As CARES Act Passes, Important Consumer Protection Measures Unaddressed

Congress passed sweeping legislation last week, the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), to address the economic fallout from the COVID-19 pandemic. While necessary to provide desperately needed funding to the health care system, to provide unemployment insurance to displaced workers, and to infuse money into the economy, the bill leaves important measures to address consumers’ health and financial well-being largely unaddressed.

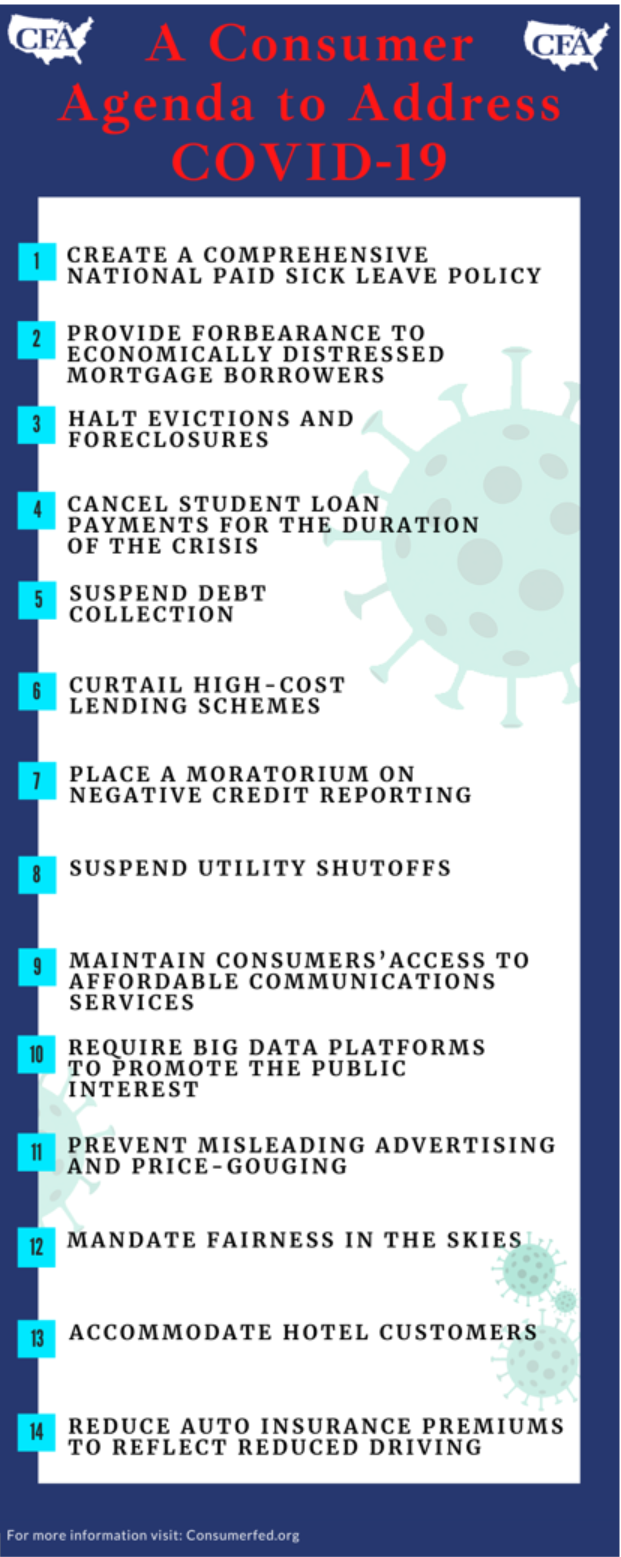

CFA wrote to the President and Congress as the COVID legislation was being drafted to urge inclusion of measures to address a wide range of critical consumer protection issue. Many of the measures that are most needed were included in the House COVID-19 response bill, but the Senate failed to include them in their Senate bill. A few of CFA’s priority issues – most notably paid sick leave and assistance for homeowners and renters – were at least partially addressed in the bill.

“We acknowledge the urgency of passing a bill and doing so quickly,” said CFA Legislative Director and General Counsel Rachel Weintraub, “but the CARES Act must be just a first step. A new round of economic assistance will be needed, and consumers’ needs must be addressed in that legislation through the addition of necessary consumer protections.”

The Bill Offers Progress on Paid Sick Leave and Assistance for Homeowners

The bill took limited steps, along lines advocated by CFA, to:

- Create a comprehensive national paid sick leave policy.

Lack of paid sick leave encourages tens of millions of workers, including restaurant staff, rideshare drivers, retail cashiers, farmworkers, and others, to continue working when they are sick, which helps to spread foodborne illness and other diseases. This threatens to nullify hard won gains from social distancing. In response, CFA advocated adoption of a comprehensive paid sick leave policy.

Between the CARES Act and the previous Families First Coronavirus Response Act, Congress has provided up to 80 hours of paid sick leave for employees who are unable to work either because of their own illness or to care for a child, but with significant gaps. Employers do not have to provide full pay, the Department of Labor can exempt businesses with fewer than 50 employees, and the Office of Management and Budget can exempt executive branch employees.

“More than ever, offering comprehensive paid sick leave to food and other ‘essential’ workers is in every consumer’s own self-interest,” said Thomas Gremillion, CFA Director of Food Policy. “By exempting large employers and potentially many others, and failing to provide for paid leave beyond a couple weeks under a narrow range of circumstances, Congress has left workers and all of us who depend on them shamefully vulnerable to this pandemic.”

- Protect homeowners and renters from economic hardship.

Workers who lose their jobs, have to stop work because of illness, or have paychecks suspended during the COVID-19 crisis may struggle to make mortgage and rent payments. CFA recommended adoption of measures to provide forbearance to economically distressed mortgage buyers and to halt evictions and foreclosures. The CARES Act includes limited measures to address those concerns.

On the plus side, consumers with federally-backed mortgages – Fannie Mae, Freddie Mac, Federal Housing Administration, Veterans Affairs, or Rural Housing loans – can seek and receive payment forbearance for 180 days, renewable for another 180 days, by contacting their servicer and attesting to being impacted by the COVID-19 emergency. Renters living in properties with federally backed mortgages also can get rent relief if the owners seek and get forbearance on their loans.

On the other hand, the bill doesn’t cover loans held in bank portfolios or those that are in private label securities. That’s a total of around 15 million loans outstanding. This raises the possibility that consumers with different loans will get different treatment. Also, there is no clear provision of badly needed liquidity for nonbank servicers, who do the great majority of the FHA, VA and RHS loans business through Ginnie Mae. “As people stop paying their mortgages through forbearance, and servicers are required to pass through the amounts owed to investors, they will rapidly run out of cash,” warned CFA Director of Housing Policy Barry Zigas.

“The bill entitles consumers to temporary forbearance of mortgage payments without documentation or paperwork, which is a huge help to homeowners who have been laid off or suffered loss of income,” Zigas said. “But the bill falls short in failing to cover all mortgages, not just government-backed loans. The failure to include specific liquidity relief for lenders could cause a new round of business failures and investor exposure to losses, which would severely undermine the housing finance system.”

The Bill Provides Limited Assistance for Student Borrowers

The CARES Act exempts some, but not all, federal student loan recipients from making payments on those loans for six months, with the interest waived during that six-month period. But borrowers will still need to make up the payments later. And the exemption does not apply to all student loans. Perkins Loans, FFEL loans held by a bank or other financial institution, and private student loans are not eligible.

CFA had called for all student loan payments to be canceled for the duration of the crisis, with the government making payments on their behalf. “Expanding this relief to student borrowers will be an important priority in any future bill,” Weintraub said.

Other Consumer Protections Are Missing Entirely

Missing from the bill are the following consumer protections identified by CFA as essential to protect the most vulnerable from financial hardship as a result of the economic fallout from the COVID-19 pandemic:

- The bill does not curtail high-cost lending schemes. CFA had called for new consumer protections to apply to high-cost credit, such as payday loans, refund anticipation loans, and car title pawns, to ensure that vulnerable consumers aren’t trapped in a cycle of debt. The bill does nothing to address this concern. Instead, federal bank regulators issued small dollar bank lending guidance that lacks protections needed to ensure loans do not trap borrowers in a cycle of debt.

- The bill fails to suspend debt collection or place a moratorium on negative credit reporting. The bill does little to protect consumers’ credit records during the crisis. While it includes a provision regarding credit reporting, it is weaker than the current industry standard for disaster victims.

- The bill fails to protect against utility shutoffs. To assist those who struggle to pay utility bills for essential services such as electricity, gas, water, and communications as a result of the economic fallout from the crisis, CFA advocated a moratorium on all utility shutoffs during the crisis. The bill does not address this concern.

- The bill fails to maintain consumers’ access to affordable communications services. At a time when remote communications are more critical than ever, the CARES Act fails to provide broadband subsidies for low-income Americans and fails to include any requirement for broadband providers to drop data caps, overage fees, or throttling practices to keep people connected. Nor does it take any steps to require big data platforms to promote the public interest or to crack down on misleading advertising and price-gouging.

The bill provides extensive financial assistance to corporations, but without doing enough to ensure that consumers’ interests are protected.

Most notably, the bill does nothing for airline passengers. It does not require airlines that receive assistance to refund consumers’ money if they want to cancel their tickets, nor does it protect consumers from being gouged for fare differences and other charges if they need to change their flights. It also fails to address systemic problems in the airline industry such as the lack of price transparency. “The airlines are getting big bucks and passengers are getting short shrift,” said CFA Director of Consumer Protection and Privacy Susan Grant.

Nor does the CARES Act condition support for hotel chains on their agreement to honor requests for room and event cancelations without penalty, as CFA had advocated. On the other hand, Alaska became the first state to take steps to ensure that consumers, not insurance companies, reap the financial benefits from reduced driving that results from the crisis. (See more below.)

“Now that Congress has passed this first and desperately needed economic assistance package, it must quickly get to work on a more comprehensive package to aid consumers. We look forward to working with members to ensure that these critical measures are quickly adopted,” Weintraub said.

“Protecting consumers is not just a matter of economic justice, it is also the best way to protect the economy,” added CFA Executive Director Jack Gillis. “CFA will continue to fight to ensure that these critical measures are adopted.”

{kind=link}

Social Distancing + Less Commuting Should Lower Auto Insurance Premiums

As millions of Americans shelter in place, work from home, or face business closures and layoffs, the number of cars on the road has fallen precipitously and, as a result, the number of daily car accidents can be expected to diminish dramatically. This reduction in claims activity results directly from consumers’ reduced mileage, a key risk factor in safe driving, and the savings should be returned to people impacted by COVID-19 restrictions on movement, argue CFA Director of Insurance J. Robert Hunter and CFA Insurance Expert Douglas Heller.

Hunter and Heller, together with Center for Economic Justice, wrote to state insurance regulators across the nation last month, urging them to direct insurance companies to offer customers premium offset payments to reflect the immediate reduction in expected insurance claims as a result of COVID-19 restrictions keeping drivers off the road.

“Imagine if the population density of New York City transformed into the population density of Idaho overnight. In terms of drivers on the road, that is exactly what is happening in many urban and suburban areas,” the groups wrote.

In the letter, the groups urged state insurance regulators to adopt and implement five actions to provide critical relief to drivers impacted by Coronavirus.

- Direct auto insurers in your state to contact their policyholders and offer premium relief to any policyholder who can demonstrate or attest that their miles driven has been impacted by COVID-19 safety measures.

- Inform insurers that such premium relief is permitted by state law and is not a rebate.

- Direct insurers to file with your department the notices they will send to policyholders and the process and timing they will use to provide relief.

- Direct insurers to report on a monthly basis anonymized information on each request for relief received, including

- Date of request,

- ZIP Code of policyholder,

- Original annual premium of policy,

- Whether request was granted or rejected,

- If rejected the reason for rejection,

- If granted the amount of premium relief.

- Encourage drivers to contact their auto insurers for relief as part of your Department’s COVID-19 consumer outreach and education.

“The likelihood of a motor vehicle accident drops radically when the number of cars on the road drops radically. Consumers who paid auto insurance premiums based on driving an estimated 1,000 miles a month but who are now driving 200 miles a month because they are forced to work at home or their business has closed should get relief from their auto insurers. Windfall profits for auto insurers and excessive auto insurance premiums should not be another harm visited upon consumers from COVID-19,” stated Hunter.

“While everyone is making sacrifices, insurance companies stand to make a windfall if they continue to collect auto insurance premiums as if nothing has changed,” said Heller. “If you are not commuting to work every day anymore, you shouldn’t be charged as though you were. Insurers should begin offering consumers credit for the overcharges that are accruing during this crisis, or regulators should make companies do it.”

Coronavirus Heightens the Need to Protect Privacy

Consumer and privacy organizations, including CFA, sent a letter to members of Congress last month urging them to take steps to protect our privacy and secure our personal data, including location and health data, in any response to the COVID-19 emergency.

“Allowing access to personal data, particularly health data, without guardrails could threaten fundamental rights and liberties and open the door to data exploitation that could violate civil rights and harm vulnerable populations. It is not enough to expect that corporations will keep the promises they make in their unregulated terms of service. There must also be federal protections for new data collection, processing and sharing, and real consequences for violations,” the letter states.

Tech companies routinely collect location data, which might be shared with public health, transportation and law enforcement authorities, the groups warned, and personal health data unrelated to the coronavirus might be improperly collected and shared, as well as data linked to commercial transactions. They outlined a set of principles that should govern policy in this area, including that any mass data collection must be deemed necessary for public health and proportionate to the need.

“Too often in times of emergency there is an impulse to collect personal data without thinking through what’s really necessary and what to do with the information once it’s no longer needed for the intended purpose,” said CFA Consumer Protection Director Susan Grant. “We can protect public health and privacy if we set some sensible guardrails in place.”