Most Large Auto Insurers Charge 40 and 60-Year-Old Women Higher Rates Than Men, Often More Than $100 Per Year

Washington, D.C. – Female motorists with perfect driving records often pay significantly more for auto insurance than male drivers with identical driving records and other characteristics the insurers use to price auto insurance, according to new research by the Consumer Federation of America (CFA) released today. This finding contrasts with the public perception that men pay more than or the same as women for auto insurance. According to a national public opinion survey, less than a quarter of Americans correctly think that women pay more.

In ten cities studied, CFA found that 40- and 60-year old women with perfect driving records were charged more than men for basic coverage nearly twice as often as men were charged the higher rate. Premiums were lower for 20-year old women than for 20-year old men most of the time; however, GEICO charged young female drivers more than young male drivers in nine of ten cities. These price differences are particularly important, according to CFA, because every state except New Hampshire requires drivers to purchase basic liability insurance coverage.

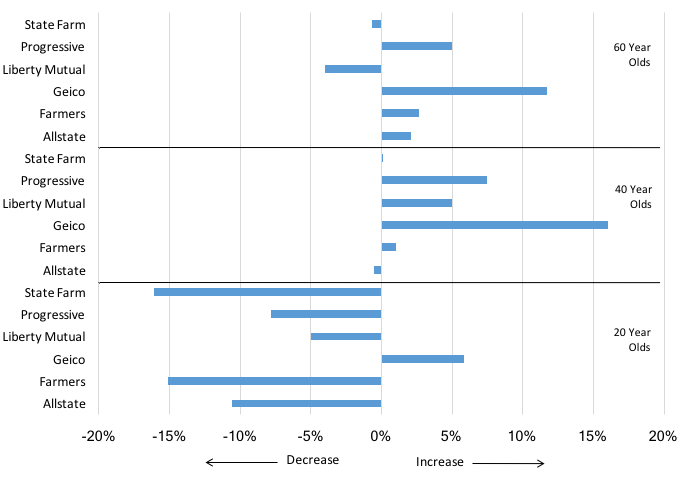

Figure 1. Average Premium for Female Drivers Relative to Male Drivers by Company and Age

Twice as Many Americans Think Men Pay Higher Premiums than Think Women Pay More, According to New Poll

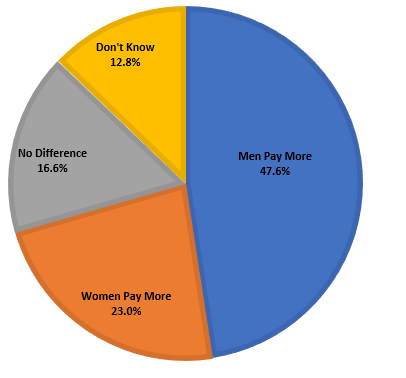

48 percent of Americans think auto insurers charge men more for coverage than women, while only 23 percent of Americans think women are charged more, according to a national survey conducted for CFA by ORC International. 17 percent think men and women are charged the same for coverage. The survey asked respondents to exclude “teenagers and other young drivers” when thinking about who pays more to eliminate the possibility that respondents were focused on young male drivers, who generally do pay higher premiums. (The telephone survey of 1,004 Americans was conducted between September 28, 2017 and October 1, 2017 and had a ±3.09% margin of error.)

Figure 2. “Excluding teenagers and other young drivers, do you think that auto insurers tend to charge higher rates to men or to women?”

Testing Found that Women Paid Higher Premiums More Often than Men, Sometimes by Significant Amounts

CFA researchers sought online premium quotes from the websites of Allstate, Farmers, GEICO, Liberty Mutual, Progressive, and State Farm, then compared 165 pairs of quotes for men and women. This comparison revealed that 40-year old women were the most likely to be charged more than men, and 60-year old women also were penalized more often, facing higher premiums than their male counterparts in 58% of the instances in which companies used a driver’s sex to alter rates.

Other findings from the testing include:

- In 38 instances, women with perfect driving records were charged at least $100 more per year than male drivers.

- In six instances good drivers faced premiums at least $500 higher solely because they were female.

- GEICO charged female drivers higher premiums 83 percent of the time, with surcharges on women averaging $176 annually, including average penalties of $143 on young females compared with young male drivers;

- Progressive charged women more 60 percent of the time, while Allstate, Liberty Mutual, and Farmers each charged men higher rates more often.

- State Farm typically did not charge different premiums to men and women, except that young male drivers always faced significantly higher annual premiums – $488 more on average – than their female peers.

“It is widely believed that male drivers, especially young male drivers, cause more, and costlier, accidents,” said J. Robert Hunter, CFA’s Director of Insurance and former Texas Insurance Commissioner. “State insurance commissioners should insist that auto insurers explain why they usually charge middle-aged and older women higher rates than men,” he added.

CFA noted that Robert Hartwig, co-director of the Center for Risk and Uncertainty Management at the University of South Carolina and former president of the insurance industry’s Insurance Information Institute recently told the Atlanta Journal Constitution: “Let me go way, way back to perhaps one of the first rating factors ever used —gender. No one doubts males are worse drivers than females in every respect.”

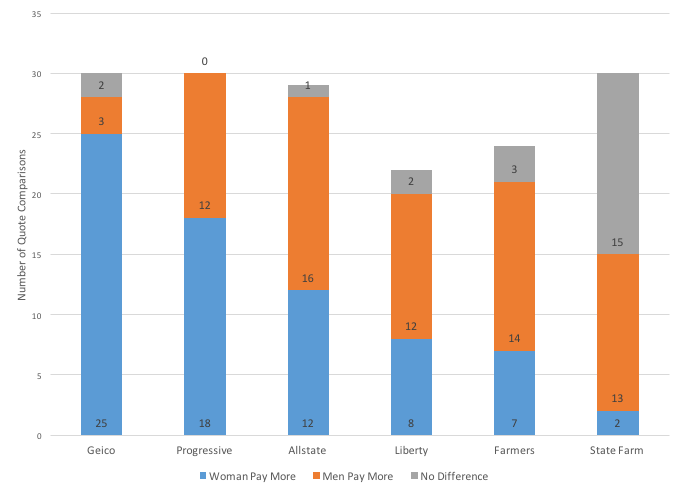

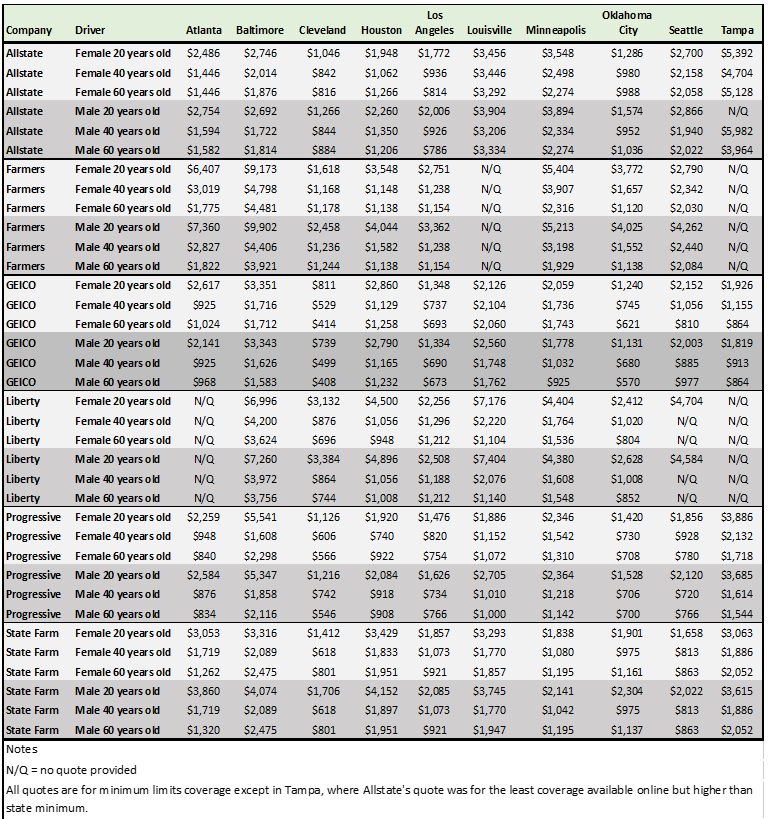

CFA tested premiums in ten cities: Atlanta, Baltimore, Cleveland, Houston, Los Angeles, Louisville, Minneapolis, Oklahoma City, Seattle, Tampa. In each city, CFA sought online insurance quotes for female and male drivers ages 20, 40, and 60, with all other characteristics remaining the same throughout the testing. In every test, the driver had a clean record with no history of tickets or accidents. For all but one test the premium quoted is for the minimum liability coverage required under state law; in Tampa, Allstate.com would only provide a quote for slightly more than the state mandated minimum coverage. The distribution of surcharges on women compared with men is shown by company in Figure 3 below, and the complete set of premium quotes is included as an appendix.

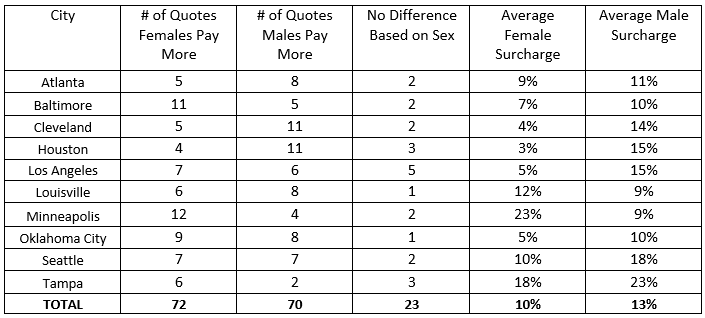

Figure 3. Sex of Driver Has Significantly Different Impacts Among Companies

Findings Highlight Flaws with Auto Insurance Companies’ Use of Non-driving Rating Factors; GEICO Almost Always Treats Women as Higher Risk, State Farm Almost Never

The inconsistent pricing decisions of these insurance companies illustrates CFA’s concern that tying auto insurance rates to factors that a customer cannot control and have nothing to do with their driving safety record – such as one’s biological sex – leads to unfair discrimination and indefensible claims of actuarial soundness.

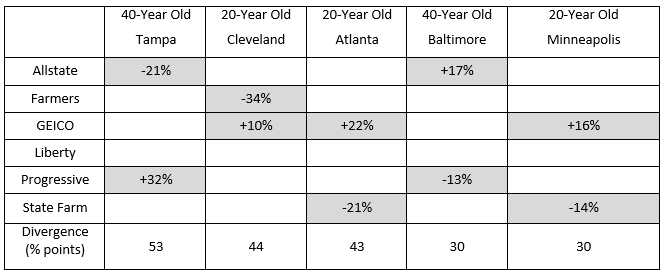

To illustrate the inconsistent conclusions drawn regarding drivers’ sex, CFA noted that in more than two-thirds of the tests, at least one company treated female drivers as being higher risk than males while another company deemed them lower risks than their male counterparts. Among 40-year old drivers in Tampa, for example, Allstate charged the female driver 21% less than the male driver, while Progressive charged her 32% more. Figure 4 illustrates the five most divergent rates by sex CFA found.

Figure 4. Rate Increase (Decrease) for Female Drivers – 5 most divergent rates

“What stands out, first, is GEICO’s aggressive punishment of good drivers simply because they are female, but also notable are the impossibly different interpretations of the relationship between sex and insurance risk,” said Hunter. “If sex were an actual risk factor, we wouldn’t see companies using it in such divergent ways.”

The inter-company differences between surcharges for men and women of the same age in the same city suggest that at least some of the companies are not making actuarially sound selections in their pricing structure, according to CFA’s Hunter, an actuary. These companies are large enough that their losses in an area should be fairly similar for similar risks. They may differ a bit, Hunter said, driven in part by different underwriting objectives and marketing strategies of the companies, but not so much as to cause rating differences by sex that are 30, 40, or 50 percentage points apart.

The relative risk associated with sex should not shift dramatically between cities within one company either, according to CFA. Progressive, for example, imposed a 32% premium hike on 40-year old female drivers in Tampa and a 3% hike on the women of Oklahoma City, while it lowered rates compared to men by 18% in Cleveland. Similarly, Allstate charged a 40-year old women in Houston and Tampa 21% less, but charged the same women 17% and 11% more in Baltimore and Seattle, respectively. These geographic differences suggest that the inherent riskiness insurers associate with being a female driver goes up or down substantially based on where they live.

“This makes no sense,” said Hunter. “If these large insurance companies are abiding by actuarial principles, you would not find one insurer granting a 21% price break for female drivers while another company sees a need for a 32% surcharge on those same drivers,” said Hunter. “Also, how can a company think that the women of Tampa are very high risks, but women of Cleveland are very low risks relative to men? A woman moving from Tampa to Cleveland does not magically become a better driver. What this really tells us is that either some companies are ignoring the data or that gender is not a good indicator of risk and should not be used.”

GEICO, in Particular, Has Some Explaining to Do

Figure 5 shows the average premium decrease (-) or increase (+) given to female customers across all cities. While each company has some large increases or decreases for certain drivers, only GEICO averages a double digit penalty for “driving while female.”

Figure 5. Average Decrease/Increase for Female Drivers by Company

| Allstate | -3% |

|---|---|

| Farmers | -4% |

| GEICO | +11% |

| Liberty Mutual | -1% |

| Progressive | +2% |

| State Farm | -6% |

Some Cities See More Severe Sex-based Premium Hikes than Others

CFA’s testing found that female drivers in Baltimore, Minneapolis, and Tampa were most likely to pay more than male drivers compared with the other cities tested. Males were most likely to see higher rates in Atlanta, Cleveland, and Houston compared with other cities. Driven by the substantially higher rates charged to young men by Allstate, Farmers, and State Farm, the average surcharge stemming from the sex of a driver is more severe for men than women, though women are surcharged more often, as shown in Figure 6.

Figure 6. Sex of Driver Raises Premiums More Often for Women, Higher for Men

“Every state but New Hampshire requires drivers, regardless of their sex, to buy auto insurance, so regulators and lawmakers have a special obligation to make sure coverage is priced fairly,” said CFA insurance consultant Douglas Heller, who conducted the study with CFA Research Advocate Michelle Styczynski. “What we have found is that insurance companies punish female drivers with perfect records more often than men, and far more often than we expected. We also found that the insurance companies’ use of sex as a rating factor does not seem to reveal much in the way of a consistent risk assessment, and regulators should reconsider allowing companies to continue using it at all.”

Contact: Bob Hunter, 703-528-0062; Doug Heller, 310-480-4170

Appendix: Annualized Premium Quotes

The Consumer Federation of America is an association of more than 250 non-profit consumer groups that, since 1968, has sought to advance the consumer interest through research, education, and advocacy