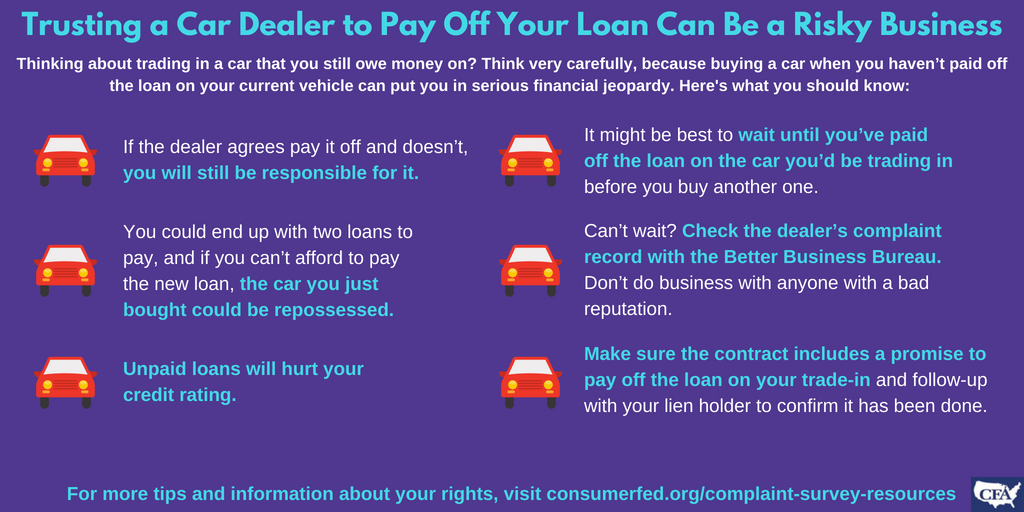

Thinking about trading in a car that you still owe money on? Think very carefully, because buying a car when you haven’t paid off the loan on your current vehicle can put you in serious financial jeopardy. Even if a dealership agrees in writing to pay off your existing loan, there is no guarantee that it will. It might be a dishonest business, one that is having financial difficulties, or may even go out of business before paying off your note.

Regardless of the reason, if the dealership fails to pay off your loan, you are the one responsible to the lien holder.

As a result, you could end up with two loans to pay and not enough money to do so. If you are unable to make your payments, your car could be repossessed. What’s more, defaulting on a loan can adversely affect your credit rating, making it hard for you to get a good interest rate on a future loan, mortgage, credit card or insurance policy. You might even be denied for a loan altogether. Even if the dealership does pay off the loan, if it delays making the payment to the bank your credit rating could still be downgraded.

Beyond these risks, the truth is that if you still owe money on your car, it’s probably not in your financial interest to sell it right now anyway, especially if you owe more than the car is worth. This is called being “upside down,” and usually means that your new car loan amount will include your existing loan balance on top of the price of your new car. Can you really afford all that? Remember that it is almost always cheaper to repair a car than to replace it. So the best thing to do from a financial standpoint is to pay off your existing car loan before you buy another car.

If, however, you can’t delay buying a new car because of a safety issue, growing family or other reason, be sure that you purchase the vehicle from a dealer with an excellent reputation. You can check the dealer’s complaint record with the Better Business Bureau. Before sealing the deal on your new car purchase, make sure that the written contract includes a promise to pay off the lien on your trade-in. Follow-up with your lien holder within 30 days to confirm that the dealership has, in fact, fulfilled that promise. If it hasn’t, your state or local consumer protection agency may be able to assist you.

This blog is one of a series of articles contributed by state and local consumer agencies in connection with the annual survey about consumer complaints conducted by Consumer Federation of America. The survey report provides “real life” examples of complaints and tips for consumers. Have a consumer problem or question? Find your state or local consumer agency at https://www.usa.gov/state-consumer.