Republicans in Congress and their industry allies complained throughout the Biden Administration about the CFPB’s purported “regulation by blog post” and alleged violations of the Administrative Procedure Act. These complaints were on full display at the House Financial Services Committee’s CFPB hearing last week: “The announcement of new regulatory requirements through blog postings, a Director’s speech, or other sub-regulatory pronouncements calls into question the legitimacy of the agency and creates a situation where regulatory expectations change rapidly according to the vicissitudes of each incoming administration.”

Well, well, well. A matter of weeks after the Trump Administration took control of the CFPB, the CFPB has now put out a press release providing “regulatory relief” for payday lenders and other financial institutions from the CFPB’s payday lending rule. As the Consumer Federation of America and others have pointed out, the CFPB’s action will be terrible for human beings harmed by financial institutions’ unfair and abusive practices. And did the CFPB follow required APA procedures for this “regulatory relief” – specifically, notice-and-comment rulemaking? Nope. The flagrant violation of the APA represented by the new CFPB’s action makes abundantly clear that all the grousing about “regulation by blog post” was never really serious in the first place.

A quick recap: The CFPB issued its payday lending rule in 2017, after years of research and preparation, under Director Richard Cordray. Cordray’s successor, Kathy Kraninger, pulled back much of the rule, but stood behind its “payment provisions.” The rule prevents lenders from collecting payments from people’s bank accounts in ways that may rack up excessive fees. The payday lending industry challenged the rule under the APA, and the U.S. Court of Appeals for the Fifth Circuit (!) fully vindicated the rule, though it took issue with the CFPB’s funding. The Supreme Court approved the CFPB’s funding, 7-2. And now, nearly eight years after the CFPB rule was issued, institutions were required to come into compliance last week.

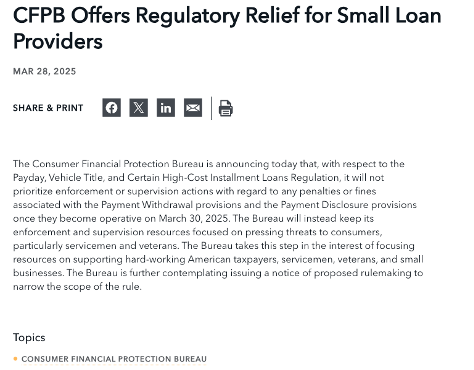

Which brings us to the CFPB’s press release:

Here’s the problem: under the APA, the federal government can’t provide “regulatory relief” from agency rules without engaging in notice-and-comment rulemaking. To give just one example, in Alaska v. Department of Transportation, the D.C. Circuit in 1989 invalidated DOT agency guidance documents purporting to provide exemptions – regulatory relief! – from existing rules. Writing for an unanimous panel, Judge Kenneth Starr (yes, that Ken Starr) found that “DOT unlawfully failed to follow the requisite notice-and-comment procedures” when it issued the exemptions. There are plenty of other examples. For instance, the Fifth Circuit in 2015 struck down the Obama Administration’s “Deferred Action for Parents of Americans” (DAPA) program because the agency failed to follow notice-and-comment procedures when announcing the relief.

Of course, as the judge dissenting from the Fifth Circuit’s DAPA ruling pointed out, federal agencies do have broad discretion about how to prioritize enforcement resources. But that’s not “regulatory relief.” The CFPB’s press release is an open invitation for payday lenders to violate the law (and hence, it goes further than other Trump Administration announcements about “not enforc[ing] any penalties or fines” under certain laws). The press release’s reference to “small loan providers” is also wrong, as the rule does not apply only to small loans or small providers of loans.

There is some good news, however. As California Attorney General Rob Bonta has noted, federal law directly authorizes states to enforce CFPB rules. See 12 U.S.C. § 5552(a)(1). Indeed, the payday rule is the first CFPB rule that states can enforce against national banks, a significant development for consumer protection at the state level. See 12 U.S.C. § 5552(a)(2). Unfortunately, there is no “private right of action” for consumers to enforce these protections directly themselves.

In the end, perhaps the most telling aspect of this saga is what it reveals about the criticism of the CFPB these past few years. All the righteous indignation about “regulation by blog post” and passionate defense of APA procedures were apparently just convenient talking points, ready to be abandoned when deregulation became the goal. Shocking.