Rising auto insurance premiums are affecting drivers across America, and folks are looking for ways to save money. One strategy often touted by insurance companies is to sign up for usage based insurance (UBI), where the companies use “telematics” to track your driving behavior and calculate your premium based on that behavior. A recent Maryland report on the use of telematics finds that while these programs benefit some people, most Maryland drivers enrolled in telematics don’t see premium savings.

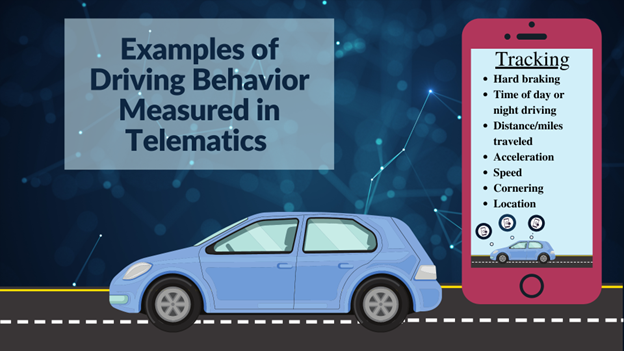

All of the largest insurance companies, from Allstate to USAA, offer these programs; they provide devices that can be installed in your car, use mobile apps downloaded to your phone, or capture data from technology in the cars themselves. Whatever telematics tech the company uses, once it is turned on, it monitors a range of driving behavior and sends that information back to the insurance company. And when your insurance policy is renewed, your premium can go up, down, or stay the same based on your driving habits. Some of the most common driving behaviors measured are listed below.

To elaborate, “hard braking” refers to how often someone slams on the brakes, and that results in higher premiums. Insurers also tend to charge people more if you drive at night or if you drive a lot. Your premium may also vary depending upon how quickly you accelerate, how often and by how much you exceed the speed limit, how often you make sharp turns around corners, and where you drive.

Telematics programs are not all the same. In addition to each having their own set of driving characteristics they use, some companies will push premiums up or down depending upon the driving score calculated from the data, while other companies only use the score to give discounts. Allstate, GEICO, Liberty Mutual, Progressive, and Travelers will hike your premiums if you are a poor driver. American Family, Farmers, Nationwide, State Farm, and USAA will not hike your premiums—at least that’s what they claim.

Theoretically, telematics could lower costs for good drivers, encourage safer driving behavior, and provide a much fairer assessment of risk than the current pricing models that penalize customers for their marital status, job title, credit score, and other socioeconomic factors. In practice, insurance companies collect an enormous amount of information through these programs but exaggerate the savings and continue to rate based on non-driving characteristics.

How do we know this? Because of the new report on telematics issued by the Maryland Insurance Administration (MIA), which is in charge of protecting consumers of insurance and making sure they are fairly treated. Over the past several months, the MIA issued a survey to 18 of the largest auto insurance companies in Maryland, 16 of which offered a telematics program. The relatively short report came out in early July, and it contains a wealth of useful information about telematics.

First, the number of telematics insurance policies in Maryland increased by 45% from 2021 to 2023. Despite that rise, most drivers still aren’t enrolled in these programs. Out of 2,296,713 drivers with auto insurance policies, 303,845 are enrolled in telematics—only about 13% of all Maryland drivers. Insurance companies have been aggressively promoting telematics through traditional advertising, celebrity endorsements, jingles, and digital “nudges” to encourage people to sign up (such as having telematics automatically be the default option when you are getting online insurance quotes). For all the hype, most people are wary of letting their insurance company ride shotgun in their car.

Second, most drivers did not save money on auto insurance by enrolling in telematics. In 2023, less than a third (31%) of drivers enrolled in these programs saw their premium go down. 24% of drivers enrolled in telematics actually saw their premiums go up. And 45% of drivers saw no premium change. Auto insurance companies claim that by enrolling in telematics, drivers can get substantial savings—sometimes up to a 30% or 40% discount. However, those numbers are the maximum possible discounts, not guaranteed, and drivers can only achieve them if they do everything perfectly. The Maryland report concludes that the supposed savings from telematics are a mirage for many drivers, or are at least highly exaggerated.

Third, telematics programs collect a lot of data about drivers and their cars. A full list of all the factors collected is on pg. 8 of the report, but it includes information that goes well beyond the commonly reported factors. Your insurance company could collect information about your car’s battery level, fuel, idle time, altitude at which you drive, how often you use your turn signals, adaptive high beams, and a great deal of information about your phone use. To make matters worse, Maryland, like most other states, has no restrictions on what data can be collected by these programs and what insurance companies can use it for. They could use this data to nickel and dime consumers, use it when a claim is filed, use it for marketing other products, or sell it in the market to businesses that want to buy your data.

Finally, telematics data is often collected not by the auto insurance companies but by shadowy third party companies. According to the Maryland report, only 5 insurers directly collected the information; the other 11 companies contracted the collection out to other corporations. The companies claim that that there are strict processes and procedures in place to both maintain the security and privacy of data, but the Consumer Federation of America is skeptical.

So what should consumers do? We recommend caution when considering telematics programs, especially in light of this new report. While some consumers may pay lower premiums if they are excellent drivers, most consumers will not save money. And by participating in telematics, you are giving up a lot of your privacy and data without meaningful privacy protections. It is not unreasonable to accept that unaccountable insurance companies will use your information not just to score your driving but to score additional profits by marketing your data.

But Maryland and other states could make changes to ensure that consumer data and privacy are protected and that telematics more accurately prices insurance and benefits consumers. We urge policymakers to adopt reforms that allow telematics programs to only collect data relevant for insurance purposes, require that data only be used for insurance purposes, prevent the telematics data from being used in a way that unfairly discriminates based on someone’s race, ethnicity, or other characteristics, and ensures that drivers can review and challenge errors in the data.

As the first state to conduct research in this area, we are hopeful that the Maryland Insurance Administration will continue to investigate telematics and lead efforts to build consumer protection guardrails around its use.