Washington, D.C. – The Consumer Federation of America (CFA) has called upon Kentucky Insurance Commissioner Sharon Clark to address auto insurance prices that leave financially vulnerable Kentucky drivers with massive surcharges, even when they have perfect driving records. According to CFA’s research, a driver living in the West End of Louisville with a perfect record but a poor credit history pays $2,089 more per year on average for minimum coverage than a driver with the same driving record but an excellent credit score and a home in the city’s East End.

In a letter sent to Commissioner Clark earlier this week, CFA wrote that, especially because Kentucky law requires every driver to buy insurance, “it is critical that consumers do not face unfair discrimination, and that historic, institutional, and algorithmic biases do not create disproportionate burdens on consumers according to their race, ethnicity, or socio-economic status.”

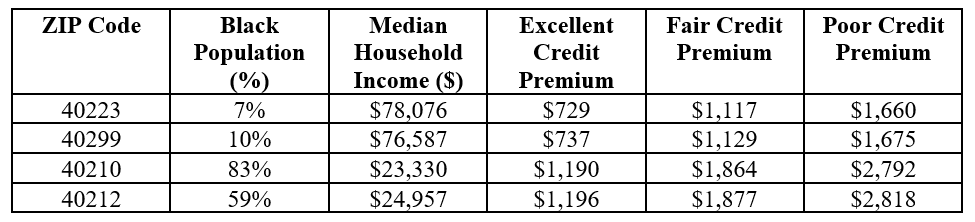

CFA acquired premium data on the cost of basic auto insurance in every ZIP code in the state of Kentucky from some of Kentucky’s largest insurers. In the data, CFA found dramatic price differences based on consumers’ credit history and the neighborhood in which they live. Statewide, Kentucky drivers with a perfect driving record and excellent credit pay an average premium of $689, but if drivers with the same driving record have fair credit, their premium climbs to $1,080. If the driver has the same driving record but has poor credit, their premium is $1,625—meaning they pay 136% more just because of their credit.

The analysis also found that this credit discrimination is compounded by auto insurers’ discrimination based on territory. In Louisville, the data show that mostly Black, low-income ZIP codes pay far higher premiums compared to mostly white, wealthy ZIP codes. Good drivers in some ZIP codes pay almost $2,000 more annually for auto insurance, as demonstrated below.

Average Good Driver Premium for Minimum Limits Auto Insurance, by ZIP and Credit History

CFA’s analysis expands upon research conducted early this month by Louisville’s WAVE 3 news, which focused on price differences among different ZIP Codes, but did not address the impact of residents’ credit history on rates. When WAVE 3 asked the Kentucky Department of Insurance what they were doing about this injustice, the Department reportedly said, “this is not a Louisville-specific issue.”

“Kentucky requires all drivers to have auto insurance, but the Department isn’t doing enough to make auto insurance affordable or to prevent unfair discrimination in the market,” said Michael DeLong, CFA’s Research and Advocacy Associate. “They should investigate this discrimination, prohibit credit-based pricing and block the kind of territorial rating that leads to the unacceptable disparities we see in Louisville. Kentucky consumers deserve better.”

Contacts:

Michael DeLong, 925-708-1135

Doug Heller, 310-480-4170