The United States is in the middle of a housing affordability crisis. Homebuying is at its lowest level since the mid-1990s and the median first-time homebuyer is now 38 years old: an all-time high. Yet, at this critical time, the nation’s most powerful housing regulator, the Federal Housing Finance Agency (FHFA), is making it even harder for working families to get a mortgage. In a new proposed rule, FHFA is weakening Fannie Mae and Freddie Mac’s Affordable Housing Goals – goals that Congress set up to ensure these Enterprises buy mortgages affordable to working families. This new proposal will make our housing crisis worse and further limit access to homeownership, especially for first-time homebuyers.

What Are the Affordable Housing Goals?

Fannie Mae and Freddie Mac are government-sponsored enterprises (GSEs), which help lower mortgage costs for American families by purchasing originated mortgages from lenders, bundling them, and selling them to investors, in what is called the secondary mortgage market. These GSEs are unlike private companies, in that they receive unique tax exemptions and government benefits in exchange for serving the entire mortgage market, including affordable housing finance needs. Currently, Fannie Mae and Freddie Mac are controlled by U.S. taxpayers, as they have been in conservatorship since the 2008 financial crisis. However, whether in or out of conservatorship, they will always have a public mission.

To ensure that Fannie Mae and Freddie Mac fulfill that public mission, Congress passed the bipartisan Affordable Housing Goals in 1992. Since then, these annual goals have required Fannie Mae and Freddie Mac to increase mortgage access for low- and moderate-income borrowers, underserved communities, and affordable multifamily developments. With input from the public, FHFA sets annual targets for the percentage of mortgages Fannie Mae and Freddie Mac must purchase that serve these borrowers and communities. For example, this would include a mortgage going to a family of four in Washington D.C. making less than $124,000 a year (i.e. 80 percent of the area median income).

The Affordable Housing Goals help ensure that the Enterprises serve all eligible working families – ranging from public school teachers to carpenters – and don’t just purchase mortgages from the richest borrowers, such as wealthy investors and those buying a second home. The Affordable Housing Goals complement other Congressional requirements meant to keep the Enterprises focused on their mission, such as the Duty to Serve program and annual contributions to the Housing Trust Fund and Capital Magnet Fund.

What is Changing Right Now?

FHFA updates the housing goals every three years and last went through this process in 2024, when it set housing goals for 2025 through 2027. But now, Trump-appointee Bill Pulte at FHFA seeks to make a mid-cycle change. In his proposed rule, multifamily and refinance goals remain unchanged, but the goals for affordable home mortgages are lowered so much that they no longer present goals to aim for, but instead give Fannie Mae and Freddie Mac free reign to pull back from supporting lower-income to moderate-income homebuyers. The proposed goals are set below the expected private market delivery of affordable mortgages, based on FHFA’s market forecasts.

This rule is a rather blatant example of how this Administration wants to limit access to the American Dream of homeownership and is drawing sharp divisions between who they think deserves access to homeownership and who they see as undeserving buyers. Their vision of American prosperity is not only antagonistic and divisive, but deeply exclusive – many working families who may see themselves as middle-class, will find themselves at the losing end of this divide. Urban Institute research has demonstrated that the housing goals have positively impacted mortgage access for lower- to moderate-income families over the last few decades, and have lowered interest rates in markets where Fannie and Freddie have a significant presence. The Congressional Budget Office estimated that the goals will result in the purchase of about 37,000 additional eligible mortgages this year and that an estimated 750,000 homebuyers in 2025 will benefit from having a goal-eligible mortgage.

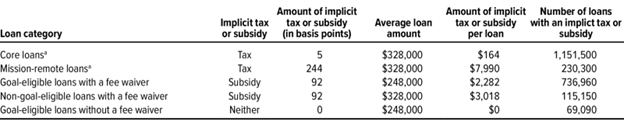

The 87-page long proposed rule includes a hotchpotch of political talking points and anti-affordability rhetoric to justify this change. One argument includes the claim that the Affordable Housing Goals have made mortgages more expensive for middle-class homebuyers. Drawing on anonymous anecdotes and speculation, the proposed rule claims that lenders “have turned away middle-class borrowers or increased prices on middle-class borrowers in pursuit of meeting housing goals.” FHFA itself acknowledges that it is not aware of “data sources that would quantify trends illustrated by these examples,” meaning that their allegations are not based on any data. According to a 2024 CBO report, the implicit subsidies going toward goal-eligible mortgages are mostly paid for by an implicit tax on so-called “mission-remote” loans, which are loans going to real-estate investors, such as those buying investment properties or second homes:

Source: Congressional Budget Office, 2024.

What this Administration calls “middle-class buyers,” then, really means real-estate investors: by zero-ing out the Affordable Housing Goals, they are prioritizing the profits of real-estate investors over the ability of everyday working families to buy their first home. The Affordable Housing Goals now serve hundreds of thousands of homebuyers every year in communities all around the country.

Weakening these goals not only puts homeownership further out of reach for working families, but also undermines Congressional intent. While FHFA has the authority to adjust the benchmarks based on market conditions, Congress stated that it expected the Enterprises to “lead the industry in making mortgage credit available” through these goals. If members of Congress want fewer of their constituents to have a chance at homeownership, they should pass a bill to that effect. However, like often in Washington D.C., these changes are being made quietly and hidden behind a wall of technical language and acronyms: in this case, a 87-page long, dense proposed rule released on the morning of the government shutdown.

This proposed rule will make mortgages harder to get for families across the country. Bill Pulte and the FHFA need to hear from the public about how stifling the Affordable Housing Goals will make our housing crisis worse. Right now, roughly 75 percent of all households cannot afford a median-priced home: the affordable housing goals are there for almost everyone. We need to keep this Administration accountable to uphold one of the most basic tenets of the Enterprises’ mission: supporting affordability in the mortgage market. Individuals and organizations interested can submit comments through FHFA’s website here by November 3, 2025.