Washington D.C. — The oil price spike of the past year, which saw gasoline prices increase by over a dollar from the summer of 2010 to the summer of 2011, will drive household expenditures on gasoline to a record average of $2900 this year. Crude oil is about $30 higher than costs or historic trends justify, generating needlessly high prices for petroleum products that will drain about $200 billion out of the economy.

This $200 billion drain is over one percent of gross domestic product and almost 2 percent of consumer spending. “Since consumer spending is the main driver of the U.S. economy, when speculators, oil companies and OPEC rob consumers of that much spending power, the inevitable result is a dramatic reduction of economic activity and employment,” said Mark Cooper, CFA’s Research Director and author of the report.

The report, entitled Excessive Speculation and Oil Price Shock Recessions: A Case of Wall Street “Déjà vu All Over Again,” notes that every oil price spike since World War II has caused an economic recession and the spike of 2010-2011 has been worse, on a sustained basis, than even the price spike of 2007-2008, which contributed to the worst recession since the great depression. A 2 percent reduction in consumer spending on goods and services translates into the loss of hundreds of thousands of jobs.

The spike in oil prices has not been caused by natural market supply and demand. In fact, U.S. demand for oil has declined since 2005, while global demand has grown less than 4 percent. In addition, global oil reserves have been growing faster than consumption and the reserve-toconsumption now stands at a higher level than it has been in a quarter of a century. Today, OPEC spare capacity is almost three times as great as it was in 2008.

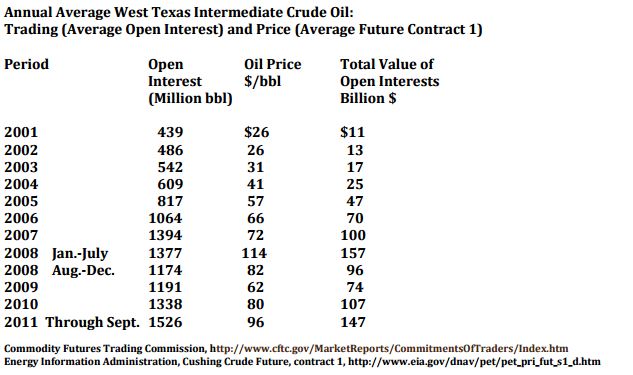

At the end of 2003 the price of West Texas Intermediate (WTI) crude oil (the “benchmark” for U.S. oil) was a about $30/bbl and the value of outstanding futures contracts (called “open interests”) for WTI was less than less than $20 billion. Wall Street firms like Goldman Sachs and Morgan Stanley and hundreds of hedge funds led the charge into the oil markets, creating products that “financialized” commodities. Index funds and pension funds soon followed. In July of 2008, when WTI hit its peak price above $140/bbl, the average value of open positions at the peak in 2008 was over $150 billion. Eight times as much money chasing the same amount of oil is a prescription for price escalation.

In the third quarter of 2008, as pressure from congress and the public outcry over oil prices forced the Commodity Futures Trading Commission to begin investigating excessive speculation, speculative money fled the market. By mid-September, before Lehman Brothers went bankrupt precipitating the financial meltdown, the value of open interests had declined by about 50% and the price of oil had fallen over 50%. By the end of the year, oil prices were below $40/barrel, a decline of 75%.

The annual averages for trading and prices for West Texas Intermediate Crude oil are described in the following table and analyzed in detail in the report.

“That is a classic bubble,” Cooper said, “but Federal regulators moved slowly to make permanent changes in the rules governing oil trading, so the bubble began to reflate in late 2010. The value of open positions has doubled in the past two years, while U.S. demand has continued to decline and global demand remains flat. Speculation has pumped the price of oil up again, putting the brakes on economic growth.”

“We have been hearing a lot of over-heated rhetoric recently about job-killing regulations,” Barb Roper, CFA’s Director of Investor Protection, said. “This report provides a timely reminder that it was weak regulation that landed us in our current economic mess, and it will take a strong policy response to restore the economy to health. Restraints on excessive speculation are just one component of that policy response, but they are a necessary component.”