Washington, D.C. — At a press conference this morning, the Consumer Federation of America (CFA) — joined by Consumers Union, USPIRG, and the United Auto Workers — issued its fourth report on credit card debt. CFA’s principal finding is that cardholders are exercising more restraint while card issuers expand their marketing, lines of credit, and profitability. CFA also learned, through a national opinion survey, that the public strongly supports new consumer bankruptcy protections.

“Credit card issuers are shameless to lobby for personal bankruptcy restrictions while they aggressively market and extend credit,” said Stephen Brobeck, CFA’s executive director. “While they urge Congress to deny families access to bankruptcy relief, these issuers enjoy high and increasing profits,” he added.

Increases in Credit Card Debt, and Consumer Concern About Repayment, Both Decline

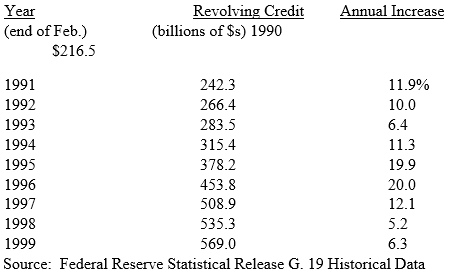

Data from the Federal Reserve suggests that the growth of credit card indebtedness has slowed. As the table below indicates, despite double-digit annual increases for most of the decade, during the past two years revolving credit rose only at a 5-6 percent annual rate.

The following table reports levels of revolving consumer credit at the end of February. The Fed estimates that 95 percent of this revolving credit is credit card debt.

Even more encouraging than this slowdown in the increase in credit card debt is the decline in the percentage of U.S. households that say they are “very concerned” about meeting their credit card monthly payments. In June 1997 and then again last week (April 1999), in surveys commissioned by CFA, Opinion Research Corporation International posed the question to a representative sample of adult Americans: “Overall, how concerned would you say you currently are about meeting your credit card monthly payments?” In June 1997, 36 percent said they were very concerned, but last week, only 31 percent said they were very concerned.

Of course, this decline may reflect, in part, favorable economic conditions. Also, of those households with at least one credit card, those with low incomes are the most concerned about making monthly credit card payments. 47.4 percent of households with incomes below $15,000 and with at least one card were very concerned.

Card Issuers Increase Marketing and Credit Lines More Rapidly than Consumer Borrowing

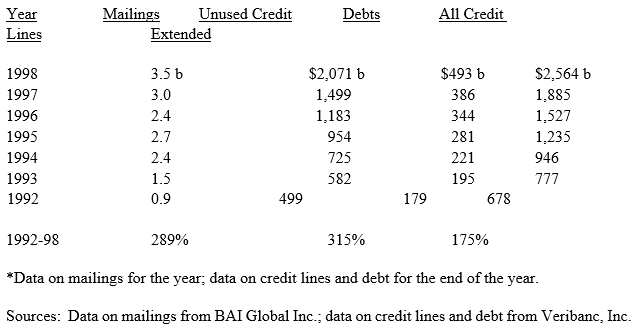

Despite complaints to Congress that bankruptcy restrictions are needed because some consumers borrow irresponsibly, credit card issuers have dramatically expanded their marketing and credit extension. More than 80 percent of credit card debt has been extended by banks (including their securitized debts). The following table shows that, in the 1990s, bank card solicitations and unused credit lines have risen far more rapidly than bank card debt — 289 percent and 315 percent compared to only 175 percent. All figures below are in billions.

As a result of this aggressive marketing and extension of credit, it is no surprise that a large majority of the public believes that credit card issuers share responsibility, with debtors, for the increase in personal bankruptcies. In the April 1999 Opinion Research Corporation International survey, 74 percent said that credit card issuers were responsible, while only 22 percent said these issuers were not at all responsible.

Bank Credit Card Profits Increase

After declining from the early to the late 1990s, bank credit card profits have begun to rise. According to the March 23, 1999 issue of Card Fax, an industry newsletter, the FDIC reports that after-tax return on average assets for credit card banks rose from 2.09 percent in 1997 to 2.84 percent in 1998, a 35.9 percent increase.

An important reason for this increase in profitability is more aggressive marketing to low-and moderate-income households. That has been an emphasis at Sears, which in 1998 earned two-thirds of its profits from credit cards. That has also been the key strategy of Metris, which now dominates the credit marketplace for lower income households. Today, a Metris stock share is 200 percent higher than it was in 1996, when it was first issued. (Wall Street Journal, December 29, 1998, A1)

There are several reasons credit card profitability has risen. Interest rate spreads have increased. So have fees, which now typically range from $25 to $29 for late payments and going over the credit limit. And, while promotional and permanent interest rates have declined, penalty rates usually exceeding 20 percent have been introduced and assessed with increasing frequency. Finally, it appears that bankruptcy rates have begun to decline.

Personal Bankruptcy Rates Begin to Decline

The April 1999 issue of the American Bankruptcy Institute Journal reported that personal bankruptcy filings dropped dramatically nationwide in January and February of this year. That follows a decline in the growth of the personal bankruptcy filing rate per thousands population to only 1.5 percent in 1998 (and to 1.0 percent in its last quarter). (Lawrence M. Ausubel, “A SelfCorrecting ‘Crisis’: The Status of Personal Bankruptcy in 1999,” paper issued by the Department of Economics, University College London on March 10, 1999)

Debt and Bankruptcy Trends Raise Questions About Proposed Restrictions on Personal Bankruptcies

If credit card issuers continue to aggressively market and extend credit, especially to the least affluent; if these issuers make higher profits; and if consumers exercise restraint in taking on new credit card debts and in filing for bankruptcy, then how can new creditor-sought restrictions on personal bankruptcy be justified? In fact, some experts like Ausubel have argued that these restrictions would aggravate the consumer debt crisis by encouraging lenders to extend even more credit knowing that it would be more difficult for borrowers to default through bankruptcy.

Public Strongly Supports Inclusion of New Consumer Protections in Bankruptcy Legislation

In the Congressional debate over bankruptcy, pro-consumer legislators have proposed two new consumer protections. One would require credit issuers to tell all cardholders, if they made only the minimum payment — usually 2% or 3% of the oustanding debt — how long it would take to pay off the debt and how much interest would be owed. The other protection would require people under 21 who wish to get their own credit card either to obtain parental approval or to demonstrate to the credit issuer that they can make payments on their own.

In the April 1999 Opinion Research Corporation International survey, the public strongly backed both consumer protections. 85 percent supported the disclosure requirement with only 11 percent opposing this measure. Of the supporters of the requirement, about three-quarters strongly supported it (63 percent of all respondents).

Support for restricting the distribution of credit cards to persons under 21 received support that was almost as strong. 80 percent supported this measure with only 17 percent opposing it. What is especially significant is that 79 percent of those respondents aged 18-24 supported this reform. That is, an overwhelming majority of many of those who might be denied cards supported the measure.