How Auto Insurers Overcharge Drivers in New Jersey Based on Their Credit Scores, Education, and Jobs

Yesterday consumer advocates held a press conference on the steps of the New Jersey statehouse to draw attention to a major problem: auto insurers’ use of unfair factors to discriminate against drivers and charge them higher premiums. As a result, people have wound up paying hundreds or even thousands of dollars more for auto insurance, even if they have a perfect driving record.

How does this work? Insurance companies use a variety of different factors to calculate your premium, including how much you drive, any tickets you receive or accidents you get into, and any claims that you file. But they also quietly use non-driving socioeconomic factors—including your credit score, your education level, and the type of job you have. Insurers use these qualities as proxies for income to discriminate against lower-earning consumers in favor of wealthier people who can easily afford additional insurance products.

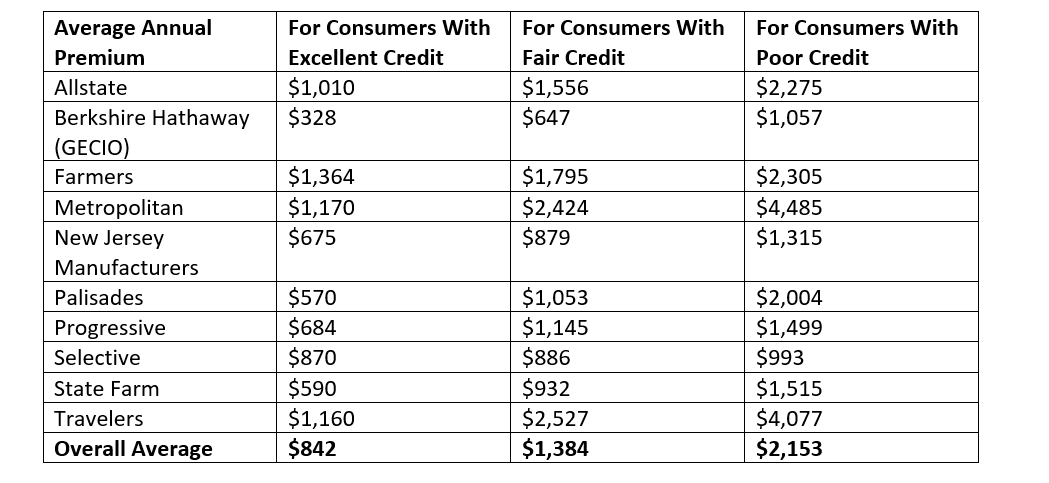

And the results are dramatic. Consumer Federation of America conducted an analysis of average premiums in New Jersey charged by ten of the largest auto insurers in the state, representing the vast majority of the market. Statewide, consumers with excellent credit scores and perfect driving records pay an average annual premium of $842. But if they have fair credit, they pay on average $1,384. And consumers with poor credit pay on average $2,153—that’s over $1,300 more or a 156% increase!

As shown below, all of the largest auto insurers practice this discrimination.

Consumers in New Jersey with poor credit are paying over $1,300 more for auto insurance annually consumers with excellent credit. Renee Koubiadis of New Jersey Citizen Action pointed out that “you can have a doctor or a lawyer or some other kind of professional who has a worse driving record, even a DUI sometimes, who are paying lower rates than someone in a low wage occupation with bad credit or fair credit. That's taking away income from them to be able to save up, to buy a house or send a child to college, or even, from day-to-day, from putting more food on the table or getting needed medications or other medical care.” Other consumer groups also emphasized that although many people don’t think about insurance that much, this is a kitchen table issue with real consequences for families.

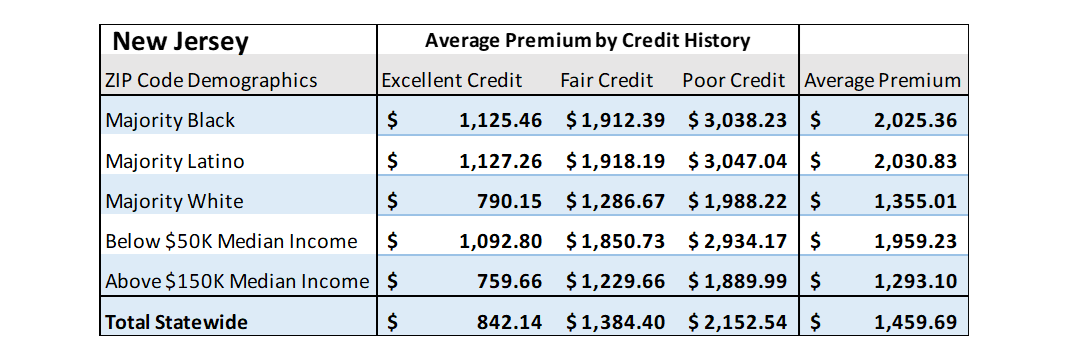

Evidence also shows that New Jersey drivers pay higher premiums based on the demographics of the ZIP codes where they live. Drivers living in majority Black or Latino areas pay hundreds of dollars, sometimes over a thousand more, than drivers living in majority white ZIP codes.

Investigations by Consumer Reports found similar results when auto insurers use people’s education levels and jobs to calculate insurance costs—people who earn lower wages and are less educated pay more. And most consumers don’t even know that auto insurers use their credit scores, education levels, and jobs to charge them higher premiums. When they discover this, most consumers strongly oppose the use of these factors.

Since New Jersey requires drivers to have auto insurance the Department has a responsibility to make sure auto insurance is affordable. But by allowing auto insurers to overcharge consumers using these factors, New Jersey is letting insurers make auto insurance expensive and even unaffordable for many consumers. They then must struggle to pay their premiums or illegally drive without insurance.

Fortunately the New Jersey Department of Banking and Insurance can fix this problem. In April thirty six organizations—consumer groups, community advocates, civil rights groups—sent a letter to the Department urging them to ban the use of credit scores, education, and occupation in auto insurance. New Jersey law says that rates should not be excessive, inadequate, or unfairly discriminatory, and the Department has the power to enforce these provisions. Several other states already ban these factors, reducing costs for consumers, and insurers operate perfectly well there.

For too long, low-income consumers have struggled to afford auto insurance. Your premium should be based on your driving record, not on your credit score or your job or whether you want to college. The Department must ban the use of credit information, education, and occupation in auto insurance pricing, and they should ban it now.