start climbing out of this crisis.”

The groups also noted that some business insurance policies, with risk calculated on such bases as payrolls or sales receipts, also deserve similar refunds to account for significantly reduced exposure. Restaurants and retail establishments that have closed should be refunded for liability coverage for which the risk is virtually non-existent, for example. Farmers Insurance commercial insurance relief and Next Insurance has also promised rate cuts.

Table 4: COVID-19 Auto Insurance Premium Relief Timeline

Lower Premium from Fewer Claims from Fewer Cars on the Road

CFA/CEJ Actions Lead to $6.6B (and counting) Auto Premium Relief

March 13: Warren Buffett acknowledges reduction in auto insurance claims due to reduced driving from COIVD19 precautions and restrictions.[1] Buffett’s Berkshire Hathaway owns GEICO, the second largest auto insurer.

March 18: the Consumer Federation of American and the Center for Economic Justice call on regulators and insurers to provide relief for now-excessive premium charges due to fewer claims from a radical drop in miles driven.[2]

March 20: Alaska Commissioner Lori Wing-Heier issues bulletin urging insurers to adjust premiums for changes in exposure.[3]

March 23: Industry trade associations, APCIA and NAMIC, ridicule CFA and CEJ’s call for auto premium relief, betray insurance consumers.[4]

March 23: Maryland Insurance Commissioner Al Redmer issues bulletin urging insurers to consider temporary premium relief to reflect lower risk exposures.[5]

March 30: CFA and CEJ again call on regulators and insurers to provide auto insurance premium relief for March, April and May and to impose a moratorium the use by insurers of consumer credit (credit scoring) information for pricing.[6]

March 30 - April 6: National media begin reporting on the issue and pressing companies for answers to CFA’s and CEJ’s concerns.[7]

March 31: Pennsylvania Insurance Commissioner Jessica Altman issues bulletin urging insurers to offer premium relief for fewer miles driven and prohibiting insurers from penalizing consumers for a declining credit score.[8]

April 6: Allstate and American Family step up and were first to announce COVID19-related auto insurance premium relief totaling $800 million.

April 7 to 10: Insurers comprising over 80% of the personal auto insurance market announce relief for March, April and May premium totaling $6.6 Billion

April 13: CFA and CEJ call on regulators to get remaining insurers to provide relief, to provide guidance for how much, how to deliver that relief, and to collect data on new claim filings to guide future relief efforts.

Table 6: COVID19 Auto Insurance Premium – Performance by, and Actions Needed from, State Insurance Regulators

-

Thank you to regulators requiring, and insurers providing, grace periods for non-payment of premium. Cancelling a policy because someone has lost their job, hasn't gotten unemployment relief and can't pay for auto insurance would be unfairly penalizing a consumer for things outside their control.

-

Insurers became aware of drop in mileage and resulting drop in claims by mid-March. A glance at empty roads made clear premium relief was needed. We understand the insurance regulators have been in crisis mode and addressing many COVID19-related insurance issues -- particularly health insurance issues – and we appreciate the tireless work of the regulators on behalf of insurance consumers. Still, the inaction by regulators to prompt insurer action on auto premium relief was puzzling, particularly given CFA and CEJ's letters of March 18 and March 30.

-

We also thank insurers that have acted to provide auto insurance premium relief, but as Doug explained, not all relief is equal. Further, it is clear that for most insurers providing relief, the amount is not enough to reflect the drop in claims.

-

More action on auto insurance premium relief is needed and state insurance regulators need to dramatically increase their engagement on the issue:

Immediate Relief for March, April, May

Rates that were reasonable on March 1, 2020 became excessive by March 15. Consumers need and are entitled to premium relief for at least part of March and all of April and May to reflect the new reality of far fewer auto claims that anticipated in current rates. State insurance regulators should:

-

Set out best practices and expectations for relief, consistent with CFA/CEJ's best practices; and

-

Direct insurers providing inadequate relief to add more relief and direct laggard insurers to act.

Actions for June and beyond

-

Require insurers to submit data weekly on new claim filed to allow regulators and the public to assess the impact of fewer miles in real time and to monitor future changes;[9]

-

Direct insurers to prepare new rates for June forward.

-

Impose a moratorium on insurance credit scoring

Insurance Credit Scoring

A couple of states have taken action to stop the use of certain underwriting or rating factors that, while perhaps actuarially sound prior to COVID19, have become unreliable and unfair. The Ohio Department of Insurance issued the following guidance regarding insurance rating related to expired drivers licenses.[10]

The Superintendent recognizes that, as a result of these restrictions and orders, some insured Ohioans will be unable to timely renew their driver licenses. This Bulletin notifies insurers that they must not cancel, non-renew, or refuse to issue a policy of automobile insurance, or deny a claim, solely because the driver license of a named insured or other covered family member has expired since the Governor’s declaration of emergency. Additionally, the automobile insurance premium amounts charged for new or renewal automobile insurance policies must not be calculated in a manner that will adversely impact the policyholder due to an insured driver’s inability to renew his or her license

Relying upon the same logic – changing circumstances have removed the validity of certain insurance pricing factors – the Pennsylvania Department of Insurance issued a bulletin with the following guidance to insurers:[11]

On March 26, 2020, the United States Department of Labor released its seasonally adjusted initial jobless claims indicating jobless claims rose to 3,283,000. The Department understands that worker displacement during the COVID-19 disruption may negatively impact insureds’ credit scores. Insurers should review the application of credit score in the rates charged to consumers and provide flexibility, where appropriate, to policyholders who may experience a negative credit event during this time. A declining credit score may not be used to increase a premium at renewal.

The logic underlying the Ohio guidance on expired drivers licenses and the Pennsylvania guidance on credit scores holds for insurance credit scoring generally – the assumptions underlying the validity of consumer credit information for pricing insurance are no longer valid and insurance regulators should impose a moratorium on insurers’ use of consumer credit scores until such validity can be re-established. CFA and CEJ explained this to regulators on March 30:

The continued use of credit scoring by insurers will penalize consumers who are the victims of COVID-19 and the massive economic and medical costs of the virus and government response. From an actuarial standpoint, the basis for the immediate moratorium is that insurance credit scoring has become a clearly unfairly discriminatory underwriting, tier placement, and rating factor. Whatever basis insurers may have used to justify their credit-based insurance scores in times past cannot hold when declining credit scores is symptomatic of policyholders’ diminished exposure (not working and not driving, for example), exactly the opposite of what credit-based insurance models predict will happen.

Predictive models are developed based on historical data – the data are mined to see what factors are most predictive of a particular outcome. If the training data are biased, incorrect, incomplete – or not representative of the future experience – the model will reflect and perpetuate the bias in the data. In the case of insurance credit scoring, historical data will not reflect the current and near future credit experience of many consumers who have been laid off, whose business has closed, who have essentially stopped driving, who have major medical bills due to COVID-19 and more.

In the case of insurance credit scoring, it is profoundly unfair to penalize drivers, homeowners, or renters with higher insurance premiums, because they were the victims of COVID-19 or are contending with the various government responses thereto.

[1] https://finance.yahoo.com/video/exclusive-warren-buffett-coronavirus-impact-124544516.html

[2] /media/uploaded/post_18892/COVID-19-Auto-Premium-Relief-Letter.pdf

[3] https://www.commerce.alaska.gov/web/Portals/11/Pub/INS_B20-10.pdf

[4] Insurance Compliance Insight, March 23, 2020

[5] https://insurance.maryland.gov/Insurer/Documents/bulletins/20-12-PandC-temporary-rate-relief-filings.pdf

[6] /media/uploaded/post_18892/COVID-19-Auto-Premium-Relief-Letter-3-30-20.pdf

[7] See, for example, Scripps TV (3/30); Newsy (4/3); NY Times (4/6); Wall St Journal (4/6); Chicago Sun-Times (4/6)

[8] https://www.insurance.pa.gov/Regulations/Laws%20Regulations/Documents/Auto%20Notice_FINAL.pdf

[9] See CFA/CEJ March 30, 2020 letter to regulators for details.

[10] https://iop-odi-content.s3.amazonaws.com/static/Legal/Bulletins/Documents/2020-06.pdf

[11] https://www.insurance.pa.gov/Regulations/Laws%20Regulations/Documents/Auto%20Notice_FINAL.pdf