Consumer Champions Chosen for Two Key Financial Regulatory Posts

On the eve of Inauguration, the Biden-Harris Transition Team announced that it had selected leading consumer champions – Rohit Chopra and Gary Gensler – to head two key financial regulatory agencies, the Consumer Financial Protection Bureau (CFPB) and the Securities and Exchange Commission (SEC) respectively. Both are subject to confirmation in the Senate before they can assume their new roles.

Chopra, who is currently serving as a Commissioner at the Federal Trade Commission (FTC), is being nominated to serve as Director of the CFPB, an agency he helped to launch and where he previously served as assistant director heading up the agency’s efforts to address student lending abuses. Between his stints at the CFPB and the FTC, he served as a senior fellow at CFA, where his work focused on consumer protection issues facing young people and military families.

“Rohit Chopra is an incredibly strong pick to lead the CFPB. Commissioner Chopra has deep experience relevant to leading the CFPB effectively: leading student lending protection efforts at both the CFPB and at the Department of Education; and deep consumer protection and enforcement experience as a Federal Trade Commission Commissioner,” stated CFA Legislative Director and General Counsel Rachel Weintraub. “Commissioner Chopra has the experience, knowledge and commitment to consumer protection to lead the CFPB and help it realign its work with the mission of the agency, which is to make the financial marketplace fairer for consumers.”

Gensler, who has previously served in the Treasury Department under President Clinton, as a senior adviser to Sen. Paul Sarbanes during the drafting of the Sarbanes-Oxley Act, and as Chairman of the Commodity Futures Trading Commission (CFTC) during the Obama Administration, is being nominated to serve as Chairman of the SEC. During his time as CFTC Chair, Gensler earned the respect of investor advocates for his willingness to write the tough rules necessary to rein in industry excesses and to do so in a way that could withstand industry legal challenge.

“We could not have asked for a better candidate to fill this post,” said CFA Director of Investor Protection Barbara Roper. “Gary is as knowledgeable about the markets as any Wall Street insider, but his commitment to investor protection is well established and unwavering. He is a seasoned regulator who knows how to get things done and isn’t afraid of a fight,” she added. “That’s going to be essential, because there’s a lot of damage to undo at the SEC, both to reverse anti-investor policies and to restore the integrity of the regulatory process. It’s a daunting task, but Gary’s the perfect person to roll up his sleeves and get the job done.”

FTC Asked to Investigate Amazon Prime’s Anti-Cancellation Tactics

According to a new report released earlier this month, Amazon Prime’s business model uses “dark patterns,” or manipulative design choices, to thwart attempts to cancel the service. CFA and six other advocacy groups wrote to members of the Federal Trade Commission (FTC) urging it to launch an investigation.

According to the groups’ letter, the results of the report point to a single conclusion, that “Amazon Prime’s subscription model is a ‘roach motel,’ where getting in is almost effortless, but escape is an exhausting ordeal.” The practices Amazon uses in this business model include “forced continuity programs that make it difficult to cancel charges, trick questions to frustrate user choice, and free trials that automatically convert into paid memberships.” According to the groups, this violates a consumer’s right not to be charged for products sold through online negative options without a simple cancellation mechanism.

The groups urged the FTC to launch an investigation into these practices to determine if Amazon violated Section 5 of the FTC Act, as well as the Restore Online Shoppers’ Confidence Act (which requires “simple mechanisms” to stop recurring charges), and the CAN-SPAM Act’s prohibition of deceptive subject headings.

“Consumers are vulnerable to being unknowingly enrolled into automatically renewing subscriptions, often from free trial offers, that are disproportionately difficult to cancel due to conscious design choices which attempt to delay or redirect user choice. Along with a subscription fee, users trapped by this model can also be forced to give up sensitive personal data like contacts, messages, or location without their meaningful consent or knowledge,” the groups stated in a separate letter to the U.S. Senate and House of Representatives.

The groups provide some examples of a few of the ways that these “dark patterns” tip the scales against ordinary consumers:

- “User interfaces can be employed to steer consumers into prioritizing Amazon’s preferred choices over others, to hide or omit relevant information, or to otherwise trick, confuse, or frustrate users.”

- Amazon misdirects consumers and challenges their choices through negatively charged statements intended to discourage users from attempting to stop paying for the service, and it employs graphic designs that may steer users away from unsubscribing through a variety of “visual interference” techniques.

- Before cancelling their Amazon Prime subscription, users must scroll past a number of graphics and statements about “Exclusive Prime benefits” they will lose, a tactic that manipulates users through the fear of loss. Amazon uses this practice to discourage the user from ending their subscription by repeatedly offering a bevy of identically designed buttons designed to divert the user’s attention away from cancelling or delay their decision.

- If a user manages to cancel their Amazon Prime subscription, they receive a message titled “Oh no! Your Prime benefits are ending!” While titled as a “confirmation” email, the contents are written in the style of a warning, informing the user that they would soon lose benefits by ending their Amazon Prime membership while offering bright yellow button that would allow them to retain these benefits. Clicking this button instantly takes the user back to their Amazon account, with a message stating that their Prime membership has been reactivated. “This is the roach motel in action: unsubscribing from Amazon Prime takes navigating at least five pages, but undoing that choice only takes a single click,” according to the groups.

“It’s okay for a company to ask consumers to confirm that they want to cancel its service, but it’s not acceptable to deliberately throw multiple roadblocks in the way, as this study shows Amazon doing. It’s especially concerning when consumers are trying to cancel free trial offers, because they’ll end up being charged for a service they don’t want if they don’t get out in time,” said Susan Grant, CFA Director of Consumer Protection and Privacy.

Trump Administration Issues Final Assault on Consumers’ Energy Bills

In the final days of the Trump administration, the U.S. Department of Energy (DOE) made a last-minute approval of an anti-consumer rule that, unless it is remedied by the Biden Administration, would effectively keep inefficient gas furnaces, water heaters, and boilers on the market.

DOE has not made a meaningful update to the standards since 1987. Instead, they have moved at a painfully glacial pace in considering new ones to the point where the Trump Administration has been able to throw a major monkey wrench in moving the market toward more efficient heating products. They did so, despite the fact that heating products represent the largest utility expenditure (often 50%, or more) of consumers’ home energy bills. The new rule makes it impossible to remove inefficient gas (non-condensing) appliances from the market; instead, it requires that they be regulated separately from other more efficient (condensing) gas products performing the same functions of providing heat and hot water.

“This is yet another harmful rule costing consumers billions of dollars that the Trump Administration is forcing down our throats at the eleventh hour,” said Mel Hall-Crawford, CFA Energy Programs Director. Indeed, “according to a report released by the American Council for an Energy-Efficient Economy and Appliance Standard Awareness Project, potential annual savings from long overdue improved efficiency standards for furnaces, boilers, and water heaters will save residential consumers approximately $3 billion by 2035 and $7 billion by 2050.”

“The life span for residential furnaces and boilers is approximately 15-20 years, and for gas water heaters, it’s typically about 10 years—that is a very long period of time for consumers to pay unnecessarily a higher premium on their energy bills for a major appliance that is inefficient. We look to the incoming Biden Administration to take prompt action to negate this rule and update the efficiency standards for these products so that more efficient furnaces become the norm and consumers’ energy bills will be lower as a matter course,” Hall-Crawford concluded.

New Report Examines Black Americans’ Finances in the COVID Era

A majority of Black Americans worry about their financial future and do not have a savings account, a problem that is only made worse by the economic hardship unleashed by the COVID pandemic, according to a new report released earlier this month by America Saves, a program of Consumer Federation of America (CFA).

The report, titled Black American Finances and Savings in a COVID Era, utilizes new data from the Federal Reserve Board’s latest Survey of Consumer Finances (SCF) and from a recent survey of 1,003 representative Black Americans commissioned by America Saves. It finds that, while Black households showed signs of financial recovery in the decade since the Great Recession, they still hold much less net wealth than other households.

Moreover, that recovery has been threatened by the COVID recession sweeping the nation, according to the report. Nearly two-fifths (37%) of Black households said, when surveyed in late November 2020, that their current financial condition had worsened since the beginning of the year. That percentage rose to 41 percent among those with incomes below $50,000. A significant majority (59%) expressed concern about their financial future.

One reason for this worry may be lack of adequate savings. Well under half of Black Americans (42%) have a savings account and/or money market deposit account (MMDA) at a bank or credit union, according to the report, and many with an account said they were not saving enough to meet emergency expenditures. Nearly two-thirds (62%) of those surveyed said they do not make “regular and automatic” deposits in savings or MMDA accounts.

Importantly, a large majority of those without savings accounts said they would “seriously” or “probably” consider opening an account if their bank or credit union encouraged them to do so and charged no monthly fees. Based on those findings, America Saves Director George Barany called on banks and credit unions “to reach out to all low- and moderate-income households to offer them no-fee savings accounts and assistance in establishing automatic saving.”

President Biden has signaled the importance of advancing racial equity to the new administration’s policy agenda. Among the executive orders signed on Inauguration Day was one pledging to take “a comprehensive approach to advancing equity for all, including people of color and others who have been historically underserved, marginalized, and adversely affected by persistent poverty and inequality” and identifying it as “the responsibility of the whole of our Government.”

SEC Proposal Would Improve Mutual Fund Disclosures

A sweeping set of proposals issued by the Securities and Exchange Commission (SEC) last year would improve the information mutual fund investors receive, including by providing them with concise, investor-friendly shareholder reports and clearer cost and risk disclosures. “While there are many rules issued at the end of the Trump Administration that will need to be reversed or extensively revised, this is one proposal that deserves to continue moving forward in the Biden Administration,” said CFA Director of Investor Protection Barbara Roper.

In a comment letter submitted to the agency earlier this year, CFA praised the SEC “for producing such a thoughtful, investor-focused proposal to modernize the disclosure framework for investment funds. While there are areas where we support revisions to the proposed approach, this proposal offers a number of significant improvements over the current approach to fund disclosure and advertising. We strongly support its eventual adoption, once the approach has undergone investor testing and additional refinements based on the results of that testing to maximize the effectiveness of the proposed changes.”

Fund shareholder reports are often hundreds of pages in length, making them unreadable for the typical investor. Under the proposal, these lengthy disclosures would be moved online, and funds would be required to deliver a concise, tailored report to investors that covers the key information that investors have identified as being of greatest interest, including information on costs, past performance, and material changes. In addition, the proposal includes steps to simplify and clarify cost information, to provide more of that information in dollar amounts rather than as percentages, and to focus risk disclosures on a fund’s principle risks.

A sample report developed by the Commission to illustrate the proposal proves “it is possible to compile the required information in a concise and visually appealing format,” CFA wrote. In order to maximize those benefits, however, CFA called for the SEC to engage in investor testing to ensure that investors understand the terminology and can use the reports as intended to better understand their fund investments. CFA also called for the information required to be disclosed online to be “tagged,” so that it can be aggregated and analyzed by third parties to the benefit of investors.

The proposal would leave the choice of how to receive those disclosures – whether in paper form through the mail or electronically – to the investor. CFA strongly supported this aspect of the proposal. In a separate letter filed late last year, CFA urged the SEC to reject a proposal being circulated by industry to default investors to electronic delivery of disclosures based simply on their having, at some point, provided the firm with an email address or smartphone number. While the time is right for the SEC to consider the potential for technology to change its approach to disclosure, “simply changing the default for how disclosures are delivered from paper to digital is unlikely to deliver the potential benefits to investors of a technology-enabled approach to disclosure,” CFA argued.

“If the Commission were to adopt the approach outlined by these groups, it would waste this opportunity to deliver that more extensive and potentially more creative reimagining of our disclosures for the digital age,” CFA wrote. “Instead of rushing to change the default, the Commission should conduct a more thorough analysis of the issue in order to ensure that the evolution toward greater reliance on e-delivery occurs on terms that are most favorable to investors and not just those that are most convenient for industry. That is a standard the current proposal from industry groups does not meet.”

“We expect disclosure modernization to be a priority in the Biden Administration,” Roper said. “But while the SEC resisted investor testing in the past administration, we expect such testing to be central to the agency’s approach going forward in order to ensure that proposed changes actually deliver the promised benefits,” she added.

Safe Washington Drivers with Low Credit Scores Charged Over 75% More

As the Washington State Legislature considers legislation to ban the use of credit scores in auto insurance rate setting, CFA released new data earlier this month demonstrating the harmful impact on consumers of this rate-setting practice. Specifically, the CFA analysis shows that good drivers in Washington State pay 35% more on average for auto insurance if they have Fair credit histories rather than Excellent credit, and those with Poor credit pay 79% more on average.

CFA’s analysis uses data from Quadrant Information Services, LLC to highlight the premium hikes imposed by 10 of Washington State’s largest insurers. The analysis, which tests premiums for good drivers purchasing the minimum state-mandated coverage, found that:

- Statewide, safe drivers with Poor credit pay 79%, or $370, more on average than a driver with Excellent credit, all else being equal.

- Premiums increase by 35%, or $165, on average statewide for a good driver with Fair credit rather than Excellent credit.

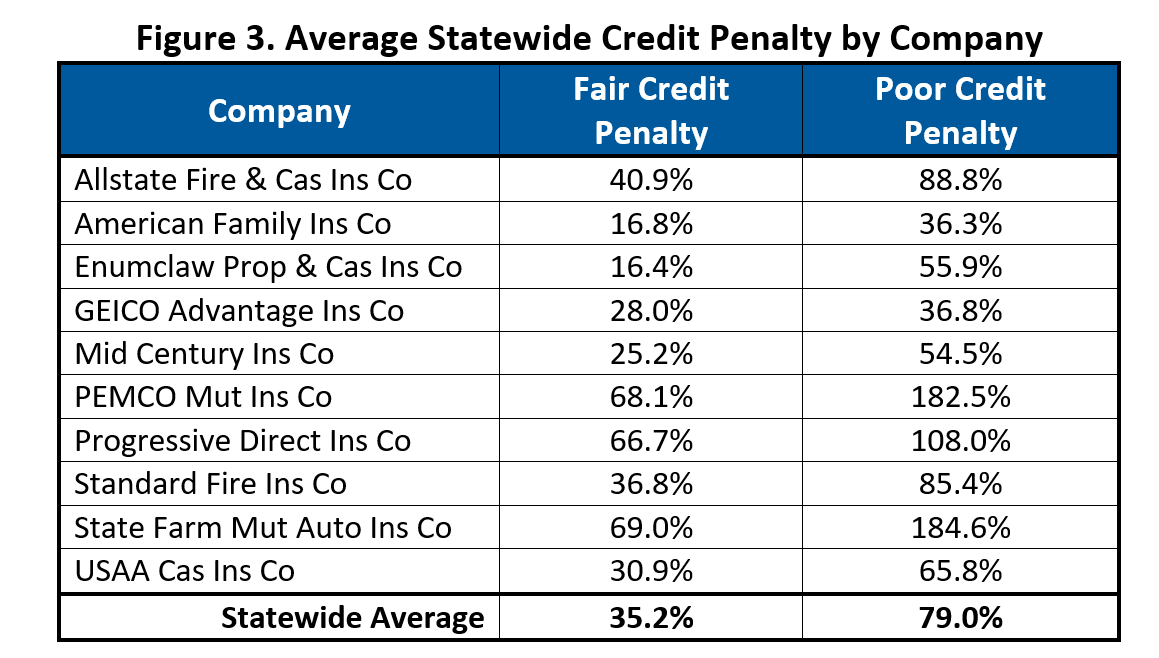

- State Farm charges the highest credit score penalty of 69% for drivers with Fair credit and 185% for drivers with perfect driving records but Poor credit. PEMCO charges the next highest credit history penalty – 68% for Fair credit drivers and 183% for Poor credit.

- Even the smallest credit score penalty, imposed by American Family, forces safe drivers with Fair credit to pay 17% higher premiums and those with Poor credit to pay 36% more.

- In Seattle, the average annual premium rises by $508 for a safe driver with Poor credit, and by more than $700 for customers of either Allstate or State Farm.

The data makes it clear that drivers with anything less than excellent credit face severe penalties in Washington State, and they have to pay substantially more for mandatory auto insurance than if they had better credit scores, even when they have perfect driving records.

The Washington premium data reviewed by CFA includes premium quotes for minimum limits auto insurance coverage from the state’s 10 largest insurers in every ZIP code. For each company, CFA reviewed the premium charged to 35-year-old drivers with different credit scores. Every premium in the database CFA used for the analysis is for a driver who has no accidents and no tickets in their driving history, and who drives a 2011 Honda Civic 12,000 miles per year.

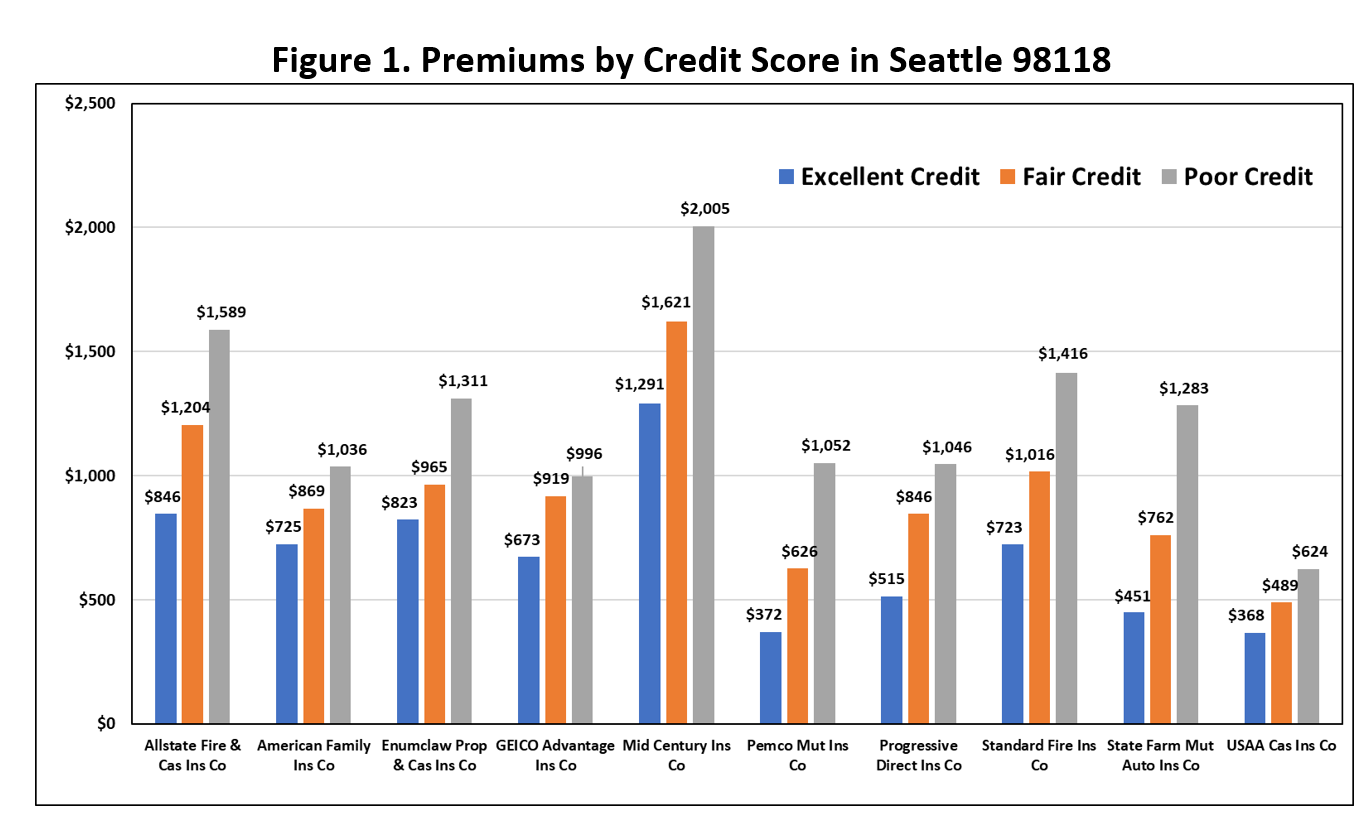

Figure 1 shows the premiums quoted to a female driver living in the Rainier Valley neighborhood of Seattle (98118) by all 10 companies according to her credit score. While the cheapest basic limits policy for the driver with an Excellent credit history (excluding USAA, which requires policyholders to have a military affiliation) is $372 from PEMCO, the best rate a driver with poor credit can find in 98118 is the $996 premium offered by Geico. That’s $624 more for drivers with perfect records even after shopping nine different companies.

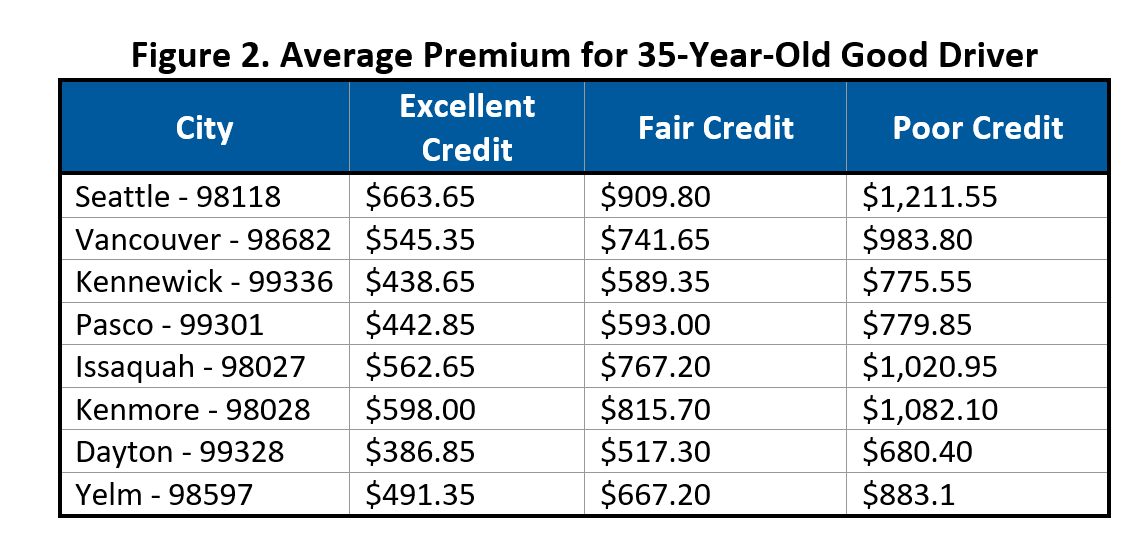

Figure 2 shows the credit based premium differences in several communities around the state, illustrating that the credit penalty is imposed on safe drivers no matter where they live.

Figure 3 shows the different penalties applied by each of the 10 companies reviewed by CFA. State Farm and PEMCO impose the most significant surcharge on lower credit drivers, while American Family and GEICO Advantage charge the lowest (but still large) penalties.

“Since state law requires that every driver buy insurance, the insurance companies should have to price policies fairly and give every good driver the best price, regardless of their credit history,” said Doug Heller, CFA Insurance Expert. “By punishing drivers with clean driving records but less than perfect credit, the insurance companies make coverage more expensive for those least able to afford it,” Heller continued.

“No matter where you live and how much you shop around, if your credit score is not great, you will be penalized when you buy insurance,” stated CFA Insurance Advocate Michael DeLong. “But the legislature has the chance to change this. They can and should pass SB 5010, which would ban the use of credit scores.”

SB 5010 was recently heard by the Washington Senate Business, Financial Services, and Trade Committee, and is waiting to be reported out.

17th Annual High Cost Lending Summit

Earlier this month, CFA hosted the 17th Annual High Cost Lending Summit as a two-day, virtual conference. The event involved a series of panel discussions highlighting current, and upcoming challenges in fighting the issue of high cost, predatory lending. They included: Lessons from the Ground, a panel focusing on the work of activists fighting high cost predatory lending across the states; Recent Research in the Payday Lending Sphere, a discussion on some of the new data and research coming out of fellow advocacy groups; What’s Next for Federal Regulation and Legislation, a roadmap of how these issues could play out in the Biden Administration; and The Threat of Fintech and Rent-A-Bank, focusing on how high cost lenders skirt state-imposed rate caps. The Summit also featured a keynote speech from Sen. Chris Van Hollen (D-MD).

Thanks to everyone who joined us for this great event!