Washington, D. C.– Fees charged by neighborhood check cashers to tum paychecks and government benefit checks into cash have risen sharply in the last ten years, according to a report released today by Consumer Federation of America. In addition to cashing checks for a percentage of face value, check cashers in some cities have begun making short-term loans, charging annual interest rates of261% to 913% to advance cash for two weeks on post-dated personal checks (“payday loans”).

“The bankless and underbankcd pay a very high price for the convenience of services sold by check cashing outlets,” stated Jean Ann Fox, CFA Director of Consumer Protection. “No area of financial services is in greater need of effective consumer protections.”

Check Cashing Costs High and Rising

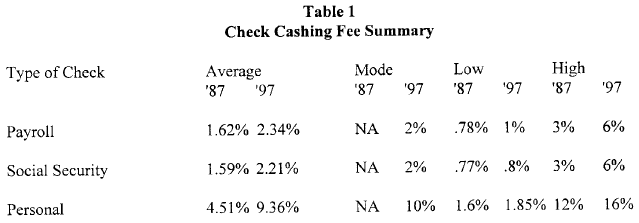

CFA surveyed 111 check cashing outlets in twenty-three of the largest urban areas of the country, asking for information on the cost to cash payroll, government and personal checks. As Table 1 shows, the telephone survey found:

The average cost of cashing a paycheck was 2.34%, with a range of 1% to 6%. That means it costs $7.49 on average to cash a $320 paycheck. The fee can cost as much as $19.20. The annual cost of cashing fifty $320 paychecks averages $374.50, with a range from $160 to $960.

The average cost to cash a Social Security check was 2.21% of the check, with a range of .8% to 6%. That means it costs an average of $11.05 to cash a $500 Social Security check, with a range from $4 to $30. The annual cost of cashing twelve $500 Social Security checks averages $132, with a range from $48 to $360 a year.

The average cost of cashing a personal check was 9.36% or $14.04 for a $150 check. The range of fees for personal checks was 1.85% to 16%, or $2.77 to $24 for this check.

A consumer cashing six $150 personal checks per year at a check cashing outlet would pay an average of$84.24, but could pay as low as $16.68 or as high as $144.

Compared to ten years ago (1987) when CFA first surveyed check cashers, the average cost of cashing paychecks has increased 44% while the cost of cashing Social Security checks has risen 37%. The average cost of cashing personal checks more than doubled.

Growing Check Cashing Industry Regulated Inadequately

The ranks of check cashers has grown from 2,151 outlets in 1986 to 5,400 today according the National Check Casher Association. The industry currently cashes 150 million checks a year worth $45 billion. Check cashing is also profitable. An Illinois study found that check cashers in that state racked up a 104% return on investment from 1988 to 1991.

Eighteen states regulate check cashers, and only twelve of these states cap fees. Those states are California, Connecticut, Delaware, Florida, Georgia, Illinois, Indiana, Minnesota, New Jersey, New York, Ohio and Rhode Island. Fee caps are as low as 90 cents for welfare checks in New Jersey to a high of 10% for checks in Indiana. The highest rate found by CFA in unregulated states was 6% for a payroll or government check and 16% for a personal check.

Yesterday, CFA sent its check cashing report to the fifty state banking regulators and state Attorneys General, requesting support for effective state laws to limit fees on check cashing and to protect consumers who use check cashing outlets as their neighborhood “banks.” (Sample letter here).

“Effective state regulation of check cashers is particularly important now that millions of consumers are moving from welfare to work,” explained Jean Ann Fox. “Most consumers leaving welfare do not have bank accounts and will now need an inexpensive means of cashing paychecks.”

Payday Loans Carry Exorbitant Rates and Require Regulation

Some check cashers have gone beyond simply cashing checks for a fee to loaning money on postdated checks to tide consumers over until their next payday. Typically, a consumer writes a check for $115 and receives $100 cash. The check casher agrees to hold the check until the next payday when he can allow the check to be sent to the bank, redeem it by bringing in $115 in cash, or “roll” it over by paying the fee to extend the loan for another two weeks. Payday loan fees translate to triple digit annual interest rates. A consumer who doesn’t make good on the check can be threatened with criminal charges for writing bad checks.

Payday lending is a fast-growing sideline for check cashers. National Cash Advance, a Tennessee chain, opened 165 stores in less than three years. Check Into Cash, another Tennessee payday loan company founded in 1993, has locations in 20 states and reported $9.9 million in 1996 loan volume, nearly triple its 1995 loans. Consumer lawsuits, enforcement actions by state attorneys general, and hotly contested battles to legitimize exemptions from usury laws in state legislatures have tracked the growth in payday lending.

CFA surveyed 26 check cashers who advertise payday loans in Yellow Page listings. These were located in fifteen ofthe 23 cities surveyed by CFA for check cashing fees. CFA computed effective annual percentage rates for $100 payday loans on checks held seven days, with results ranging from 521% to 1820%. For payday loans held 14 days, the annual interest rate ranged from 261% to 913%.

“Payday loans are a transfer of wealth from the poor and the poor-risk to the predatory and the powerful,” according the CFA’s Jean Ann Fox. “America hasn’t come very far from tum-of-the-century ‘salary-buyers’ and ‘loan sharks’.”

Even some banks are involved in payday lending. For example, Eagle National Bank of Upper Darby, Pennsylvania, makes “Cash ‘Til Payday” loans through Dollar Financial Group’s national network of check cashing outlets. Eagle National Bank loans up to $200 for a maximum of 28 days for a $24 fee. A typical $100 loan for 14 days costs $12 or 313% APR.

Some states ban cash advance loans as violation of small loan laws or state usury caps. Other states have legitimized payday lending with restrictions, including California, Colorado, Iowa, Kansas, Louisiana, Minnesota, Nebraska, Ohio, Oklahoma, Washington and Wyoming. State laws against payday loans by check cashers or by unlicensed small loan companies have failed to prevent a national bank from making these loans through check cashers, since most state small loan acts and check casher licensing laws exempt banks and states have no control over interest rates charged by out-of-state national banks.

“CFA calls on the Comptroller ofthe Currency to take action to make sure national banks do not slip through loopholes in state laws against usurious payday loans,” Jean Ann Fox stated. “We urge states to include state banks under small loan interest rate limits and check casher payday loan prohibitions.”

The CFA report calls for an outright ban on payday loans that do not comply with state small loan rate caps or usury ceilings. Other payday loan protections recommended by CFA to state officials include a ban on paying one loan with the proceeds of another, a prohibition against threatening borrowers with bad check criminal proceedings, and treatment of unpaid loans as unsecured debts in bankruptcy filings.

EFT’99 Offers Potential Solutions to Check Cashing Problems

Treasury officials are now drafting regulations to implement the law requiring all federal checks to be electronically deposited by 1999 (EFT’99). If designed to be consumer-friendly, the rules can open the door to traditional financial institutions for the ten million unbanked American households who receive federal checks. CFA has urged Treasury not to define check cashers as

”authorized payment agents” permitted to receive electronic federal checks including Social Security, pension, or Supplement Security Income payments. Instead, CFA supports requiring that these funds be electronically deposited into individual low cost accounts at insured depository institutions. The CFA report notes that access to low-cost bank accounts will eliminate the need to pay check cashers to cash federal checks while introducing millions of consumers to mainstream banking.

“Treasury should not force federal recipients to go to fringe bankers, such as check cashers, to receive their federal checks,” Ms. Fox stated. “Surely it was not Congress’s intent to put consumers at the mercy of high priced check cashers just to save the cost of printing and mailing paper federal checks.”

Advice to Consumers

To reduce fees and save money, CFA urges consumers to maintain a low-cost account at a credit union or bank to cash checks for free and pay bills by check instead of by purchased money orders. A savings or checking account can also help consumers build up a safety margin of savings and start building their credit rating. Consumers can look for lower-cost alternatives, such as cashing checks at retail stores, or asking an employer to pay in cash or make arrangements for a nearby bank to cash employee checks. Consumers can cash checks at the bank on which it is drawn, even if the recipient does not have an account at that bank. Adequate identification is required.

CFA advises consumers to avoid payday loans for emergency credit. Licensed small loan companies, secured credit cards, and overdraft protection on checking accounts, although expensive, are a better buy than triple digit interest rates on cash advance loans. CFA reminds consumers to shop for credit by comparing the annual percentage rate(%) as well as the finance charge($).

CFA is a non-profit association of some 240 pro-consumer groups that was founded in 1968 to advance the consumer interest through advocacy and education.