Washington, DC — The Consumer Federation of America (CFA) today released the results of a national poll showing that consumers overwhelmingly want limits and additional disclosures on bank overdraft fees. While the Federal Reserve is implementing new rules requiring banks to gain the consent of their customers prior to enrolling them in a debit card overdraft program, the new rules do nothing to rein in high fees or provide real-time disclosures.

“There is strong support among Americans for Congress to finish the job, begun by the Federal Reserve, to protect consumers from unfair overdraft fees and practices,” said Jean Ann Fox, director of financial services for Consumer Federation of America (CFA). Both the House and Senate banking committees held hearings late last year on legislation that would curb the cost and frequency of fees, prohibit banks from manipulating the processing of payments to drive up overdrafts, and provide a warning at the ATM before a transaction triggers an overdraft fee.

“The Federal Reserve‟s recent rules address only consumer consent on certain types of overdrafts – they do nothing to get at the substantive problems with today‟s overdraft product, particularly the cost and frequency of these fees,” said Rebecca Born, Policy Counsel for the Center for Responsible Lending (CRL). “Initial consent is only a baseline protection.

Consumers „consented‟ – signed on a line somewhere – to most abusive credit products extended over the last several years. That doesn‟t mean that any credit terms, no matter how outrageous or irresponsible, should be fair game.”

“Changes to bank overdraft programs announced by some of the largest banks last fall have not cut the steep cost of overdraft fees or provided consumers real control over their checking accounts,” noted Ms. Fox. “Under the most restrictive voluntary limit of three overdraft fees per day, a consumer could still rack up 90 $35 overdraft fees per month for a total of $3,150. That‟s an exorbitant amount of money for overdraft fees, and that‟s why we need Congress to rein in these practices.”

CRL estimates that consumers paid $23.7 billion for overdraft fees in 2008, an increase of 35 percent over just two years. CRL reported that 50 million Americans overdrew their checking accounts at least once over a 12-month period with 27 million accountholders paying five or more overdraft or insufficient funds fees per year.

“The failure of the Federal Reserve to protect consumers from abusive overdraft fees also demonstrates that Americans need the Consumer Financial Protection Agency, currently being considered in the Senate, to monitor bank fees and ensure that they are fair for the long term,” Ms. Fox said.

Bank Overdraft Fees and Practices

In January 2010, CFA reviewed bank fee schedules from fifteen large consumer banks and found that the largest banks continue to charge steep fees, pile on extra fees when overdrafts are not repaid within days, and charge multiple fees per day.

High fees: Big bank overdraft fees range from a low of $19 for the first U.S. Bank overdraft in a year to $39 charged by Citizens Bank after a customer has overdrawn twice in one year. The typical highest fee is $35 per transaction that overdraws an account. Eight of the largest banks charge a flat overdraft fee, regardless of the number of times a customer overdraws in a year. Tiered fees are charged by seven of these banks. For example, Fifth Third Bank charges $25 for the first overdraft, $33 for two to four overdrafts, and $37 each if a customer overdraws five or more times in a year. Wachovia charges $22 for the first overdraft and $35 for subsequent ones.

Overdraft fees bear no relationship to the amount of credit extended when banks cover overdrafts. According to the FDIC, the typical debit card overdraft is $20, far less than the typical $35 fee big banks charge per overdraft. There are currently no limits on the dollar amount that banks may charge when customers are permitted to overdraw an account.

Several banks have recently set thresholds for total dollars overdrawn per day before fees are triggered. For example, Bank of America does not charge fees unless the total dollars overdrawn at the end of the day exceed $10. U.S. Bank announced a $10 trigger for overdrafts to be implemented early in 2010. Some banks announced a $5 total overdrawn per day trigger, including BB&T, Capital One, Chase, Regions and Wells Fargo. Because these thresholds are very low and apply only to the total amount overdrawn per day (as opposed to applying to each individual overdraft transaction), they are not likely to provide much relief to customers who overdraft.

Frequent fees and limits: Sixty percent of the largest banks charge additional fees when the overdraft and original fee are not repaid within days. TD Bank adds $20 if an overdraft is not repaid in ten days. In some states, Chase adds up to $25 after five days while Bank of America adds a second $35 fee if the overdraft is not repaid in five days. SunTrust adds another $36 fee on the seventh day and BB&T charges a $30 “Overdrawn Account Collection Fee” on the fifth day the account is overdrawn. Other banks impose per day fees for sustained overdrafts; for example, Fifth Third charges $8 per day after an overdraft is unpaid for three days.

The combination of original and sustained overdraft fees escalates the cost of a single overdraft to consumers. In addition to the initial $36 overdraft fee, PNC Bank charges $7 per day after four days up to a maximum $98. A PNC customer with one $20 overdraft unpaid in two weeks could be charged $134. Citizens Bank charges two sustained overdraft fees of $35 each if the overdraft and fees are not repaid in ten days for a total of up to $109 for a single overdraft.

About half the banks impose daily limits on the number of overdraft fees they will charge, ranging from three per day announced by Chase to six per day at TD Bank. Under the most restrictive voluntary limit of three fees per day, a consumer could incur 90 overdraft fees per month, not counting any sustained fees. By contrast, the new Credit CARD Act limits credit card issuers to one over-the-limit fee in a month when consumers opt in to having transactions paid that exceed their limit. There is no parallel limit on the number of overdraft fees banks can charge.

Transaction ordering to maximize fees

Financial institutions can manipulate the order in which withdrawals are posted in order to trigger more overdraft fees. Large institutions usually clear the largest transaction first, causing more transactions to overdraw the account. This practice generates more in overdraft revenues because the institution can charge an overdraft fee for each transaction once the account is below zero. Among the large banks announcing changes to their practices, Chase announced that it would process payments in real time in the order received by the bank. We are aware of no other banks that have committed to this change.

Congressional Legislation Would Protect Consumers

Pending legislation in Congress introduced by Senator Christopher Dodd (S. 1799) and Representative Carolyn Maloney (H.R. 3904) would address the fundamental and pervasive problems with overdraft loans today – namely, their high cost and the frequency with which fees are charged. The bills would require that overdraft fees be reasonable and proportional to the institution‟s cost of covering the overdraft. They would limit overdraft fees to one per month and six per year; after these limits are reached, institutions could continue charging for overdrafts but only through a lower cost program like an overdraft line of credit. The bills would also prohibit institutions from manipulating the order in which they post purchases in order to maximize fees and require a real-time warning at the ATM before an overdraft fee is triggered.

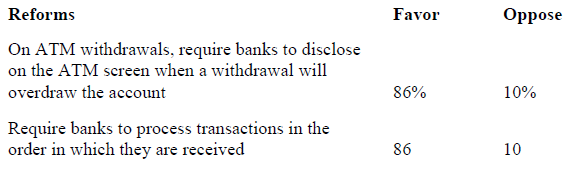

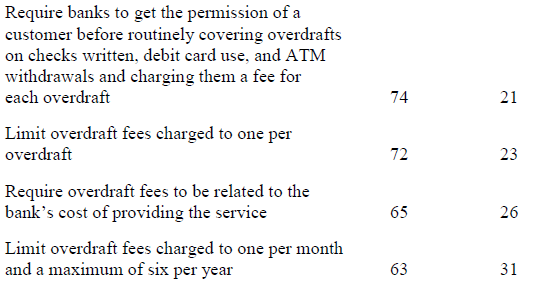

Consumers Strongly Favor Reform

A survey of 1,015 representative adult Americans, commissioned last month by the Consumer Federation of America, revealed strong support for new overdraft fee protections. By margins ranging from two to one up to eight to one, respondents indicated that they favored a half-dozen new overdraft fee protections that were not included in the Federal Reserve‟s new rules but that are now being debated in Congress.

“New overdraft fee protections are desired by a large majority of all Americans and particularly by middle income families,” said Fox. All demographic groups related to factors including age, income, education, ethnicity, and household character support these reforms, but those with incomes $75,000 to $100,000 are especially supportive. Overdrafters supported reforms at about the same high level as respondents who don‟t overdraw their account.

The survey also asked respondents whether they had overdrawn their checking account in the past year. Nearly one-third (31 percent) of those with such a checking account said that they had. Surprisingly, a significant minority of all demographic groups had overdrawn checking accounts. However, young adults age 18-34 (74 percent) and families with children (41 percent) were especially likely to report they had overdrawn their account. It is also interesting that young adults were particularly likely to support limiting overdraft fees charged to one per month and six per year.

The survey was conducted for CFA January 18-21 by Opinion Research Corporation using telephone interviews. The margin of error is plus or minus three percentage points. The survey data is available to the press.

Recommendations

CFA and CRL support swift passage of H.R. 3904 and S. 1799 to protect consumers from astronomically expensive overdraft traps and tricks. By requiring banks to get consumers‟ affirmative consent to having overdrafts paid for a fee for all types of transactions and setting limits on the cost and frequency of overdraft fees, Congress can put bank account control back into the hands of consumers and save families up to $24 billion a year now paid for overdrafts.

Later this year, banks will have to get affirmative consent from new and existing accountholders before routinely paying for a fee debit card purchases and ATM withdrawals despite insufficient funds. CFA and CRL recommend that banks simply deny these electronic overdrafts at no cost to consumers. And, until Congress acts on a full slate of reforms, we recommend that consumers say “ no” to their banks‟ debit card overdraft programs and ask that their banks let them opt-out of overdraft programs altogether.

To protect against insufficient funds fees, consumers can request to have their checking account linked to a savings account, credit card, or line of credit to get lower cost protection.