Washington, D.C. — This morning, the Consumer Federation of America (CFA) released data which show that increasingly cautious borrowing by consumers has forced credit card issuers to reduce their marketing efforts and extension of credit. These data include numbers compiled by economist Lawrence M. Ausubel, which reveal a significant decline in the per capita personal bankruptcy rate – 9.43% from the fourth quarter of 1998 to the fourth quarter of 1999. There were 112,000 fewer personal bankruptcies in 1999 than in 1998, the largest one-year decline on record.

“Credit card issuers should abandon their hypocritical efforts to pass one-sided bankruptcy legislation,” said Travis Plunkett, CFA’s legislative director. “Restricting consumer access to bankruptcy will only encourage credit card issuers to market and lend more aggressively, especially to the least affluent and sophisticated borrowers,” he added.

“The bankruptcy bill would lead to a resurgence in the incidence of badly-overextended consumers by encouraging lenders to lower their credit standards and solicit riskier customers,” said Professor Ausubel. “Since the bankruptcy crisis is selfcorrecting, it does not require harsh legislation,” he added.

Borrowers Exercise Greater Restraint

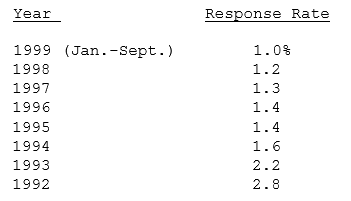

Credit card borrowers, whose restraint was evident by the middle of 1999, have cut back even more since then. They have increasingly “just said no” to credit card solicitations. As the data below show, they have dramatically reduced their “response rate” to these mailings — from 2.8 percent (1992) to 1.0 percent first 9 months of 1999) — a decline of 64.3 percent. [Source: BAI Global]

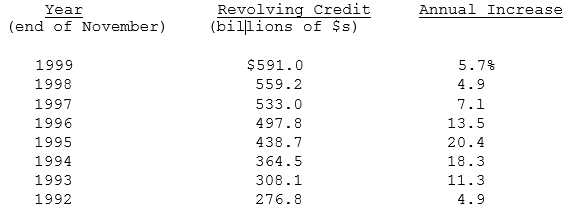

Borrowers have also significantly cut back annual increases in credit card borrowing. In the past decade, these increases escalated steadily from about a 5 percent level to more than 20 percent then declined back to the 5 percent level. [Source: Federal Reserve Board] (Since the last data released by the Fed are for the end of November, we have compared revolving debt levels at the end of November in every year. Almost all unsecured debt is credit card debt.)

Borrowers Default Less Frequently on Debts

Over the past two years, credit card lenders have seen net chargeoffs (debt losses/outstanding debt) decline steadily. They have suffered lower debt losses as a percentage of total debts and in absolute dollars. [Source: VERIBANC]

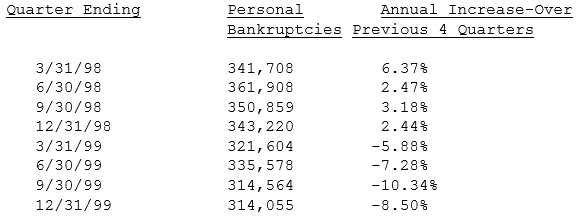

A key reason for this recent reduction in debt losses is the decline, from the spring of 1998 until the winter of 1999, in personal bankruptcies. As recent research by Professor Ausubel of the University of Maryland indicates, from 1998 to 1999 the number of these bankruptcies declined 8.01 percent — from 1,397,695 to 1,285,801. Moreover, from the second quarter of 1998 until the last quarter of 1999, there has been an almost continuous decline. [Source: Administrative Office of U.S. Courts/Professor Lawrence Ausubel]

Credit Card Lenders Begin to Reduce Marketing and Credit Extension

In response to several factors including declining direct mail response rates and moderate increases in credit card debt, lenders have begun to reduce their marketing and credit extension.

Credit card mailings remain the single most important way for issuers to market their plastic. They “sell” about threequarters of all cards through this means. According to BAI

Global, credit card mailings increased from 3.1 billion in 1997 to 3.5 billion in 1998 but declined to 2.4 billion in the first 9 months of 1999, which projects to 3.1 billion for the entire year. According to another data source, which recently reported a decline in fourth quarter mailings, this number may be even lower, perhaps only 3.0 billion.

Even more striking is the decline, for the first time in decades, in the unused credit lines provided by bank card issuers. [Source: VERIBANC] From the end of 1992 ($499 billion) until the end of 1995 ($954 billion), these lines nearly doubled. Then from the end of 1995 until the end of 1998 ($2,071 billion), they more than doubled. But from the end of last year until the end of September 1999 ($2,046 billion), these unused credit lines actually declined.

Harsh Bankruptcy Bill (S. 625) Before the Senate

Credit card lenders have been the most prominent proponents of bankruptcy legislation, which has passed the House and will likely be considered by the Senate early in the Congressional session. Consumer organizations, academics and bankruptcy administrators oppose this legislation because it would make the bankruptcy system less effective, more cumbersome and more expensive for families that need financial relief.

The Senate bill would not provide consumers with information that they could use to avoid bankruptcy. Late in the 1999 Congressional session, the credit card industry killed a key amendment to the Senate bill that would have informed cardholders on their monthly statement of how long it would take them to pay off their outstanding balance at the minimum rate, as well as the total amount they would owe in interest and principle at this rate.

Under the present Senate bill, card issuers do not have to provide any information to cardholders on monthly statements if they maintain a toll-free number to give consumers general information about paying off their balances at the minimum rate. Card issuers would not be required to disclose the existence of the toll-free number.

“Creditors have killed an amendment that would help Americans use unsecured credit intelligently and responsibly,” said Plunkett. “The lender substitute would be virtually worthless to borrowers,” he added.

Onerous legal and paperwork burdens in the Senate bill will disadvantage cash-strapped families that cannot afford a lawyer. Cumbersome informational requirements will substantially increase the cost of accessing the system for families who are most in need of debt relief and financial rehabilitation. These paperwork requirements would apply to all debtors, even lowerincome debtors.

The means test to determine which debtors can file chapter 7 bankruptcy (instead of chapter 13) is arbitrary and inflexible and will make it harder for modest-income Americans to get financial relief. It is based on IRS standards not drafted for bankruptcy purposes that do not take into account individual family needs for expenses like transportation, food and rent. It disfavors renters and individuals who rely on public transportation and unduly benefits higher income individuals with more property and debts.

The Senate bill would compromise the payment of high-priority debts after bankruptcy, such as child support and alimony, by increasing the amount of debt for which debtors will remain liable. The bill provides creditors, especially credit card companies, with a variety of new opportunities to file lawsuits challenging the discharge of debts; lawsuits that financiallypressed families will likely accede to because they cannot afford to challenge them. Moreover, the bill allows creditors to coerce “reaffirmation” agreements from debtors to remain legally liable for more consumer debts, by threatening to repossess essential appliances like refrigerators and washers. These provisions cover all people who file for bankruptcy, including those who meet the “means test” and qualify for chapter 7.

The bill does not insure that, in this intensified competition for the debtor’s limited resources, parents and children owed support will prevail over the sophisticated collection departments of creditors.

“The Senate bankruptcy bill does not pass the basic test of fairness and balance. It does little or nothing to address creditor abuses while denying access to the fresh start needed by many families in financial crisis,” said Plunkett.

The Most Important Thing Congress and Issuers Could Do to Accelerate the Decline in Personal Bankruptcies

While personal bankruptcies should continue to decline as consumers and creditors exercise greater restraint, this decline would, over time, certainly accelerate if credit card issuers were to phase in an increase in the minimum payment allowed from 2-3 percent to 4 percent.

“The decline in the typical minimum payment to 2 or 3 percent is responsible for much of the rise in consumer bankruptcies through the past decade,” noted Stephen Brobeck, CFA executive director. “That low minimum payment, which barely covers interest obligations, convinces many borrowers that they are okay as long as they can meet all their minimum payment obligations. But those that cannot afford to make these payments carry so much debt that bankruptcy is usually the only viable option.”

In the past year, lenders have expressed surprise and dismay that they can no longer reliably predict which borrowers will end up in bankruptcy. That is because low minimum payments allow insolvent borrowers to pay all their credit card bills on time. But at a certain point they realize their situation is hopeless and declare bankruptcy. (At 2 percent, monthly credit card payments totaling $400 represent $20,000 of credit card debt.)

Although some creditors now realize they made a mistake in dropping the minimum payment to 2 percent, they will not benefit from unilaterally raising this minimum since they will lose so many customers. That is why Congress would be wise to require credit card issuers to require minimum payments of at least 4 percent from all new customers. Despite industry criticism of such a requirement, it would be welcomed by many individual lenders.