State and national consumer organizations joined the Consumer Federation of America (CFA) today to release a new study concluding that the property/casualty insurance industry continued in 2007 to systematically overcharge consumers and reduce the value of home and automobile insurance policies, leading to profits, reserves, and surplus that are at or near record levels. The study estimates that insurer overcharges over the last four years amount to an average of $870 per household.

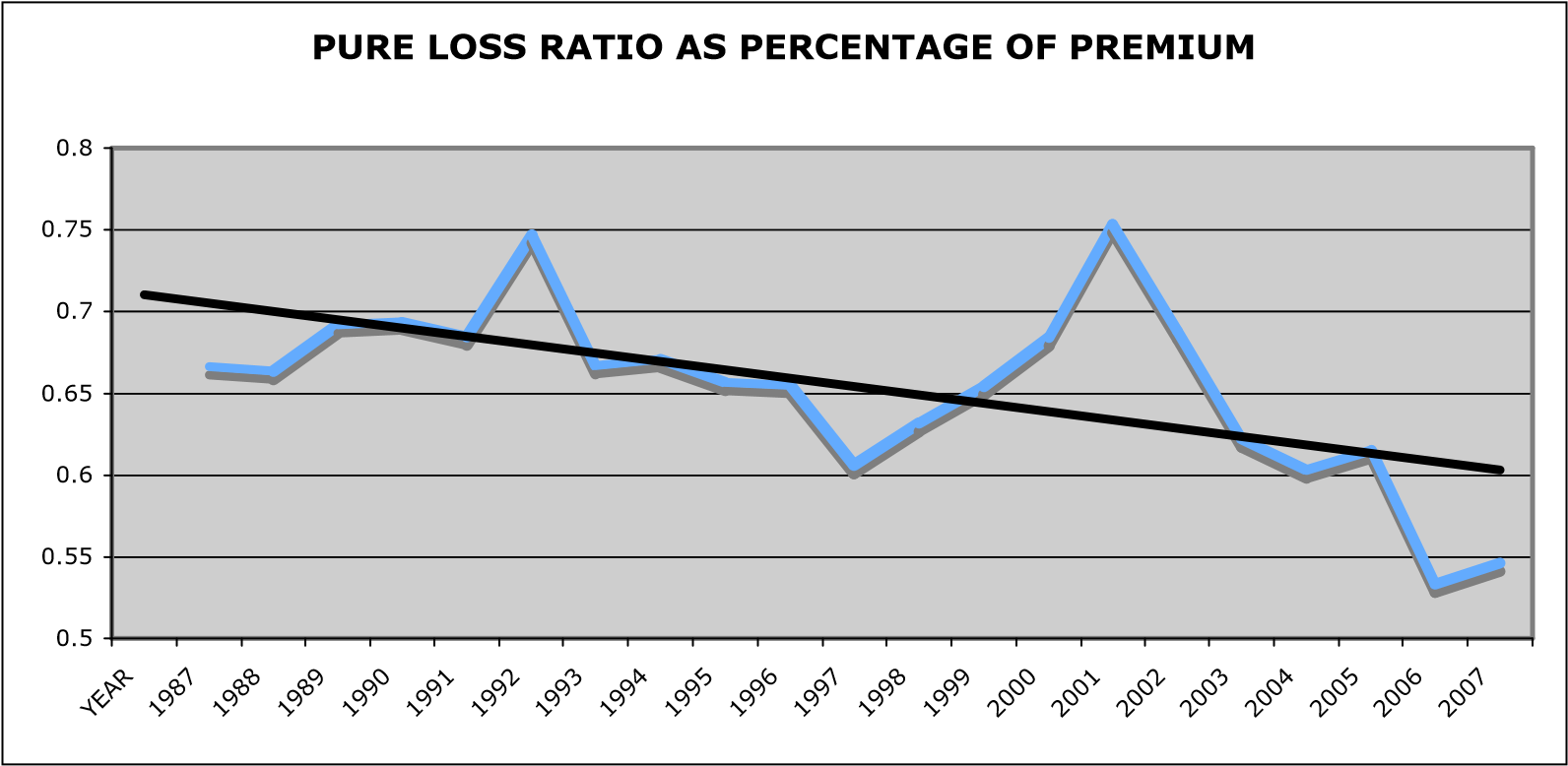

The report provides extensive data demonstrating that property/casualty insurance companies are paying out lower claims in relationship to the premiums they charge consumers than at any time in decades. The pure loss ratio, the actual amount of each premium dollar insurers pay back to policyholders in benefits, was only 54.6 cents in 2007. Over the past 20 years, the amount paid back as benefits has dramatically declined from over 70 cents per premium dollar, indicating a huge loss in the value of insurance to consumers.

“Consumers ultimately pay the price for the unjustified profits, padded reserves, and excessive capitalization that exist right now in the insurance industry,” said J. Robert Hunter, the Director of Insurance for the Consumer Federation of America (CFA) and author of the study. Hunter is an actuary, former state insurance commissioner, and former federal insurance administrator.

“The insurance industry reaped record profits in 2004 and 2005, despite significant hurricane activity,” said Hunter. “Profits in 2006 rose to unprecedented heights and 2007 may set a fourth consecutive profit record,” he said. “Unfortunately, a major reason why insurers have reported record-high profits and low losses in recent years is that they have been methodically overcharging consumers, cutting back on coverage, underpaying claims, and getting taxpayers to pick up some of the tab for risks the insurers should cover,” said Hunter.

In the last several years, insurers sharply increased premiums for homeowners and commercial insurance and reduced or eliminated coverage for tens of thousands of Americans in coastal areas. Insurers have succeeded in convincing Congress to continue taxpayer subsidies for terrorism losses and are seeking additional subsidies for catastrophe insurance.

Using a number of common measures of financial health, the study finds that balance sheets for property/casualty insurers are in better condition overall than at any time in history.

Record High Profits/ Low Losses

The study estimates that after-tax returns for 2007 are about $65 billion, just under the record level set in 2006. If insurers release even a small part of their swollen reserves as profits, final profits for 2007 will exceed those of 2006. Profits for the record years of 2004, 2005, 2006, and 2007 are estimated to be $253.1 billion. The loss and loss adjustment expense (LAE) ratio for 2007 is estimated to be 66.7 percent, the second lowest in the 28 years studied. Five of the seven lowest loss and LAE ratios in the last 28 years have occurred since 2003.

Claim Payouts Continue to Drop

Consumers have experienced a startling drop in the amount of premium paid in benefits by the insurers, from 72 percent in the late 1980s to only 60 percent today when plotted on a straightline trend over the period:

This drop in the efficiency of the insurance product for consumers is startling and calls for action by the regulators to control industry excesses.

Insurance is a Low-Risk Investment

Representatives of the insurance industry often claim that high premiums and profits are necessary to compensate for the excessive risks they must bear. In fact, insurance is a low-risk investment. Using standard measures of stock market performance that assess financial safety and stock price stability, the property/casualty insurance industry represents a below-average risk compared to all stocks in the market, safer than investing in a diversified mutual fund.

In 2007, the study estimates that stock insurers will earn a return on equity (ROE) of more than 19 percent, well in excess of what is required by investors. The lower industry-wide ROE that insurers report underestimates the industry’s actual ROE.

Surplus is Unprecedented: Insurers are Overcapitalized

The study estimates that retained earnings, or surplus, for the entire industry was $687 billion at the end of 2007. An adequate surplus guarantees a safe insurance industry, but this amount is excessive by any legitimate measure. To assess the financial solidity of an insurance company, regulators examine the ratio of net premium written to surplus, which, at the lowest level ever, 0.66 to 1 (66 cents of premium written for every dollar of surplus), is less than half of the extremely safe 1.5 to 1 ratio that is recommended by many observers and far less than the famous “Kenny” rule of 2 to 1 as an efficient surplus level. The largest loss ever suffered by the insurance industry, Hurricane Katrina, represented an after-tax loss of $26.7 billion, or 4 percent of current surplus when adjusted to 2007 dollars. The $12.2 billion in after-tax losses experienced by insurers after the September 11th terrorist attacks amounts to 2 percent of surplus. Many insurers are engaged in massive stock buy-back programs and the purchase of other corporations with this excess capital. Insurance chief executive officers now have the highest average cash compensation of any industry in America. Even the Insurance Information Institute (III) admits that the industry is overcapitalized: “…there is excess capital in the industry today – estimated by some analysts to be as much as $100 billion…” The excess capital approaches $175 to $200 billion if reserve redundancies (see below) are eliminated.

Loss and Loss Adjustment Expense Reserves are Padded with Hidden Profits

When industry profits are high, as they have been in record amounts since 2003, insurers tend to pad their reserves. This practice contributes to financial solidity. However, insurers also pad their reserves because it removes income from their profit statements, thus lowering their tax burden because reserves are not taxed and income is. This practice also allows insurers to point to inflated “losses,” which rise due to reserve redundancies, as justification for not lowering rates.

The Insurance Services Office (ISO) estimates that loss and loss adjustment expense reserves at year-end 2006 were 9 percent redundant, a figure that represents over $50 billion in excessive reserves. Adjusting for the time value of money, ISO saw an additional $13 billion in padded reserves at year-end 2006. CFA estimates that the redundancy in reserves increased in 2007 and could be up to more than $80 billion by year-end 2007.

Insurers Have Lowered Risk and Maximized Profits through Legitimate and Illegitimate Means

In recent years, insurers have reduced their financial risk by making wise use of reinsurance and other risk-spreading techniques, such as securitization. However, the study cites several tactics that insurers have also used to shift costs and risk onto consumers and taxpayers. Some of the questionable methods that insurers have used to shift risk include:

- Sharp limits on coverage and availability. Insurers have imposed large hurricane deductibles, capped home replacement and rebuilding costs, added new exclusions such as mold, and placed unjustifiable restrictions on claims. For example, “anti-concurrentcausation” clauses, now in wide use, attempt to strip all coverage for hurricane damage if a non-covered event like a flood occurs, even if the flood hits hours after a home is destroyed by wind. Some insurers have canceled policies, refused to renew policies, or refused to write new coverage in coastal areas and entire states from Texas to Maine.

- Harsh homeowner’s rate increases. Insurers have imposed sharp rate increases on many homeowners throughout the nation. A major reason for these recent increases is that insurers are relying on short-term predictions of potential weather disasters, reneging on promises to use more scientific long-term computer predictions.

- Programs designed to systematically underpay claims. Many insurers are now using new computer-directed programs like “Colossus” and “Claims Outcome Advisor” that allow insurers to determine the amount of overall claims savings they want to achieve before claims are assessed for legitimacy.

- Taxpayer subsidies. Insurers and real estate interests were the major proponents of the Terrorism Risk Insurance Act, which Congress recently continued under industry pressure. The study estimates that insurance companies have received a subsidy of about $4 billion to date because insurance companies do not have to pay premiums for the reinsurance provided by the federal government. Some insurers have urged Congress to create a similar program to cover natural disasters. Insurers have also received significant taxpayer support at the state level, through the creation of state directed “insurers-of-last-resort.” The existence of these companies allows insurers to “cherry pick,” by insuring lower risk households themselves and sending higher risk households to the state company. Only Florida has taken steps to end this practice.

“Insurers have been so successful in shifting their risk onto consumers and taxpayers that they have produced record profits during a period of increased storm destruction,” said Hunter. “This risk shift is reflected by the fact that insurers are paying less and less of the premium dollars they receive in benefits to consumers.”

Recommendations for State Policymakers

- Require insurers to offer an all-risk homeowners insurance policy. This would once again ensure that homes are protected from catastrophic events. It would also help consumers understand exactly what their policy covers, and encourage insurers to do more to prevent losses before they occur.

- Better oversee the use of socio-economic factors used to set rates, like credit scoring. Insurers have been able to maintain excessive pricing through the use of such information as consumers’ credit scores, prior insurance limits, occupation, and educational attainment. This information is opaque to consumers and has not been examined by most regulators to ensure that it results in the setting of fair rates. State regulators should require that pricing practices: promote risk reduction; are logically related to risk (so consumers know what steps to take to reduce rates); protect low income and minority consumers; and are open and transparent to the public.

- Increase scrutiny of computer-based claims settlement procedures. The use of computer procedures has shielded insurers from scrutiny of questionable claims practices, while state insurance regulators have largely looked the other way. In 2008, regulators should pierce the mystery of how claims are settled and stop practices that deny the full payment of legitimate claims.

- Make state-backed reinsurance available. States should join together to offer reinsurance to private insurers using the recent Florida legislation as a model. If all catastrophe-prone states joined together to underwrite reinsurance at actuarially sound rates (or even at a mark-up of 50 percent over actuarially sound rates), they would likely end or significantly diminish the periodic crises that follow big hurricanes or earthquakes.

- Consider offering state-backed property and automobile insurance. Policymakers in coastal regions should consider whether the increasing rates, decreasing coverage, and turmoil created by large numbers of periodic non-renewals have reached the point where private insurers should not be offering certain coverage at all. In 2007, Florida allowed its primary insurer, Citizens Insurance Company, to offer comprehensive homeowners insurance policies at competitive rates. This forced private insurers to lower some rates and allowed Citizen’s to spread risk more broadly. States should consider taking this approach further by offering automobile insurance, which would assure that, over time, the state would make a small profit or at least break even on its insurance offerings.

- Better regulate the use of catastrophe modeling. States should follow Florida’s example in blocking catastrophe-modeling firms from using short-term projections as the basis for establishing insurance rates and require them to return to the practice of using long-term projections. Coastal states should consider uniting to develop a coastal weather modeling system of their own to test the accuracy of private projections and to evaluate the fairness of insurer rate requests.

- End unjustified geographic discrimination. If any insurer fails to market a line of insurance that it is selling in other parts of a state (or in other states), regulators should consider convening hearings to determine if the insurer’s license should be revoked for geographic discrimination.

- Review homeowners insurance policy forms for hidden provisions. Insurance regulators should carefully review the policy forms and exclusions they have allowed to become part of homeowner’s policies, and require insurers to offer clear disclosure about exclusions and lower rates to reflect decreased risk that results from these exclusions.

Recommendations for Federal Policymakers

- Repeal the McCarran-Ferguson Act’s antitrust exemption for insurance. The excessive pricing and unjustified claims practices documented in this report are abetted by collusive and anticompetitive behavior allowed under this law. Congress should impose the same antitrust law relative to insurance with which virtually every other business in America must comply.

- Authorize interstate cooperation on catastrophe insurance. Congress should authorize states to use interstate compacts to create multi-state risk “pools” to cover wind and other catastrophic losses. Such legislation should allow states to permit the accumulation of tax-free reserves if the funds collected are kept for the purpose of paying claims after wind disasters strike.

- Repair the troubled National Flood Insurance Program (NFIP) before vesting it with any additional authority. Congress should not pass any legislation to subsidize wind insurance or to add wind coverage to the National Flood Insurance Program. The NFIP is in disarray. Out-of-date flood maps used by the NFIP have underestimated flood risk and resulted in unjustifiably low insurance rates. This has created hidden subsidies for unwise construction in the nation’s floodprone areas, helping to create a $20 billion shortfall in NFIP funding. The use of private insurers to run the program has resulted in between one-third and two-thirds of flood premiums flowing to insurers, not to the payments of claims. There is also evidence that insurers have shifted the cost of wind claims they should have paid to taxpayers—who support the NFIP.

- Eliminate any federal policies that might undermine the development of the securitization of insurance risk. The federal government should undertake a study of federal laws and rules to ensure that the responsible securitization of insurance risk is encouraged, not discouraged, by federal tax policy. Fostering increased securitization of catastrophe risk is a far more favorable option for consumers and taxpayers than insurer efforts to receive more taxpayer subsidies.

Advice for Consumers

- If possible, do not do business with a company that has a history of anti-consumer behavior. When purchasing or renewing a homeowner’s policy, consumers can contact their state insurance departments to get information on companies in their areas that have sharply raised rates and cut back in coverage in recent years.

- Carefully review policies at purchase or renewal to determine whether high out-of-pocket costs will be imposed. Consumers should look for separate deductibles for wind damage, anticoncurrent-causation clauses, mold exclusions, limits on replacement costs, and other restrictions on coverage.

- Consumers who live away from coastal areas should actively shop for better coverage and rates. Because insurance companies are overcapitalized, they are looking for new business in lower risk areas. Rate decreases and better coverage are possible.

- Demand thorough oversight of insurer actions by state regulators. If consumers have a problem with rates or coverage, they should file an immediate complaint in writing with their state insurance agency and follow up for a response. Consumers should also contact insurance regulators to find out what they are doing to require that rates are fair and reasonable and that insurers are not unjustifiably withdrawing coverage.

The report was written by the Consumer Federation of America and released with national and state consumer organizations, including Americans for Insurance Reform, Center for Economic Justice, Center for Insurance Research, Center for Justice and Democracy, Consumers Union, Empire Justice, Florida Consumer Action Network, Foundation for Taxpayer and Consumer Rights, Neighborhood Economic Development Advocacy Project, New Jersey Citizen Action, Texas Watch, and United Policyholders.