This blog is based on the testimony of CFA’s Director of Housing Sharon Cornelissen before the Environment and Transportation Committee at the Maryland General Assembly on January 21, 2025

Over the last few years, homeowners’ insurance costs have steeply risen across the country. Consumers are increasingly vulnerable to sudden policy non renewals or steep price jumps, making it essential that rules and regulations for insurance provide much-needed consumer protections. We are also at a critical turning point where we have to shift our collective mindset from relying on insurance companies to price risk, to government and insurance companies working together to reduce risk – a partnership that would involve the extensive capital and investment portfolios of these companies.

Homeowners’ insurance matters as it increasingly shapes who can afford to become and remain a homeowner. For most Americans, their home equity represents their largest financial asset. Houses do not only offer shelter and help root people in their community, but also help safeguard financial stability. For the majority of homeowners, home insurance is not optional, as lenders require homeowners with a mortgage to have homeowners insurance at all times, in order to protect the collateral of the home that underwrites the loan. This means that even if they fall behind on their insurance payment, their mortgage servicer will still charge them for what is called “force-placed” insurance – a type of insurance that only protects lenders, even as homeowners pay.

One of the key consequences of this home insurance crisis is that we’ve seen many homeowners make the difficult financial decision to go underinsured or uninsured. Indeed, last year, CFA published the “Exposed” report, where we found that one in thirteen homeowners nation-wide (7.4 percent) were uninsured.

A Close Look at the Insurance Crisis in Maryland

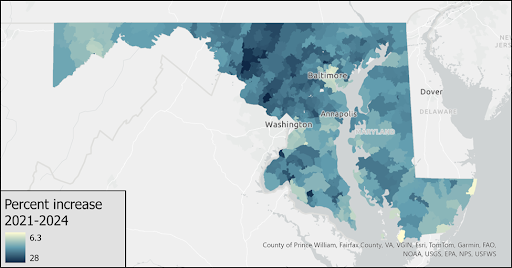

To better understand some of the implications of steep home insurance price hikes, this blog takes a close look at the case of Maryland. CFA is releasing a new report on home insurance next month, in which we use proprietary Quadrant industry data. The map of Maryland below shows premium hikes from 2021 to 2024 in the typical costs of home insurance for a homeowner covered for $350,000 in replacement value.

Figure 1: Maryland Premium Increases 2021-2024

Source: Forthcoming CFA report (2025), Analysis of 2024 Quadrant Data

The map shows that premium hikes happened almost everywhere across Maryland and often much-surpassed inflation, ranging from a 6 percent to 28 percent increase from 2021 to 2024. Rural areas and other affordable parts of the State saw some of the starkest premium hikes – giving context on how homeowners’ insurance is worsening our affordable housing crisis. Moreover, towns in Maryland with some of the highest premium increases, which were all above 25 percent, included: Gaithersburg, Frederick, Towson, Chaptico, West Friendship, and Montgomery Village.

With such steep price hikes, some homeowners may find the new rates unaffordable and fall behind on their homeowners’ insurance bills, potentially leading to non-renewal of policies. How many homeowners in Maryland did not see their policies renewed because of late payments? The Federal Insurance Office released new data this month, which provides details on Maryland zip codes with the highest nonrenewal rates because of late payments.

Table 1: Maryland Zip Codes with the Highest Late Payment Nonrenewal Rates

| Rank | Zip Codes | Town/City | Late Payment Nonrenewal |

| 1 | 21714 | Braddock Heights | 8.5% |

| 2 | 21223 | Baltimore | 3.8% |

| 3 | 20868 | Spencerville | 3.8% |

| 4 | 21864 | Stockton | 3.5% |

| 5 | 21205 | Baltimore | 3.5% |

| 6 | 21835 | Linkwood | 3.4% |

| 7 | 21912 | Warwick | 3.3% |

| 8 | 20144 | Delaplane | 3.3% |

| 9 | 21213 | Baltimore | 3.2% |

| 10 | 21051 | Fork | 3.1% |

| Maryland | State-wide | 0.9% |

Source: CFA Analysis of 2025 Federal Insurance Office Data. Data from 2022.

The table above shows that in Maryland overall, these nonrenewal percentages remain fairly low: only around 1 percent of homeowners across the entire state saw their policy cancelled because they did not make their payment on time. However, some zip codes saw much higher rates of policy non renewal – ranging anywhere from 8.5 percent in Braddock Heights, a community just outside of Frederick, to 3 percent in many other zip codes, including several communities in Baltimore.

What Can States Do to Help Tackle Our Home Insurance crisis?

With consumers experiencing rising premiums and diminishing access to home insurance, states have a range of options to enforce stronger consumer protections and direct greater investments into resiliency. Two key state policy recommendations, which have been successfully implemented in other states, provide important consumer protections.

- Better Protect Homeowners Against Sudden Nonrenewal

States should adjust insurance regulation to better protect homeowners against sudden non-renewal and give them more time to catch up on payments or find another affordable option. In many states, including in Maryland, homeowners currently only have 10 days after they miss one payment until their insurance company drops them – leaving them suddenly unprotected and in a rush to find an alternative. In this short time frame, homeowners may not even be aware that they missed a payment. Without adequate consumer protections, homeowners will be fully exposed during this period of late payment. We recommend that states extend that grace period to give homeowners 30 days to catch up on payments, starting from the day that insurers have alerted them that they are late on this bill. The California Insurance Code provides this grace period to homeowners to fend off higher non-renewal rates.

- Require Insurance Companies to Work as Partners in Risk Mitigation

States should work together with insurance companies as partners to invest in risk reduction and make community investments. A model here is the “Massachusetts Insurance Industry Community Investment Initiative” – which has been successfully run for more than 25 years and was recently renewed in 2022 with support of the insurance industry. It applies to both Property and Casualty and Life Insurers in Massachusetts. Insurers receive a tax credit, in the form of reduced tax on investment earnings, in exchange for making the required amount of investments in local housing, community, and economic development. In Massachusetts, over $544 million has been invested by Property and Casualty Insurers through this initiative.

Insurance companies are currently only in the business of insuring risk, and often withdraw from risky communities or hike up prices as they see fit. But making them investment partners in housing, community development, and resiliency would ensure that they have a stake in these places and become partners in helping to reduce collective risk. With the appropriate oversight, such a program is low-hanging fruit for states as they seek to lower both risks and premiums, while ensuring that more homeowners are protected.