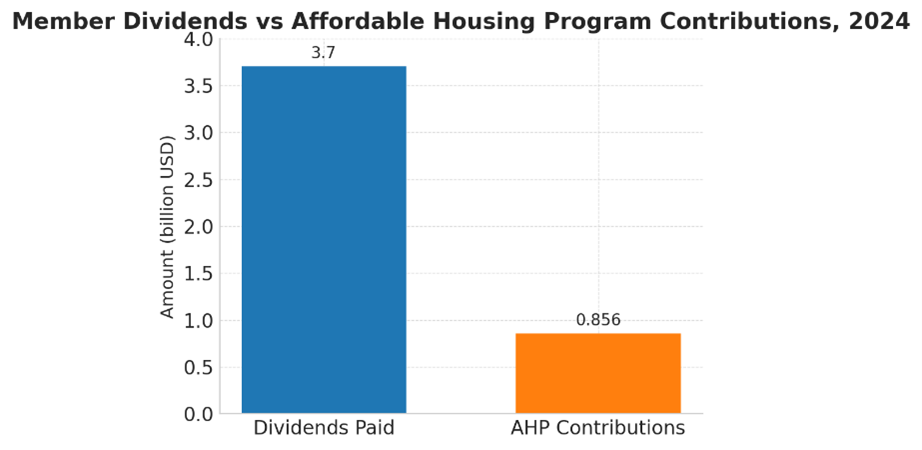

The Federal Home Loan Bank (FHLB) System is a government-sponsored system of 11 regional banks that was chartered by Congress in the 1930s to help lower housing costs by supporting affordable liquidity for housing finance. The system recently released its 2024 combined financial report, which the Consumer Federation of America analyzed on behalf of the Coalition for Federal Home Loan Bank Reform. A review of 2024 data shows that this government-sponsored enterprise (GSE) has drifted from its public mission: to support liquidity for housing and community development. In 2024, the FHLBs made $6.36 billion in profits, of which they paid out over 50% ($3.7 billion) as dividends to private members.

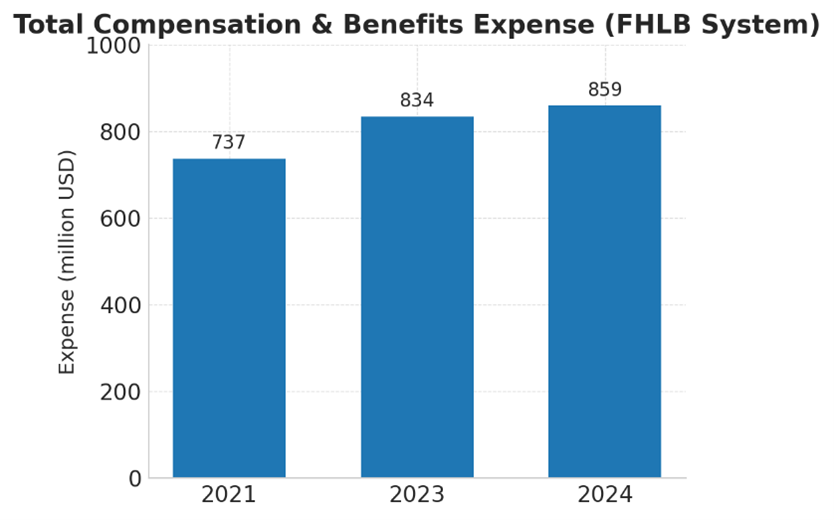

By contrast, they allocated $856 million to their housing programs (13.5% of net income), just slightly over the 10% floor set by Congress. This means that they failed to meet their own commitment to contribute 15% of net income to housing contributions. Moreover, it also means that they spent more on compensation and benefits ($859 million) than on housing programs in 2024, including paying 31 executives across the system over $1 million dollars in compensation.

The Congressional Budget Office estimates that the Federal Home Loan Bank System receives an estimated $6.9 billion in annual government support due to its unique status as government-sponsored enterprise. However, rather than supporting Americans through a housing crisis, the vast majority of the benefits of the FHLBank System flow to enrich the System itself and its private members: especially the largest banks and insurance companies. This is a wasteful and inefficient allocation of government support.

GSE Status Fueled High 2024 Profits, Despite Narrow Margins

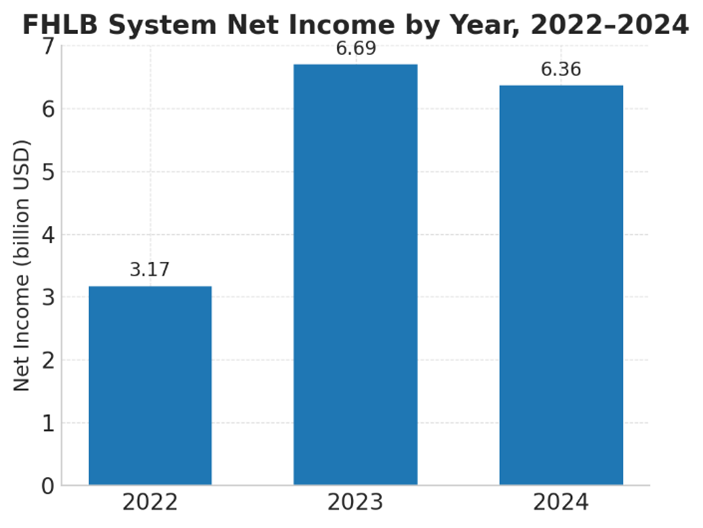

FHLB System net income reached $6.36 billion in 2024, just 5% below its record 2023 earnings and about double the $3.17 billion earned in 2022. The System’s profit stems from the FHLBs’ ability to tap capital markets at exceptionally low rates thanks to its Congressional charter and unique benefits as a GSE.

Notably, the persistence of high profits in 2024 reflects an increase in the System’s investment income. Investment income primarily benefits the System’s members, because this income allows FHLBs to lend to members at lower spreads and supports higher dividends. In 2024, advance volume fell and earned interest income on advances dropped by 10% to $43.5 billion. At the same time, interest income from investments grew to $24 billion. Investments now provide 38% of the FHLBs’ total interest earnings, up from 33% the previous year.

The FHLBs operate on very slim margins. Their average cost of funds in 2024 was 5.07%, while the average yield on assets was approximately 5.43%, a spread of only 0.36 percentage points. This narrow margin works because:

- Their funding advantage as a government-sponsored enterprise (GSE), supported by an “implied guarantee” of the federal government, lets them borrow more cheaply than private companies.

- Their credit losses are effectively zero (as a GSE, FHLBs enjoy a “superlien” status, giving them precedence over other creditors, including taxpayers protected by the FDIC).

- They don’t pay corporate taxes as a GSE.

Essentially, they “borrow low” as government-sponsored enterprise and lend slightly higher to private members, leveraging a $1.3 trillion balance sheet to generate billions in profit.

Balance Sheet Shifting to Investment Income: A GSE-Backed Hedge Fund?

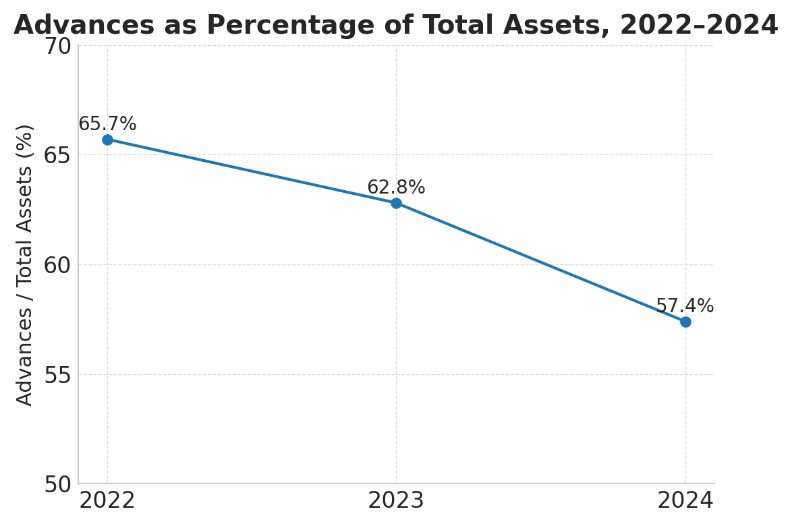

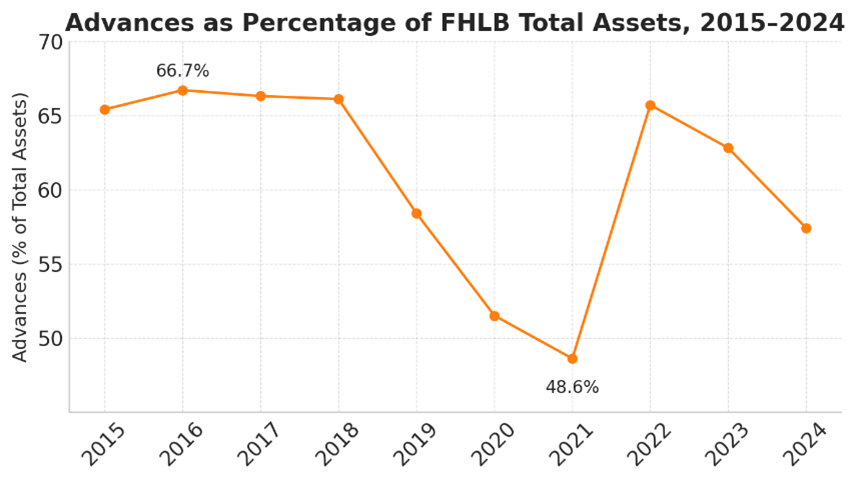

While FHLB total assets held steady in 2024 at $1.3 trillion, the composition changed significantly. Member advances fell by 9% during 2024, down to $737 billion at year-end. As a share of total assets, advances declined to 57% (from 63% in 2023 and 66% in 2022).

By contrast, the FHLBs’ investment portfolio grew in 2024. Holdings of securities reached $468 billion (36% of total assets), a 15% increase from 2023. The FHLB of San Francisco even ended 2024 with more investments than advances. This shift toward investment income even further moves this GSE away from it core activity of advance lending, and its mission to provide liquidity for housing and community development. Instead, the Federal Home Loan Banks are turning more and more into “government-sponsored hedge funds,” generating virtually risk-free high returns for its members, while relying on the implied backing of taxpayers. Nearly 40% of FHLBs’ assets are now investments undertaken primarily for income purposes, with no relation to housing finance.

Meanwhile, mission-centric assets like the Mortgage Partnership Finance (MPF & MPP) programs remain relatively small. These mortgage loans held by FHLBs were about $69.6 billion at the end of 2024 (only 5% of assets), up modestly from $61.3 billion in 2023. The surge in investments much outpaced the growth in mortgage holdings.

Who Benefits from FHLB Lending? Advance Borrowers and Market Concentration

FHLBs have over 6,500 banks, credit unions, and insurance companies that are members nation-wide. However, many members never borrow advances and a small number of members does a disproportional share of advance lending. Financial data from 2024 shows that the FHLB system primarily provides cheap liquidity to the largest banks and insurance companies, rather than serving smaller institutions focused on housing and community development finance.

The 2024 Financial Report shows that:

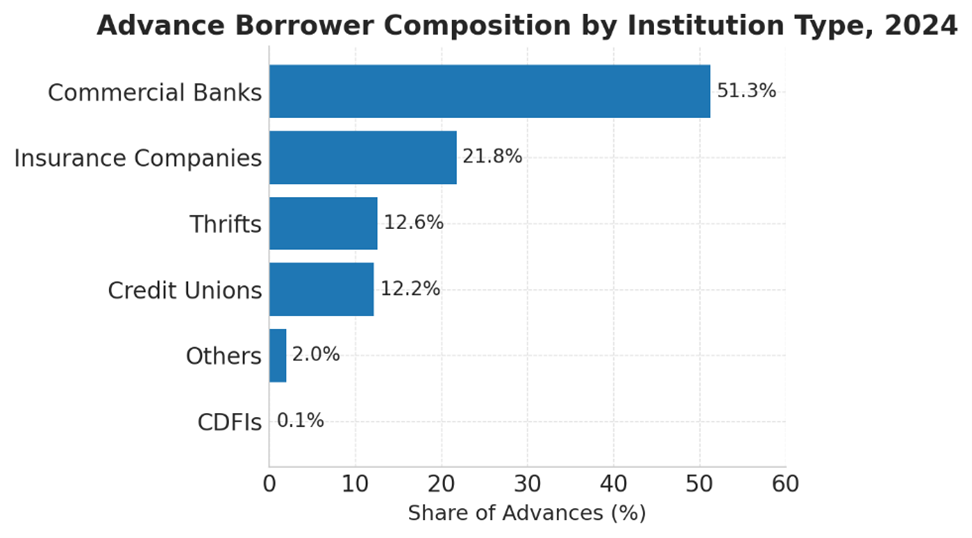

- The overall share of total advances for commercial banks dropped slightly to 51% from 54% in 2023.

- Insurance companies held 22% of advances (up from around 18% in 2023).

- Thrifts (savings associations) held 13% of advances.

- Credit unions held 12% of advances.

- Former members and housing associates were marginal borrowers (2%)

- Community Development Financial Institutions (CDFIs) only held 0.1% of advances

More striking is the concentration of advances in relatively few large institutions. As of year-end 2024:

- Just 2% of members accounted for 71% of total advance dollars (these 126 members held over $1 billion each in advances).

- The top 10 borrowers held 25% of all advances.

- Almost half (46%) of FHLBank members had no advances at year-end 2024.

Such heavy reliance on a few large institutions raises systemic risk concerns. The FHLB of San Francisco experienced this during the Spring 2023 regional banking crisis, when several high-lending members (like First Republic Bank) failed, causing 42% of its advances to run off. This concentration also raises questions about whether the FHLB System truly serves the housing market or primarily functions as a “lender of last resort” for large banks and insurers.

Private Gains vs Public Mission: Dividends vs. Affordable Housing

By law, each FHLB must set aside 10% of its annual profits for the Affordable Housing Program (AHP). This fund helps nonprofits, state housing authorities, developers, and CDFIs finance affordable housing construction and downpayment assistance programs. In 2024, the mandatory contribution was about $718 million, and the FHLBs voluntarily added $138 million more (3.5% voluntary contribution), totaling $856 million for housing programs.

This contribution is woefully small relative to profits. The $856 million allocated to housing programs was only about 13.5% of the $6.36 billion net income: importantly, it fell short of the “$1 billion in housing contributions” and FHLBs own commitment to contribute 15% of profits to housing in 2024, a promise that they heavily advertised over the last year.

Additionally, much of these allocated funds are unspent. According to their own financial data, only $484 million was actually expended on housing grants in 2024. Leftover AHP liabilities from past years have brought the total of unspent housing dollars to 1.8 billion. As the United States faces a housing crisis, communities, non-profits, and builders across the country are in critical need of these un-deployed housing funds – including the promised funds that never materialized.

Congress passed the 10% AHP minimum in 1989, at a time that FHLBs were financially recovering from the savings and loan (S&L) crisis. From 1989 to 2011, Treasury required the FHLBs to pay an additional 20% of net income every year, to pay off the System’s REFCORP obligations. But today, they have long paid off this Treasury debt and their financials show they can easily contribute more.

If Congress raised the annual mandatory housing contributions from 10% to 30% of net income, an additional $1.9 billion would have gone to affordable housing just in 2024 – without the need for a single additional taxpayer dollar in appropriations. Such an increase has been recommended in recent reform proposals: for example, Senator Catherine Cortez Masto’s Federal Home Loan Banks’ Mission Activities Act would require each FHLBank to contribute 30% of its net earnings to the AHP and related community programs.

The FHLB financials show that an increase in AHP is feasible, because as housing funds sat idle within the FHLB System, over 86% of profits were retained or paid to private shareholders. The FHLBs paid out $3.7 billion in dividends to member institutions in 2024 – more than four times what they spent on housing programs that year. This disparity has fueled claims that the FHLB System is privatizing profits while socializing risk.

The FHLBs’ response to these arguments is that providing liquidity to members indirectly supports housing finance. However, the balance sheets show that many FHLB members, especially its heaviest advance borrowers, do not originate mortgages anymore.

Executive Compensation that Exceeds Housing Funds in 2024

Operating costs at the 11 FHLBs have drawn scrutiny, with particular attention on executive compensation. Despite being cooperatives with a public mission and government support and despite having a relatively simple business model with few branch locations and employees, the FHLBs pay leadership comparable to that of large, complex, private financial firms.

In 2024:

- 31 FHLB executives earned over $1 million each.

- The average annual compensation of the 11 regional FHLBanks presidents was about $2.3 million each.

- The system spent $859 million on “compensation and benefits” expenses, spending more on compensation in 2024 than on housing contributions!

Critics from CFA and Brookings, to the Cato Institute have called out how these pay levels are wasteful and excessive for a quasi-public institution.

A Congressionally Chartered Hedge Fund Rather than Housing Engine?

Congress chartered the FHLB system as a GSE to help support affordable liquidity for housing and community development. However, analysis of the 2024 financial data demonstrates that this housing mission is increasingly ignored today. The data shows that the FHLBs spent more on salaries than on housing funds in 2024, while $1.8 billion of funding obligated to affordable housing programs remains unspent in the middle of a housing crisis.

Advance volume has been falling while simultaneously becoming more concentrated, with an uptick in FHLB investment activity. A growing share of their income (38%) comes from hedge-fund like investment behavior, rather than their Congressionally chartered mission of doing advance lending to help lower consumers’ housing costs. Advance lending itself remains highly concentrated among its largest members: just 2% of members borrowed 71% of total advance dollars in 2024.

To steer the FHLB System back to their housing mission:

- Congress should pass the Federal Home Loan Banks’ Mission Activities Act which would increase minimum housing fund contributions from the current 10% to 30% of net income. This Act also proposes to put limits on excessive compensation, linking it more closely to mission-based incentives. Finally, this Act seeks to make membership more beneficial for the smallest members, including small credit unions, community banks, and CDFIs, which are most engaged in mission-based lending and should be the primary beneficiaries of FHLBanks advances and other programs.

- FHFA should critically examine where the FHLB System can cut waste and inefficiencies, including by putting limits on excessive executive compensation and seeing where efficiencies can be generated through consolidation of functions across the 11 Banks.

FHFA should ensure that the System contributes to resolving our nation’s housing crisis. This includes expanding its MPP (Mortgage Purchase Programs), to help fill affordable mortgage liquidity gaps unsupported by Fannie Mae and Freddie Mac. FHFA should also pressure the System to develop programs that make advance lending more affordable and available to our nation’s community development financial institutions, who currently only receive 0.1% of the System’s advances. Finally, FHFA should continue to work on improving the efficiency of AHP programs and voluntary housing programs (including their transparency and public disclosures), while ensuring that the FHLBs actually spend AHP obligations, rather than leaving promised funds unspent on their books.