Deregulatory Agenda on Display in House Committee Markup is Anti-Investor and Anti-Consumer

On April 26, the House Committee on Financial Services conducted a “mega” markup to consider dozens of anti-investor/anti-consumer bills. Many of the bills considered aim to further expand private capital markets at the expense of our public capital markets and to expand the pool of investors that can be sold private securities without the protections afforded by the public markets.

In advance of the markup, CFA sent a letter of strong opposition to many of these bills, including opposition to a “bipartisan” package of bills that, in part, would expand the “Accredited Investor” definition, the boundaries of which delineate which investors may be sold unregistered, private securities.

CFA also strongly opposed the antithetically-named “Improving Disclosure for Investors Act of 2023” (H.R. 1807), a bill that would severely diminish the effectiveness and accessibility of critical investor disclosures by defaulting investors into receiving them electronically, even when investors have shown a clear preference for receiving disclosures in paper. And finally, CFA wrote to oppose a package of partisan bills, the “Expanding Access to Capital Act” (H.R. 2799), that would recklessly expand private markets and diminish investor protections across the board, and another package of bills intent on defanging the Consumer Financial Protection Bureau (CFPB), entitled the “CFPB Transparency and Accountability Reform Act” (H.R. 2798).

Accredited Investor Definition

Notably, the bipartisan package of bills considered during the markup included a bill, “the Fair Investment Opportunities for Professional Experts Act” (H.R. 835), that would enshrine in statute the Securities and Exchange Commission’s accredited investor definition, one for which there is ample evidence showing that it is ineffective in defining a population of investors capable of truly fending for themselves without the protections afforded in the public market.Coincidentally, the bill’s lead sponsor, Rep. French Hill (R-AR), said exactly this during debate of the bill, stating that “wealth is not correlated with wisdom” and, moments later, “I don’t think smart investing is correlated with wealth.” Moreover, the bill would expand the definition to include individuals who have “demonstrable education or job experience to qualify such person as having professional knowledge of a subject related to a particular investment.” It’s not clear who would qualify under such a test or whether or how that person would have access to the information necessary to evaluate an investment and value any particular private securities. Troublingly, members of the committee opined that merely having a professional degree or certification, like investors with an MBA or law degree, or those who are a Certified Public Accountant (CPA) or even a “young PhD medical doctor,” to quote Rep. Hill, should qualify an investor to purchase private securities. All of these examples, and others that were floated during debate, are unproven and likely ineffective proxies for the sophistication necessary to fend for one’s own in private securities markets. And sadly, this bill is but one of several other problematic accredited investor-related bills that advanced on a bipartisan vote.

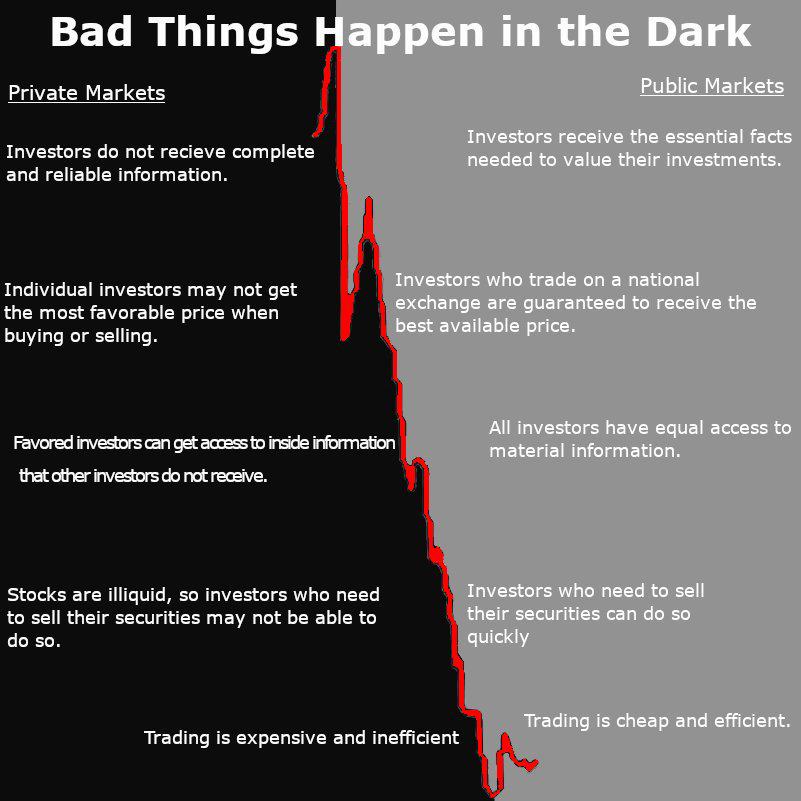

Private Market Deregulation

Even more unfortunately, these bills and others considered during this markup clearly illustrate the Committee’s recent and dramatic turn toward a deregulatory agenda that has occurred under Rep. McHenry’s (R-NC) chairmanship of the full committee and Rep. Ann Wagner’s (R-MO) leadership on the capital markets subcommittee. This pivot toward expanding private markets at the expense of public markets was made most evident by the “Expanding Access to Capital Act of 2023” (H.R. 2799). This package of more than a dozen partisan bills would expand private market exemptions, expand the accredited investor definition, and otherwise erode or negatively impact investor protections and public markets.It is of profound concern that a significant part of the committee’s legislative agenda will apparently be to further deregulate our capital markets and expand the loopholes that have allowed private market capital raising to eclipse capital raising in public markets, the continuation of a troubling trend that has bedeviled investor protections and market integrity for decades. Private markets lack transparency, have limited regulatory oversight, and contain weak fraud prevention mechanisms, and the committee should be focused on minimizing the harms retail investors suffer when exposed to them—unfortunately, this markup displayed an intent to do just the opposite.

State Activity

The U.S. Congress, however, isn’t the only venue where efforts to expand the sales of private market securities to retail investors are occurring. For example, Nevada’s Assembly recently saw passage of Assembly Bill 75 (AB75), which would create an exemption to the federal securities laws for intrastate securities offerings to “Nevada certified investors.” In partnership with the University of Nevada School of Law’s Public Policy Clinic, CFA wrote to members of the Nevada legislature to oppose this bill, as it would expose Nevadans to the most speculative, risky, and illiquid securities, and would open the door to substantial fraud and abuse.What’s Next?

For the bills that received bipartisan support, it is expected that they will move relatively quickly, and may advance to a floor vote in the House via “suspension of the rules.” For reference, the House suspension calendar is typically used to fast-track bipartisan, noncontroversial bills, meaning they do not have to go through the Rules Committee and the House does not need to adopt a rule to debate them, sidestepping procedural hurdles that commonly slows legislation in the House.Other bills that advanced, however, including both the “Expanding Access to Capital Act” (H.R. 2799) and the “CFPB Transparency and Accountability Reform Act” (H.R. 2798), were advanced on a party line vote and therefore will likely have a more uncertain path through the legislative process.

And finally, one portion of the committee’s markup that deserves highlighting occurred during a colloquy between members while debating the “Improving Disclosure for Investors Act of 2023” (H.R. 1807): prior to passage of the measure (by voice vote), Ranking Member Maxine Waters (D-CA) was able to secure commitments from Chair McHenry and the bill’s lead sponsor, Rep. Bill Huizenga (R-MI), for further negotiations with Democratic members to determine the final version of the bill that would be brought to the House floor. This could provide a critical opportunity to amend the bill’s most problematic features.

Conclusion

As these bills and others are deliberated further in both the House and the Senate, CFA will continue working to ensure that consumers’ interests are promoted, investor protections are preserved, and both public and private markets operate with integrity and transparency.