Credit Card Issuers Aggressively Expand Marketing and Lines of Credit on Eve of New Bankruptcy Restrictions

As a creditor-funded campaign to restrict consumer access to bankruptcy approached passage in Congress, the Consumer Federation of America (CFA) released data that show that credit card issuers dramatically increased their marketing and credit extension last year. These factors, along with a drop in debt losses and consumer bankruptcies, were key reasons for profits that have increased by nearly 50 percent in two years and are at a five-year peak.

“Credit card issuers are brazenly lobbying for new bankruptcy restrictions at the same time their aggressive marketing and lending practices are pushing many families closer to the financial brink,” said Travis Plunkett, CFA’s legislative director. “While the issuers urge Congress to deny families access to bankruptcy relief, their profits are soaring.”

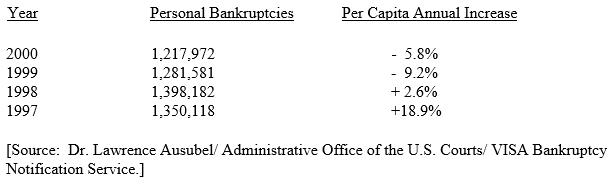

The Consumer Federation of America also released figures compiled by University of Maryland economist Lawrence M. Ausubel that reveal that bankruptcies fell sharply for the second year in a row. The per capita personal bankruptcy rate has declined by 15% since the end of 1998.

“The bankruptcy legislation is the wrong bill at the wrong time,” said Professor Ausubel. “There cannot be a worse time to enact a harsh bankruptcy bill than when the President warns the American people of an impending economic slowdown. In the longer term, the bill will also encourage lenders to lower their credit standards further and solicit riskier customers, increasing the number of badly-overextended consumers in the country.”

Issuers Expand Marketing and Credit Lines Faster Than Consumers Increase Borrowing

Last year, bankcard issuers responded to declining direct mail responses and moderate increases in credit card debt by sharply increasing their marketing and credit extension. (Banks extend the overwhelming majority of credit offered through credit cards.) The surge in industry profits in 2000 also fueled increasing marketing and credit extension.

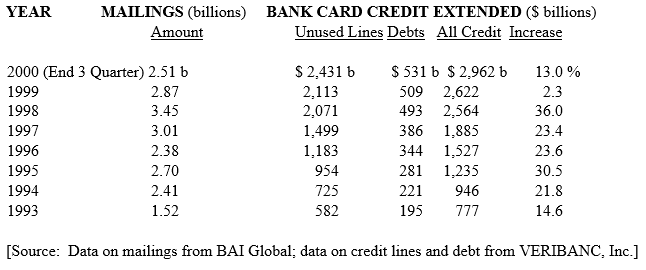

Total credit extended, which includes unused credit lines and debt incurred by consumers, approached three trillion dollars for the first time ever. Total credit increased by 13 percent during just the first nine months of 2000, which projects to a 17 percent increase for the entire year. Most of the increase in total credit extended can be attributed to credit extended by issuers ($340 billion increase for the first three quarters) as opposed to debt incurred by consumers ($22 billion increase).

Mailings remain the single most important way for issuers to market their credit cards, accounting for about three-quarters of all cards sold. Mail solicitations through the third quarter of 2000 were 2.5 billion, which projects to 3.3 billion for the entire year. This is a 14 percent increase over the number mailed in 1999. Credit card mailings declined quarter-to-quarter from 955 million in the second quarter of 1998 to 510 million in the fourth quarter of 1999, which was the lowest quarterly level in four years. Mailings then surged to their highest level ever of 991 million in the second quarter of 2000 and stayed high in the third quarter (880 million). [Source: BAI Global]

Industry Profits Surge

Fewer bad debts and personal bankruptcies and an increase in income from fees drove bank card profits to the highest level in five years in 2000. Pre-tax return on assets (ROA), an important measure of profitability, was 3.6 percent in 2000. These profits represent a 16 percent increase over 1999 (3.1 percent ROA) and 44 percent more than 1998 (2.5 percent ROA). Profits haven’t been this high since 1995 (3.6 percent ROA). Issuers have continued to increase the number and amount of fees. Fee income contributed to 28 percent of profits in 2000, up from 24 percent in 1999. [Source: R.K. Hammer, Investment Bankers]

Consumers Exercise Restraint in 2000: Bankruptcies and Responses to Direct Mail Decline

Personal bankruptcies dropped for the second year in a row. The bankruptcy rate is now lower than before bankruptcy legislation was introduced in Congress in early 1997.

Given the sharp decline in personal bankruptcies, it is not surprising that credit card lenders saw net chargeoffs—the proportion of debt losses to outstanding debt—decline again. Net chargeoffs at the end of the third quarter 2000 were 1.05 percent. This rate is lower than at the end of the third quarter of 1999 (1.07 percent) and a substantial 30 percent lower than at same time in 1997 (1.37 percent). [Source: VERIBANC]

Despite the increase in credit extended, consumers are increasingly saying no to credit card solicitations. The response rate has declined from 2.8 percent in 1992 to .6 percent for the first three quarters of 2000. The response rate of .4 percent in the second quarter of 2000 was the lowest in the past decade. [Source: BAI Global]

Consumer restraint in 2000 was also evidenced by the fact that bank card issuers extended credit at a faster rate than consumers assumed debt. During the first three quarters of the year, unused credit lines increased by 15 percent (from $2.11 to $2.43 trillion), while consumer debt increased by only 4 percent (from $509 billion to $531 billion). [Source: VERIBANC]

Severe Bankruptcy Restrictions Near Passage

Credit card lenders have been the most vigorous supporters of bankruptcy legislation (S. 220/ H.R. 333), which is scheduled to be debated in the Senate Judiciary Committee and on the House Floor this week. President Bush has indicated that he is supportive of the bill. Public interest organizations, academic scholars and bankruptcy practitioners oppose this legislation because it does not balance responsibility between working families and creditors, whose practices have contributed to the rise in bankruptcies.

The legislation would not curb aggressive lending practices by the credit industry or provide adequate information to consumers about the cost of carrying credit. Proposed amendments that would target abusive lending practices involving college students, predatory mortgage loans and high-cost “payday” loans are not included. The bill allows lenders to provide only very general information on the credit card statement about the cost of paying the bill at the minimum rate.

It would make it harder for modest-income Americans to get a fresh start in bankruptcy. The “one size fits all” means test to determine which debtors can liquidate some debts in chapter 7 bankruptcy is arbitrary and inflexible. It eliminates the ability of bankruptcy judges to make decisions that take into account individual family needs for expenses like transportation, food and rent.

It bill would increase the number of consumers who fail to complete 13 bankruptcy. The bill is supposedly designed to require more debtors to use chapter 13 bankruptcy, where they must repay more of their debt than in chapter 7. However, experts estimate that the number of people who will fail to complete a chapter 13 “reorganization” bankruptcy would increase by at least 20 percent under the bill. The failure rate in chapter 13 bankruptcy is already two-thirds of those who file. The bill’s “cramdown” provision alone would make it much harder for families to use chapter 13 to save their homes and cars.

Onerous legal and paperwork burdens in the bill will disadvantage cash-strapped families who cannot afford expensive legal assistance. Cumbersome informational requirements would substantially increase the cost of accessing the system for families who are most in need of debt relief and financial rehabilitation. These paperwork requirements would apply to all debtors, even lower-income debtors. The bill provides creditors with a variety of new opportunities to file legal motions challenging the liquidation of debts; motions that financially-pressed families would likely agree to because they cannot afford to challenge them. The bill also eliminates provisions of the law that allow families to catch up on rent and avoid eviction.

It would compromise the payment of high-priority debts after bankruptcy, such as child support and alimony, by increasing the amount of debt for which consumers are liable. The legislation would result in many new “nondischargeable” debts that must be paid to credit card companies. It would give creditors new leverage to coerce “reaffirmation” agreements that require the debtors to remain legally liable for more consumer debts even after they declare bankruptcy. These provisions would affect debtors of all incomes who file for bankruptcy.

It would allow wealthy debtors to keep expensive homes while filing for bankruptcy. Those declaring bankruptcy could retain homes of unlimited value in five states, including Florida and Texas, as long as the debtor owned the property for two years before declaring bankruptcy.

The Most Important Thing Congress and Issuers Could Do to Accelerate the Decline inPersonal Bankruptcies

While personal bankruptcies would continue to decline if consumers and creditors exercise greater restraint, this decline would, over time, certainly accelerate if credit card issuers were to phase in an increase in the minimum payment allowed from 2-3 percent to 4 percent.

“The decline in the typical minimum payment to 2 or 3 percent is responsible for much of the rise in consumer bankruptcies through the past decade,” noted Stephen Brobeck, CFA executive director. “That low minimum payment, which barely covers interest obligations, convinces many borrowers that they are okay as long as they can meet all their minimum payment obligations. But those that cannot afford to make these payments carry so much debt that bankruptcy is usually the only viable option.”

In the past few years, lenders have expressed surprise and dismay that they can no longer reliably predict which borrowers will end up in bankruptcy. That is because low minimum payments allow insolvent borrowers to pay all their credit card bills on time. But at a certain point they realize their situation is hopeless and declare bankruptcy. (At 2 percent, monthly credit card payments totaling $400 represent $20,000 of credit card debt.)