On November 7, 2024, the Consumer Financial Protection Bureau (CFPB) ordered Navy Federal Credit Union (NFCU) to refund more than $80 million to consumers, stop charging illegal overdraft fees, and pay a $15 million civil penalty to the CFPB’s victims’ relief fund. The enforcement action found that NFCU charged customers surprise overdraft fees, even when their accounts showed sufficient funds at the time of the transactions.

On June 30, 2025, Russell Vought, the CFPB’s Acting Director, terminated this enforcement action. The reversal contradicts a memo from the CFPB’s Chief Legal Officer to prioritize the agency’s enforcement work on the needs of “service members and their families.”

The CFPB’s order covered two scenarios that caused surprise overdraft fees. There is only a slight overlap between the two: one covers the period from 2017 to November 30, 2020, whereas the other spans from October 1, 2020 to December 31, 2022.

To better understand the order and the implications of its cancellation, the Consumer Federation of America reviewed complaints involving overdraft and non-sufficient funds (NSF) fees filed with the CFPB’s Consumer Complaint Database (CCD) by Navy Federal Credit Union account holders from January 1, 2017 until September 1, 2025. This span covers both relevant time periods during which surprise overdraft fees were charged.

However, because people often file complaints well after an incident’s occurrence, CFA’s analysis also takes into account complaints up to September 1st of this year. The majority of the complaints filed with the CFPB about NFCU’s overdraft practices have been received since the announcement of the enforcement action on November 7, 2024. After discussions with former CFPB officials, it is CFA’s understanding that this is not an unusual outcome. Enforcement actions convey to the public that a regulator is willing to hold companies accountable for unlawful practices. When an action is announced, victims come forward to share their stories, even if the violation occurred in the past. The counterfactual—that 2025 complaints only cover 2025 activities—seems highly implausible, given that the number of complaints in the last six months far exceeds those of the last twelve years. In fact, if it were true that complaints were always filed quickly, it would signal the risk of alarming new consumer compliance issues at NFCU.

The CFPB’s practice has always been to verify with the financial institution that the complaints received were made by a person with an account, so we can have confidence that each complaint is unique and genuine. In fact, many of the complaint narratives highlight the exact practices described and reference the order as grounds for a remedy.

For example, a servicemember living near Joint Base San Antonio Lackland filed this complaint in January 2025:

For these reasons, complaints from 2017 to 2025 provide a reasonable lens for considering the impact of the order’s cancellation. Naturally, it is not a perfect fit; some of the complaints surely resulted from other types of overdraft sequences, and the vast majority of people who were charged surprise overdraft fees never filed a complaint. The data is the best resource available for understanding the experiences of account holders. Because approximately 80 percent of complaints have a ZIP code, these complaints can also help clarify important questions about the geographic distribution of the harms. For example, the data can reveal how many complaints were filed by account holders living near large military installations.

About the Order: Some payments would be authorized when the payment was made, but later charged a surprise overdraft fee

The larger component of the order concerned instances when consumers were charged an authorized-positive settle-negative (APSN) overdraft fee. NFCU would authorize the transaction, which appeared to be payable given the available balance, but then charge an overdraft fee when the transaction settled negatively during overnight batch processing. The order acknowledged that the timing between payment and submission by a merchant for a transaction can vary significantly, and often takes as long as three days.

The CFPB said people could not have reasonably known how to avoid these fees. Account holders clearly agreed – and were frustrated by having to pay fees. An internal NFCU document obtained in the CFPB’s investigation quoted an employee who said APSN fees frustrated customers and were “a huge pain point for members.”

During the two-year period covered by the order – the only years when victims of the policy were due a remedy – account holders were charged approximately $80 million in unexpected APSN overdraft fees. Starting in January 2023, NFCU changed its method for settling these transactions.

Deposits from payment apps increased the available balance but were not credited to the current balance until much later, leading to surprise overdraft fees.

The second activity addressed by the order concerned instances when consumers were charged a surprise overdraft fee for an overage resulting from a delayed original credit transaction (DOCT). The CFPB said NFCU’s DOCT policy was in practice from as far back as at least 2017. The policy typically applied to deposits received from peer-to-peer payment app services such as Cash App, PayPal, or Zelle. The account holder would see an increase in their available balance within a few minutes of receiving funds. However, if the transaction came in after 10 am, the daily cutoff time until September 2020, the deposit would not be posted until the next day. During the interim, the account holder was left vulnerable to surprise overdrafts.

The CFPB said cutoff times for DOCTs were not clearly disclosed to customers. NFCU changed the daily cutoff time to 8 pm in September 2020 and made a disclosure about the change in December 2020. During the period covered by the order, surprise overdraft fees related to DOCTs exceeded $4 million.

*But disclosures notifying consumers of any cutoff time – at 10 am ET or 8 pm ET – were not provided until December 2020.

*But disclosures notifying consumers of any cutoff time – at 10 am ET or 8 pm ET – were not provided until December 2020.

In September 2020, NFCU took a voluntary step to remedy some DOCT surprise overdrafts. At that time, a new policy was put in place where all DOCTs received before 8 pm ET posted on the evening of the same business day. To address the costs incurred by affected consumers, NFCU issued refunds totaling $3.4 million for overdrafts that occurred as a result of this sequence during the period from 2017 to 2019.

The Consent Order

NFCU consented to the issuance of the order “without admitting or denying any of the findings of fact or conclusions of law.”

The CFPB used the authority granted to it in the Consumer Financial Protection Act (Section 1036(a)(1)(B) to prevent “unfair, deceptive or abusive acts and practices.”

The CFPB filed the order on November 7th, 2024 (the “Effective Date). The compliance plan required NFCU to deposit $80,689,100 into a separate deposit account within 10 days. Within 60 days, it was required to submit, for the review of the CFPB’s Director of Enforcement, a plan to implement the terms of the order within 60 days. Given that the plan was due only two weeks before the start of a new administration, it is doubtful that NFCU paid remedies.

Analysis

In the time period analyzed (January 1st 2017 – September 1st 2025), there were 8,272 complaints submitted to the CFPB regarding overdraft issues at Navy Federal Credit Union. Of these, 2,331 were submitted by servicemembers (who checked the servicemember box when filling out their complaint).

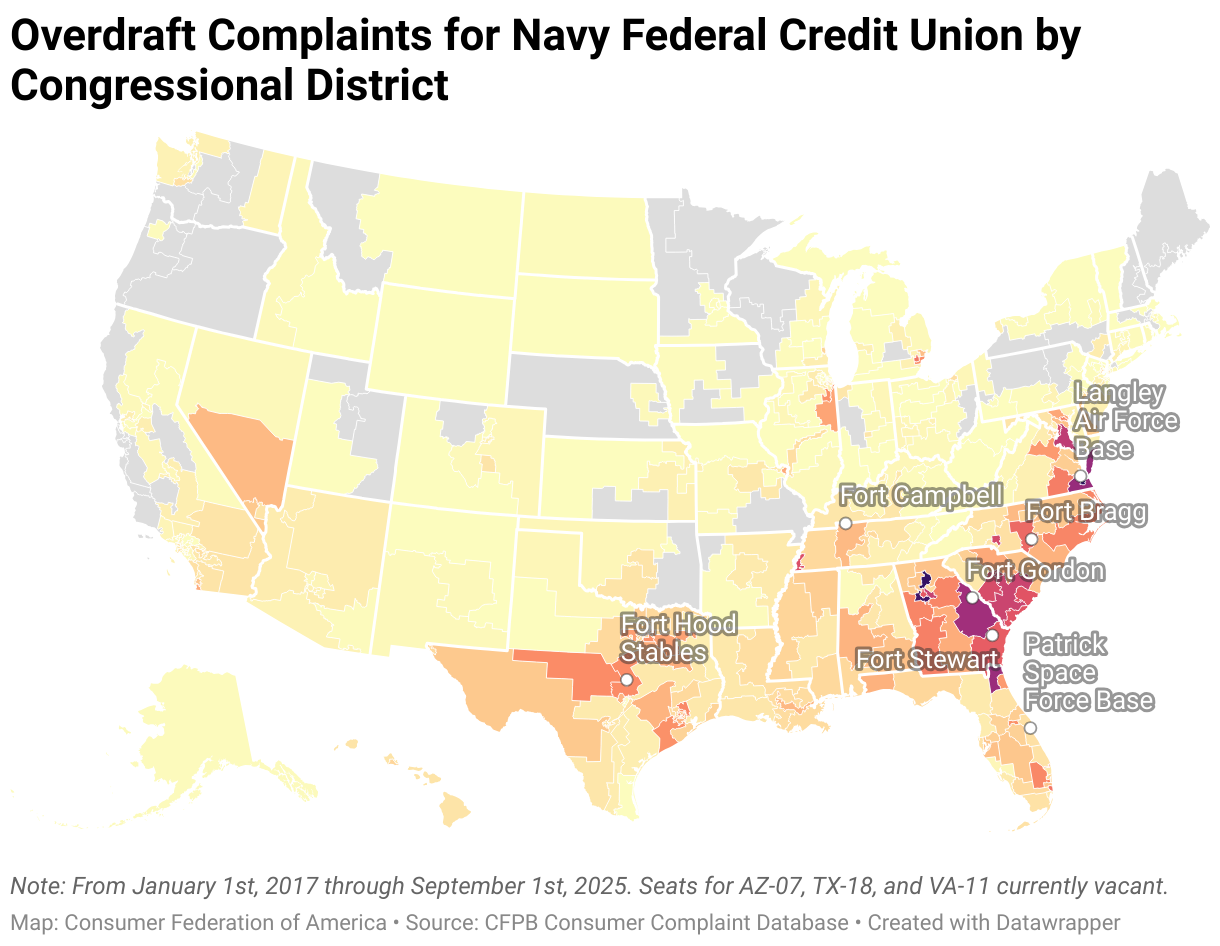

The map below breaks down the number of overdraft complaints for Navy Federal by congressional district. The map reveals that most of the complaints were filed by consumers in the southeastern part of the country, home to many military bases and families. The district with the highest number of overdraft complaints was the Virginia 3rd, which includes the city of Norfolk.

Hover over the map for further information on the number of NFCU overdraft complaints, the number of complaints by service members, and the representative for each district. Click on the “Get the data” button to download the data in the map. A table breaking down complaints by state can be found at the bottom of this page.

Figure 1: NFCU Overdraft Complaints by Congressional District

Source: CFPB Consumer Complaint Database; Consumer Federation of America

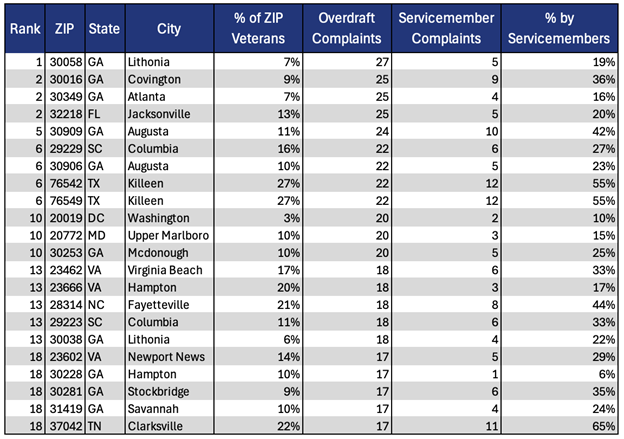

For a more fine-grained look at the data, we also rank ZIP codes by the number of NFCU overdraft complaints in the table below. ZIP code 30058 in Lithonia, Georgia has the most complaints with 27. Like in the above map, many of the most impacted ZIPs are in the southeastern part of the country; four of the top five ZIPs are in Georgia alone.

We also provide the share of the population in each ZIP that is a veteran using data from the American Community Survey (data on the number of active-duty military personnel by ZIP is not publicly available). The average share of veterans in a ZIP code across the United States is 8%. The vast majority of the most impacted ZIPs have veteran shares greater than this (18/22 ZIPs).

Table 1: ZIP Codes by Number of NFCU Overdraft Complaints

Source: CFPB Consumer Complaint Database; American Community Survey; Consumer Federation of America

Why This Matters

Debts incurred by active-duty servicemembers and their families are serious problems. In 2006, the Department of Defense released the groundbreaking “Report on Predatory Lending Practices Directed at Members of the Armed Forces and Their Dependents,” noting that predatory lending undermines military readiness, harms the morale of troops and their families, and adds to the cost of fielding an all-volunteer fighting force.” The report contributed to work that led to the passage of the Military Lending Act (MLA). In 2014, the Wall Street Journal wrote that “the Pentagon considers debts incurred by military members to be a significant morale and readiness issue.”

Overdraft fees can contribute to debt problems. In his 2011 Senate testimony, retired US Navy and Navy-Marine Corps Relief Society President Charles Abbot said that “Banks and credit unions on and near military bases continue to charge exorbitant and multiple fees associated with overdraft protection.” The Pew Charitable Trusts documented issues surrounding overdraft practices at banks serving the US military in a 2014 report. While some banks defend overdraft practices on the grounds that they are less harmful than payday loans, many states no longer permit payday lending. In places where payday loans are illegal, overdraft credit does not serve as a better alternative. In fact, it may be the most expensive option. Indeed, a substantial share of complaints filed regarding NFCU’s overdraft fees were made in states without payday loans, including Georgia, Virginia, and North Carolina.

About Navy Federal Credit Union (NFCU)

NFCU is a non-profit federally chartered credit union owned by its shareholder depositors. Its field of membership consists of servicemembers, veterans, Department of Defense employees and contractors, and their families.

When Congress passed the Federal Credit Union Act in 1934, it exempted credit unions from federal income tax. In exchange for these and other exemptions, credit unions return profits to their shareholders through lower fees on services, lower interest rates on loans, dividend payments, and other benefits.

Navy Federal Credit Union is a member of the Consumer Federation of America and has representation on CFA’s Board.

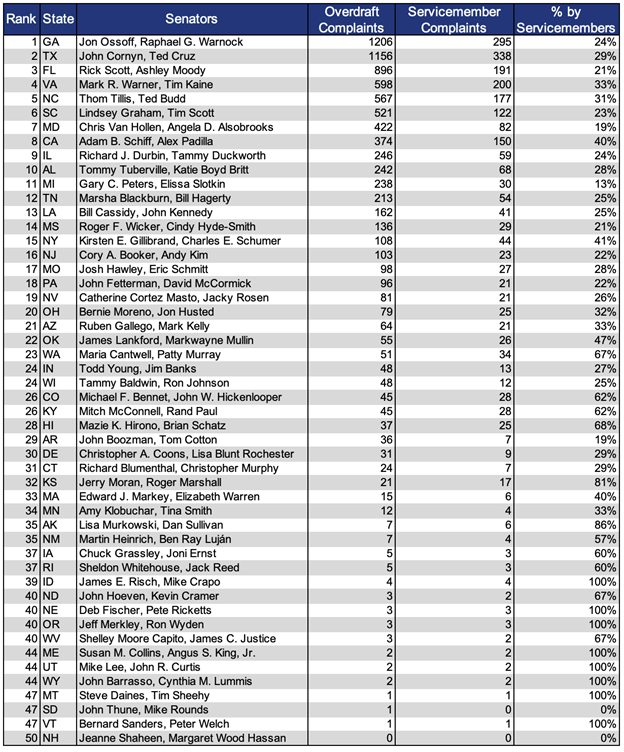

Table 2: States by Number of NFCU Overdraft Complaints

Source: CFPB Consumer Complaint Database; Consumer Federation of America