Only One-Quarter of Big Banks Promote Accessible and Affordable Savings Accounts to Lower-Income Savers

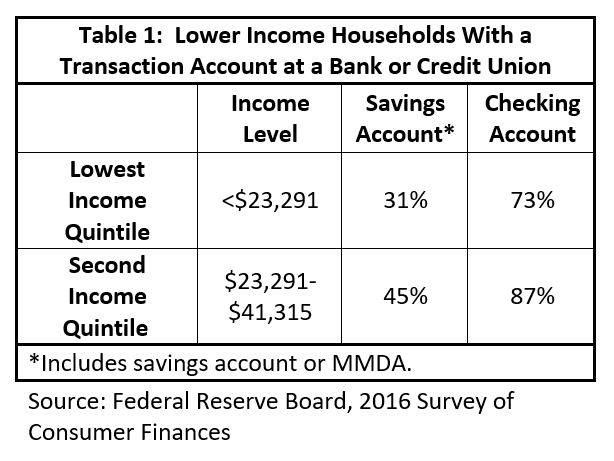

Washington, D.C. – A new Consumer Federation of America (CFA) report has concluded that only 25 of the 101 largest banks (by number of branches) promote automatic saving and offer savings accounts that are accessible and affordable to low- and moderate-income households. Disaggregating 2016 Federal Reserve Board data, the report also found that just 38 percent of households in the two lowest income quintiles (40% of all households) have a savings or money market deposit account at a bank or credit union.

“If banks made a greater effort to offer and market affordable savings accounts to lower income families, these households would be better able to meet their emergency savings needs,” said Stephen Brobeck, a CFA Senior Fellow and author of the report.

The report emphasizes the importance of savings accounts that are fed by regular, automatic transfers from checking. “80% of all lower income households [two lowest income quintiles] have checking accounts,” noted Brobeck. “It would be relatively easy for banks to promote automatic savings to these families,” he added.

The report recognizes that while small savings accounts may not be profitable for banks, they will eventually permit some customers to save larger sums and take out auto and mortgage loans. The report points out that banks can maintain these small accounts inexpensively when deposits are made automatically, withdrawals are through ATMs, and monthly statements are emailed. It also notes that the Community Reinvestment Act requires banks, especially large ones, to meet a service test for making available services, including “low-cost bank accounts.”

CFA’s 21-page report:

- Reviews research on emergency savings needs,

- Explains the importance of bank and credit union savings accounts for meeting these needs,

- Defines criteria for accessible and affordable automatic savings accounts that are promoted on bank websites,

- Uses these criteria to evaluate savings accounts offered by big banks,

- Identifies the banks that offer accounts meeting these criteria,

- Identifies those few banks offering customers financial incentives to save,

- Suggests an expanded role for regulators in encouraging banks to offer and promote accessible and affordable savings accounts,

- Outlines research that would provide important new knowledge about the effectiveness of automatic savings accounts and their marketing, and

- Offers suggestions to consumers about how to most easily build emergency savings.

As well as calling on banks to promote affordable savings, the report urges consumers to use existing bank and credit union opportunities to save more effectively.

- For those with an automated savings account, increase (even by a small amount) your monthly deposit.

- For those without an automatic savings account, ask your bank or credit union if you can automate it and, by doing so, avoid monthly fees.

- For those with a checking account but no savings account, ask your bank or credit union if they can create an automatic savings account with no monthly fees.

- For those with no checking or savings account, find a local bank or credit union that offers a savings account with a small opening deposit and no monthly fees. Ten of the 101 largest banks offer such an account, and large credit unions are even more likely to do so.

The report also learned that:

- Eighty (79%) of the big banks charge no monthly fees on savings accounts held by those under 17 or 18 years of age.

- Twelve of these banks extend the fee waiver to young adults up to the age of 24 or 25.

- Seven banks waive monthly fees for older persons.