Washington, DC. – Auto insurance premiums often rise dramatically for good drivers as a result of insurance companies’ consideration of personal characteristics related to customers’ economic status, according to new research released by Consumer Federation of America (CFA) today. CFA analyzed minimum limits liability premiums quoted to men and women in 15 cities by five of the nation’s largest auto insurers and found that premiums jumped by an average of 59%, or $681 annually, when characteristics of the drivers were changed to reflect a lower economic status. Auto insurance, which is regulated at the state level, is required of drivers in every state but New Hampshire.

A copy of the study is available here: http://bit.ly/298tfw6

“Insurance companies should judge you on how you drive, not who you are,” said J. Robert Hunter, CFA’s Director of Insurance and former Texas Insurance Commissioner. “Insurance companies are penalizing good drivers by hundreds and sometimes thousands of dollars each year based on economic and social status, and the end result is that the poor pay more, much more.”

In its study, CFA tested the impact of the following five factors commonly used by insurers to price auto insurance:

- Level of Education

- Occupation

- Homeownership status

- Ownership of a car during prior six months

- Marital status

Despite having the exact same driving record and living at the same address, drivers pay higher premiums 92% of the time if they have a high school degree and a blue collar or hourly job, rent their home, have not owned a car (and had no auto insurance) for the past six months, and are unmarried. Each of these is associated with lower economic status. Among the other findings of the report:

- The average premium for all drivers with high economic status indicators is $1,144, while the low economic status driver is charged $1,825, a $681 (59%) increase.

- GEICO and Progressive charge the largest average percentage increases (92% and 80%, respectively) to lower economic status drivers.

- Allstate and Farmers charge the largest average annual dollar increases ($915 and $900, respectively) to lower economic status drivers.

- State Farm charges smaller increases to lower economic status drivers (13%, or $217 annually).

- Drivers in Queens, NY; Jersey City; Boston; Atlanta; Minneapolis; Houston; and Jacksonville face some of the steepest increases, all of which average more than $700 more per year for good drivers due to their economic status.

Most Americans Reject Insurance Companies’ Rating Practices, According to New Poll

Most Americans believe that auto insurance premiums should be tied to policyholders’ driving safety record and accident history and that insurance companies should not use personal economic factors such as their education or occupation, according to a national poll conducted by ORC International June 9-12, 2016.

In the survey, a representative sample of 1,000 Americans were asked: As you probably know, auto insurers use many factors to decide how much each driver is charged for their insurance coverage. How fair do you think it is for insurers to use each of the following factors in deciding on an auto insurance price for a driver? Would you say each is very fair, somewhat fair, somewhat unfair or very unfair?

According to the survey, Americans overwhelmingly reject the economic and personal factors that often drive the premium setting strategies of major insurance companies.

While the vast majority of Americans consider it fair to use moving violations and traffic accidents in pricing, few consider it fair to use non-driving related factors related to economic status. The percentages of Americans who find each factor fair are:

Only about one American in ten believes the use of education, occupation, home ownership, marital status, no previous insurance, or credit score is “very fair.”

“The American people don’t like the idea of insurance companies using personal and economic factors to set premiums, even though most people don’t realize how much of an impact these non-driving characteristics have on the price they pay for coverage,” said the study’s co-author Doug Heller.

In Some Cities, Economic Rating Factors Can Cost Customers More Than $1,000 Per Year, Others Get No Offer

The use of economic factors varied by company and from city to city, but drivers in all cities but Los Angeles saw rates rise by at least 33% on average after accounting for the cumulative impact of the five factors. The average impacts of these rating practices, by city, are:

Los Angeles was the only city tested in which there was consistently little difference between the lower economic status driver and the upper economic status driver. This is because, under California’s consumer protection laws, all of the non-driving factors tested in this report are prohibited from use in auto insurance pricing in California with the exception of marital status, which accounts for the 9 percent, or $80 per year, average premium difference seen in Los Angeles.

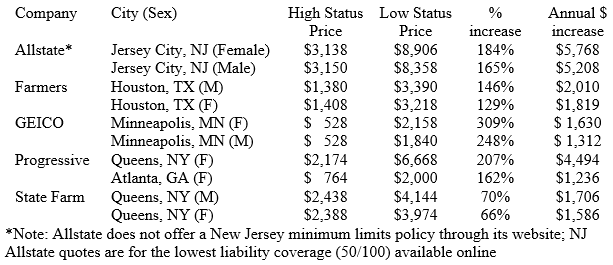

Within several of the cities studied there were some extremely large price increases by individual insurers. The two largest rate hikes for each company, among the cities tested are:

The only instances where premiums came down for lower-income drivers were from Allstate, which lowered rates by 19 percent for the lower economic status female driver in Chicago and by 4 percent for both male and female drivers in Oklahoma City.

In addition to the high prices for drivers with low economic status indicators, CFA found that in several instances, insurance companies refused to provide an online quote to these drivers. In 21 instances, State Farm, Farmers, or Allstate would offer a quote for coverage to a high status driver but did not supply a quote to his or her lower economic status counterpart at the same address. The inability to get an online quote for coverage creates another barrier to obtaining coverage for lower- and moderate-income drivers, according to CFA.

CFA noted that due to the constraints of web-based premium testing, the study does not include any changes to premiums due to a customer’s credit score. A 2015 study published by Consumer Reports, however, indicated that premiums rise significantly for a driver with low credit score, which would further increase the disparities found in this report in every city except Boston and Los Angeles where auto insurance credit scoring is prohibited.

CFA Recommends Regulators and Lawmakers Ban the Use of Economic Status Factors in Auto Insurance Rating and Underwriting

After reviewing the data, CFA prepared a series of recommendations for regulators and lawmakers to protect consumers from the unfair pricing practices uncovered in its report. The central proposal is that states should enact legislation that emphasizes drivers’ accident and ticket records and prohibits the use of non-driving related characteristics such as those discussed in the report.

“Drivers are required to buy auto insurance in all states but New Hampshire regardless of their economic status, which means that it is the duty of lawmakers and regulators to protect consumers from unfair pricing practices of the insurance industry,” said Hunter. “They have, with only a couple of exceptions, completely failed to do their duty,” he said.

This report is one of a series of reports on the cost of auto insurance and particularly its impact on low- and moderate-income Americans. A complete list of those studies with thumbnail descriptions is available here.

The Consumer Federation of America is an association of more than 250 non-profit consumer groups that, since 1968, has sought to advance the consumer interest through research, education, and advocacy.