Washington, D.C. – Consumer Federation of America (CFA) and the Center for Economic Justice (CEJ) called in mid-March for auto insurance relief in the wake of reduced driving due to COVID-19, and on April 6 the first insurance company refunds were announced. Since then most major insurers have responded with a wide variety of relief programs, and today CFA and CEJ are releasing an updated Report Card grading the insurance companies.

“With the changes brought on by Stay at Home orders, insurance companies need to return billions that drivers have overpaid as a result of COVID-19. We are grading insurance company actions to make sure consumers get the refunds they deserve,” said J. Robert Hunter, Director of Insurance for CFA and former Texas Insurance Commissioner.

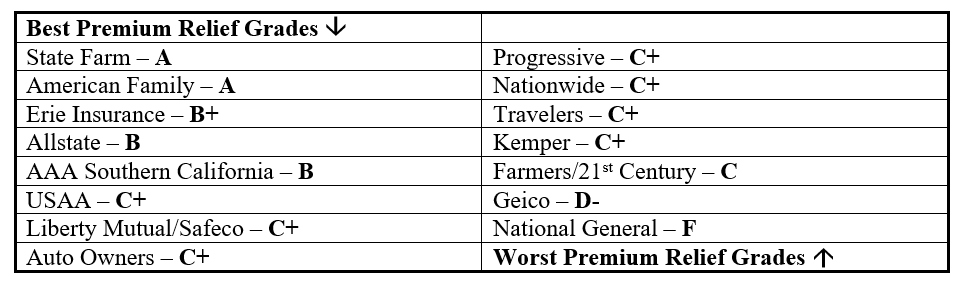

The updated Report Card now shows the following grades for the nation’s 15 largest insurers:

View the complete updated scorecard sorted by Company Market Share or by Grade.

Updating their April 13, 2020 scorecard, the groups highlighted the following:

- Some major insurers have still not taken action to provide premium relief: National General, Sentry, Alfa and Texas Farm Bureau received an F.

- Erie improved from F to B+ by changing course and providing immediate relief instead of a vague promise of future relief. Erie has promised to pay dividends in an industry-leading amount of 30% of two months premiums and now has one of the top 5 grades.

- Additional insurers have announced actions including the Auto Clubs (AAA), MAPFRE, Southern Farm Bureau, American National, Country Financial and Selective.

- West Bend’s and Hanover’s grades improved after the insurers provided clarifications of their relief programs.

The groups noted that a number of smaller insurers have also announced relief but are not included in the Scorecard. The scoring methodology and detailed grade report are here.

CFA and CEJ calculate that the relief promised for March, April and May now exceeds $7 billion. But, according to the groups, that is not nearly enough as the drop in auto insurance claims is far greater.

“For those insurers providing premium relief, the relief ranges from just over 10% to 35% of two months premium with the vast majority of insurers providing only 15%. With some data showing motor vehicle accidents down 50% or more,[i] more relief is needed for March, April and May from nearly all insurers,” said Hunter. “It’s clear that premium relief of 30% or more will be needed for these months.”

The groups had previously published a chart showing how different reductions in auto insurance claims should translate into premium relief.

“Auto insurance is regulated by the states and state laws require auto insurance rates to be cost-based and not excessive,” said Birny Birnbaum, Executive Director of CEJ. “That means insurers must provide the auto premium relief because the rates based on pre-COVID-19 restrictions have become excessive. State insurance regulators have been largely absent on providing guidance to auto insurers on the amount of needed premium relief and have provided no longer-term plan for insurers to address ongoing relief for what will be a slow economic recovery.”

What Do Consumers Need to Do?

The auto insurance premium relief announced by insurers is based on an overall reduction in claims because of fewer people on the road and fewer miles driven. This is relief given to all policyholders because of the overall reduction in claims paid by insurers. This “aggregate” relief to all policyholders is different from a lower rate for an individual driver whose driving has dropped because of COVID-19 impacts. CFA and CEJ provided this advice to consumers:

- If your individual driving has changed dramatically, contact your insurance company or insurance agent and ask to be “re-rated” at your lower mileage. This is different relief from the relief promised by many insurers.

- Check your insurer’s website for information on the “aggregate” premium relief the insurer is offering. Most insurers providing relief will do so automatically and don’t require the policyholder to take action. If you’re not sure if the “aggregate” relief is automatic, contact your insurer to make sure you are getting the relief.

- If you don’t find any information on the “aggregate” relief, contact your insurer and demand the premium relief that other insurers are providing.

[i] For the period ending April 4, the Massachusetts State Policy reported a 58% reduction in accidents. See https://www.wcvb.com/article/massachusetts-insurance-companies-rolling-out-coronavirus-rebates-discounts/32111638 Similarly, University of California at Davis estimates that car crashes in California are down 50%. See https://roadecology.ucdavis.edu/files/content/projects/COVID_CHIPs_Impacts_updated_415.pdf