The Securities and Exchange Commission (SEC) recently adopted rules to strengthen investor protections in the Special Purpose Acquisition Company (SPAC) market. CFA applauds the SEC for taking these important steps to protect investors, enhance transparency, and improve market integrity. Moreover, CFA commends the SEC for strengthening the final version of this rule to bring SPACs that are acting as illegal investment companies into alignment with the rules for inadvertent investment companies under the Investment Company Act (ICA), a change from the SEC’s proposal that CFA specifically advocated for in filed comments.[1]

As background, a SPAC serves as a vehicle for private companies to enter the public markets without going through the traditional IPO process. SPACs effectively function in two phases – the SPAC phase and the de-SPAC phase. In their first phase, SPACs function as mutual funds – a type of investment company. In their second phase, de-SPACs function as IPOs – the first time a private company is introduced to the investing public.

With these transactions, however, SPACs’ complex, opaque, and speculative qualities often lead to profound disadvantages and risks for retail investors, especially as compared to a SPAC’s sponsors and early institutional investors. As a result, many SPAC transactions have resulted in significant harm to investors when they lost significant value in the public markets after its sponsors and early investors had exited the company and liquidated their stakes.

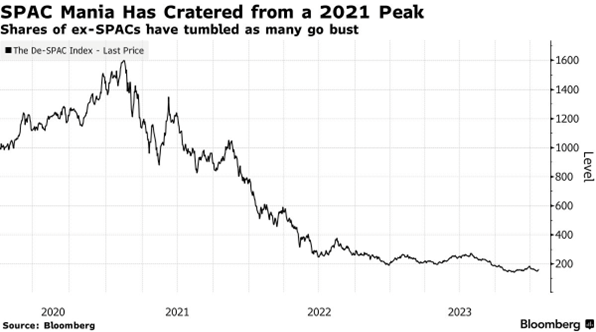

The risk and volatility of this market is further demonstrated by the reality that the once booming SPAC market, which peaked in 2021, has given way to a cratered SPAC market today.

Critically, during the initial stage of a SPAC transaction, nearly all SPACs meet the definition of an investment company, as they are engaged primarily in the business of investing, reinvesting, or trading of securities. And because these entities mirror the operations of investment companies, like money market mutual funds, they should adhere to the same requirements of the ICA as any other investment company. Indeed, the ICA imposes a comprehensive regulatory framework on investment companies which includes rules designed to protect investors whose funds are managed and controlled by another entity.

However, many SPACs have failed to follow even the most basic of ICA’s requirements and therefore operate as illegal investment companies. Among other violations, SPAC sponsors’ compensation structure is likely to be impermissible under the ICA, SPAC sponsors and their affiliates engage in conflicts of interest that are impermissible under the ICA, SPACs issue warrants with terms that are impermissible under the ICA, and many SPACs’ governance structures are impermissible under the ICA.

When the SEC proposed its new SPAC rules, it provided a new safe harbor under the ICA that would have provided special treatment to SPACs, allowing them to effectively function as investment companies for two years without having to comply with the investor protections afforded by the ICA. Accordingly, CFA raised strong objections to this part of the proposal, arguing that this safe harbor exceeded existing limits for inadvertent investment companies. CFA’s comment urged the Commission to significantly narrow the scope of any safe harbor and emphasized that SPACs operating outside the safe harbor should always be deemed in violation of the law.

In response to these concerns that were raised by CFA and others, the SEC adjusted its approach in the final rule, eliminating the proposed safe harbor.

In addition to this important adjustment, the final rule retained other investor protections from its proposal, and adopted reforms that will benefit market integrity writ large. For example, the rules will require additional disclosures about SPAC sponsors’ compensation and conflicts of interest, disclosures about possible dilution of investors’ shares, and other information that is vital to investors involved in SPAC transactions.

In conclusion, the SEC’s efforts to strengthen investor protections in the SPAC market is laudable, and CFA applauds the SEC for addressing concerns related to illegal investment company practices within the SPAC market.

[1] See Consumer Federation of America, Comment Letter Re: Special Purpose Acquisition Companies, Shell Companies, and Projections at 1 (June 13, 2022), https://bit.ly/3UsDq5W.

[2] Bailey Lipschultz, SPAC Industry Fears SEC’s Rules Could Finish Off Ailing Market, Bloomberg (January 24, 2024), https://bit.ly/47Yjw5U.