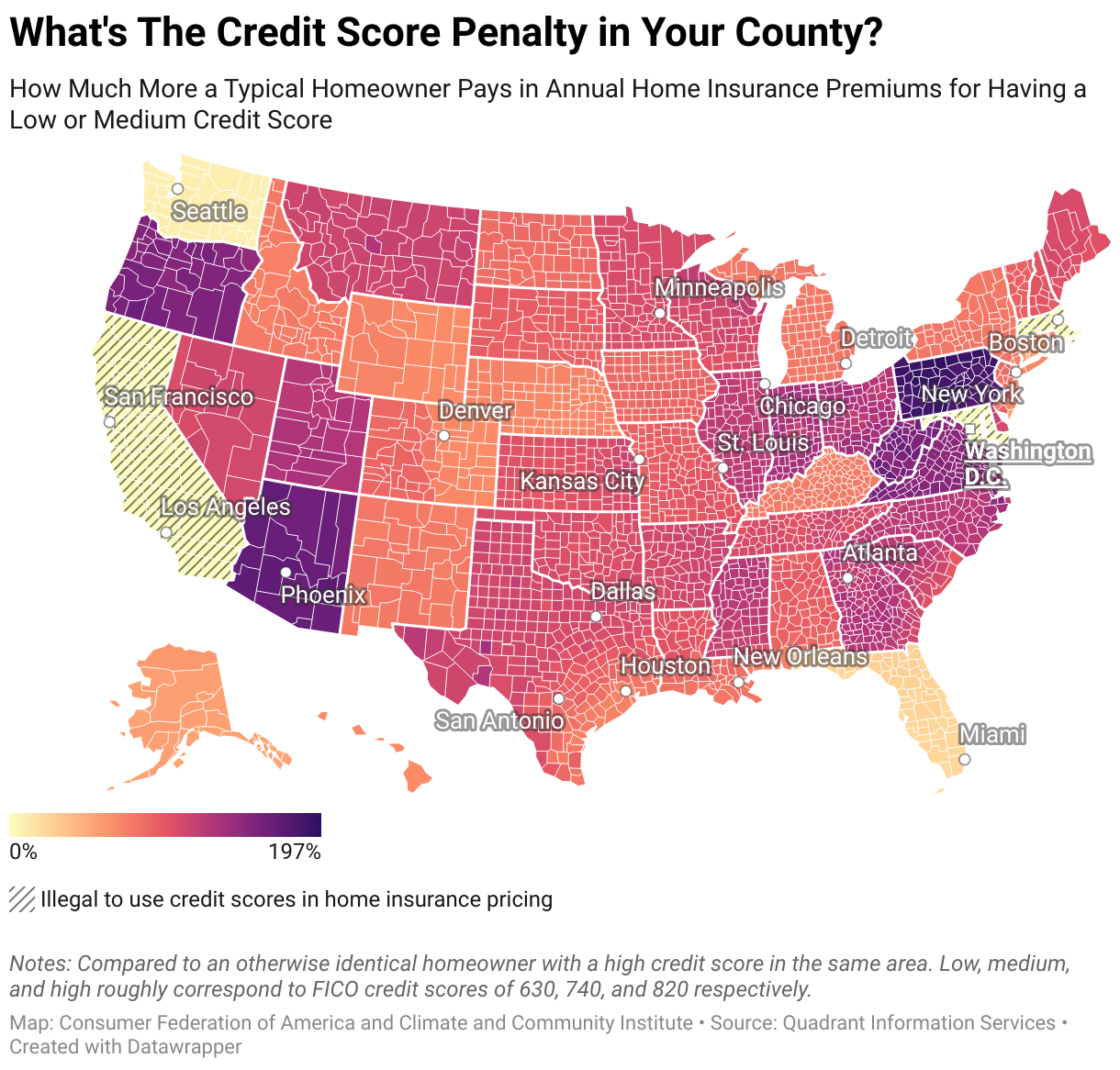

Homeowners insurance protects consumers’ homes and belongings in case of unexpected damage or a natural disaster. Lenders require homeowners with a mortgage to always maintain this coverage, meaning that most homeowners have no choice but to carry insurance. But insurance costs have skyrocketed in recent years, leaving many homeowners struggling to find affordable options. Many others find themselves without coverage when their long-time insurer refuses to renew their policy and may struggle to find any insurer that will cover them. While more frequent and severe climate-driven disasters are an important driver behind increasing homeowners insurance premiums, they are only part of the story. Insurance companies take into account dozens (and sometimes hundreds) of factors when they price insurance. How much an insurance company charges any given homeowner for their insurance is also shaped by the qualities of their home, such as the roof’s age, the construction materials, and how much it would cost to rebuild. But even two neighbors with the exact same type of house may get charged wildly different insurance premiums, since most insurance companies consider individual factors as well to price insurance. These factors include customers’ marital status, occupation, and, as this issue brief shows, credit history.

This issue brief, which builds upon an academic paper on credit scores by Professor Nick Graetz of the University of Minnesota, examines how insurance companies use consumers’ credit scores (also called “credit-based insurance scores”) to price homeowners insurance and how this unfair practice penalizes certain consumers.

The brief shows that:

- Insurance companies charge the typical homeowner $1,996 dollars (or 99 percent) more each year just for having a low credit score;

- Homeowners in Pennsylvania, Arizona, Oregon, and West Virginia face the largest penalty for having a low credit score;

- It is often more expensive to have a low credit score than to live in an area with a high disaster risk.