Auto finance is at a breaking point in our country. Americans owe more than ever in auto debt–over $1.6 trillion–and the economic pressure cooker that American households are in is rapidly jeopardizing their ability to avoid disastrous auto lending outcomes like delinquency and repossession. These precarious dynamics mean that lenders’ activity will have increasingly significant impacts on families whose budgets are stretched ever thinner, and our financial regulators should be carefully watching lenders’ conduct to ensure that borrowers are not exploited.

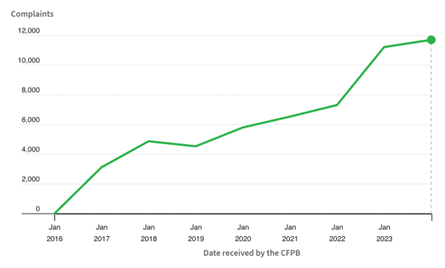

Instead, under Trump’s leadership, our federal financial watchdog is doing the opposite, and is taking steps to significantly scale back the Consumer Financial Protection Bureau’s supervision of auto lenders. Auto finance is already notoriously opaque, particularly in the nonbank sector. Under the existing supervision program, the CFPB’s Supervisory Highlights reports are one of the few tools available to policymakers and legislators that provide insight about conduct in the market. But at this critical juncture for car buyers, CFPB Director Vought is abruptly signaling that auto lenders’ activity and treatment of struggling borrowers is not worth broader scrutiny, despite the fact that auto related CFPB complaints are at an all time high.

In 2015, the CFPB finalized a rule that clarified its ability to supervise nonbank auto finance companies that originate 10,000 loans per year and therefore qualify as “larger participants” in the marketplace. Through these supervision exams, the CFPB has provided redress to victims of illegal auto lending conduct, identified widespread auto lending abuses that plague the industry, and stimulated compliance with consumer financial protection laws. But the Advance Notice of Proposed Rulemaking published by the CFPB on August 7 seeks to shrink the Bureau’s nonbank larger participant auto lending supervision jurisdiction to as few as five lenders. This could reduce the number of supervised auto lenders by 90%, removing a powerful incentive to comply with consumer financial protection laws for a large portion of the industry. Removing this oversight will leave us without a proverbial smoke detector to correct insidious conduct before it turns into bigger fires that merit large scale enforcement actions (which the Bureau is also turning its back on).This is part of a larger effort by the Bureau to roll back their entire supervision program, including supervision of banks, other markets, and risky conduct.

The Bureau’s Supervisory Highlights describe noteworthy illegal conduct by auto lenders, but they now serve as an unfortunate omen for some of the conduct that will be permitted to fester if the Bureau dismantles a large swath of its auto lending supervision program:

Repossession and collections. Losing a car to repossession is devastating. Without access to transportation, borrowers lose their jobs, their credit is wrecked, they face continued collections and judgments, and buying a replacement car is extremely difficult. Auto debt collection activity and repossessions expose borrowers to particularly harmful conduct, as highlighted by CFPB supervision:

-

- Using starter interrupt devices (that beep or prevent a vehicle from starting if the lender asserts that the consumer is late on payments) when consumers were not actually behind on payments

- Illegally threatening to suspend the borrower’s drivers license or vehicle tags when borrowers were late

- Repossessing cars after the borrower made sufficient payments or where the servicer agreed to cancel the repossession order;

- Holding borrowers personal belongings in the repossessed car hostage until they paid an illegal storage fee;

- Charging excessive repossession fees, making it difficult or impossible for consumers to reinstate their loan agreement.

Add-on abuses. These products, like window etching, service contracts, or fabric protection, increase the cost of an auto finance contract by hundreds or thousands of dollars. They are frequently overpriced, and many car buyers are tricked or coerced into purchasing them. CFPB supervision repeatedly identified all manner of add-on abuses by lenders, including:

-

- Charging interest on add-ons that were added to the contract without the buyer’s consent

- Refusing to cancel add-on products or using onerous cancellation processes (such as requiring a borrower to visit a dealership in person twice to cancel)

- Financing add-ons that were completely void and worthless to the consumer

- Miscalculating rebates owed on canceled warranty products, affecting the calculation of deficiency balances

GAP products. GAP (guaranteed asset protection) is an add-on product with its own host of issues. GAP is intended to cover the difference between the amount you owe on your auto loan and the amount the insurance company pays if your car is stolen or totaled. But when your loan contract ends early–the loan is paid off, refinanced, or the car is repossessed–the lender owes you the unused portion of the GAP coverage. CFPB supervision has identified numerous problems with lenders’ handling of GAP products:

-

- Failing to refund unused GAP premiums or miscalculating refund amounts

- Violating the GAP contract by accepting monthly payments even after the vehicle was declared a total loss

- Collecting payments for GAP products where the consumers’ vehicles did not even qualify for GAP coverage

- Misrepresenting the benefits of GAP products

Hidden and deceptive fees. CFPB exams root out illegal conduct that consumers would have almost no way of learning about on their own. CFPB supervision identified instances of fees in auto finance contracts that were worthless, fraudulent, or hidden from the consumer.

-

- Payment processing fees that far exceeded the cost of servicing payments (“pay to pay fees”).

- Collecting interest on fraudulent loan charges, such as options that were not present on the vehicle.

- Charging consumers for unnecessary force-placed insurance policies and collecting premium payments for force-placed insurance after repossessions.

- Charging late fees post-repossession, and overcharging late fees in excess of the contractual capped amount.

Credit reporting. Credit scores are economic gatekeepers. When auto lenders violate their statutory obligations to accurately furnish information to consumer reporting agencies, the harm to consumers goes well beyond that individual loan. CFPB supervision has repeatedly found credit reporting errors by auto lenders:

-

- Reporting information with actual knowledge of errors about amounts past due, scheduled monthly payment amounts, and inaccurate dates of first delinquency;

- Continued errors in delinquency reporting, despite determinations that the information was furnished inaccurately or incompletely;

- Failing to implement reasonable policies and procedures concerning the accuracy and integrity of furnished information, such as document retention policies and documenting the process for identifying frivolous or irrelevant disputes

The Bureau is accepting comments on its ANPR until September 22, 2025. The link for submitting comments can be found here. After that, the next step in this process will be for the Bureau to publish a Notice of Proposed Rulemaking, which is where it will set forth a more definitive plan for reducing its supervision of nonbank auto finance companies.