Washington, D.C. — Today, in response to a new report on discriminatory auto loan markups by American Honda Finance Corporation, the Consumer Federation of America calls on Honda and its dealers to end undisclosed lending practices that discriminate against AfricanAmerican car buyers. “In response to litigation and public pressure, other auto loan companies are beginning to curb discriminatory auto loan practices, and Honda should do the same,” said CFA Executive Director Stephen Brobeck.

The report, prepared by Dr. Mark Cohen of Vanderbilt University, is based on examination of records of 383,652 AHFC customers over the period, June 1999 to April 2003. It concludes that African-American borrowers consistently paid higher “finance markup charges” over average than white customers when they finance their cars at dealerships through AHFC. The study controlled for factors such as term of loan, type of vehicle, creditworthiness of borrower, and geographic area.

Auto loan markups occur when lenders allow car dealers to mark up auto loans above the “buy rate” reflecting the actual creditworthiness of borrowers. A growing body of evidence reveals that hundreds of thousands of consumers, perhaps millions, have trusted auto finance companies and car dealers to charge them fair and reasonable rates only to then be subjected to markups that, in the past, have often exceeded five percentage points. A report, which was released by CFA, the National Council of La Raza, and the Rainbow-PUSH Coalition early this year, estimated that these overcharges cost consumers at least $1 billion annually.

The harm of loan markups goes well beyond their discriminatory impact on AfricanAmericans and Hispanics and affects all consumers noted Stuart Rossman, Director of Litigation at the National Consumer Law Center (NCLC), and a co-counsel for plaintiffs in several auto loan markup cases: “In addition to more costly monthly payment obligations and greater indebtedness, markup policies expose all customers to a higher incidence of various harms including ineligibility for future financing programs through other lenders, exposure to higher credit costs under tiered pricing systems used by other lenders, and more frequent delinquencies and defaults, resulting in increased rates of repossession and bankruptcy.”

The Reverend Jesse Jackson, President of the Rainbow/PUSH Coalition, promised that “Rainbow/PUSH will continue to advocate for car interest rates that are not determined by one’s skin color or economic status.”

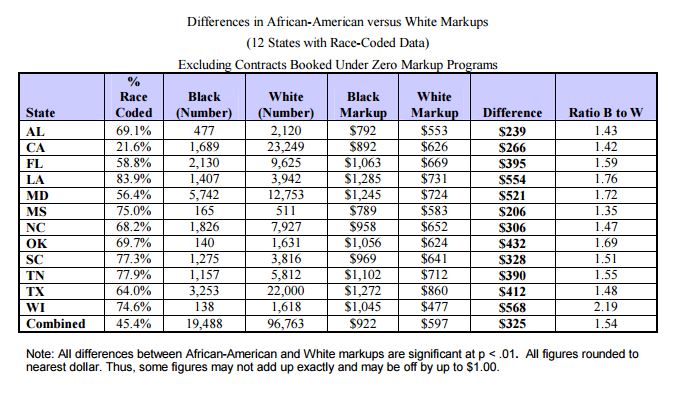

Honda Auto Loan Markups Are Much Higher for African-Americans

Dr. Cohen’s report contains the following important findings:

- 43.3 percent of African-American Honda Finance borrowers were charged a markup, compared to only 22.2 percent of white borrowers.

- African-American borrowers on average paid more than two times the amount in subjective markups compared to whites — $557 versus $227, a difference of $330.

- Honda used a unique practice in which customers from different credit tiers were charged different markups. While most new car buyers were limited to either a zero or two percentage point markup, those from the least creditworthy tier could be charged a 3.5 percentage point increase. There appears to be no business justification for this differential markup policy since differences in creditworthiness are reflected in the “buy rates.”

- Honda does not prohibit the practice of “tier bumping,” where dealers can arbitrarily assign customers a higher credit risk rating when arranging financing. Because of the credit tier pricing policy, customers who were given this higher rating were effectively subjected to two loan markups reflecting piggybacked discriminatory policies.

Consumer Leaders Ask Honda to Reform Its Practices

The Cohen report analyzes Honda lending data disclosed in a discrimination lawsuit against the lender filed in federal court in Tennessee. In addition to NCLC, this lawsuit was filed by the law firm of Cunningham, Bounds, Yance, Crowder and Brown and the law offices of Clint Watkins, Michael Terry and Wyman Gilmore. A similar lawsuit was filed in California state court by former U.S. Assistant Attorney General for Civil Rights, Bill Lann Lee, of the firm Lieff, Cabraser, Heimann and Bernstein, who is counsel for plaintiffs in Pakeman v. American Honda Finance Corporation.

Also in California, Consumers for Auto Reliability and Safety, a non-profit auto safety and consumer advocacy organization, is promoting state legislation, AB 1839, authored by California Assemblymember Cindy Montanez, that will be the strongest regulation in the nation to curb auto dealer/lender markups. AB 1839 would curb markups at 2 percentage points for loans of 60 months or less, and at 1 percentage point for longer loans.

In response to similar litigation and requests by consumer groups, state attorneys general, and even industry experts to end the markups, several auto finance companies have revised their lending practices. For example, General Motors Acceptance Corporation imposed a 2.5 percentage point cap on the dealer markup as a result of a settlement negotiated in a lawsuit alleging discrimination in the markup. And, Ford Motor Credit Corporation subsequently lowered its cap to 2.5 percentage points following findings of discrimination and consumer gouging in FMCC auto finance markup practices.

While heartened by this progress, and by consumer education efforts undertaken and funded by the auto loan finance companies, consumer groups still object to auto loan markups in principle. “Creditworthiness is entirely taken into account by the buy rate at which lenders are prepared to extend credit to car buyers,” said Brobeck. “Dealers should be permitted to charge lenders a reasonable processing fee but not to arbitrarily mark up loan rates above the buy rates and to do so without disclosing these markups,” he added.

“What is striking here is that, while the nation’s top two auto lenders have begun correcting the practice, Honda has refused to respond,” said Brobeck. “Our hope is that the findings of this latest report will encourage Honda to change its abusive lending practices,” he added.

CFA is a federation of some 300 consumer groups that seeks to advance the consumer interest through research, education, and advocacy.

A summary of the Cohen report is available at: www.consumerfed.org/hondasummary.pdf The full Cohen report can be found under the heading AHFC at www.nclc.org/initiatives/cocounseling/examples_litigation.shtml

.

.