Investors’ mutual fund purchase practices bear little resemblance to those recommended by investor educators, according to a recent survey commissioned by Consumer Federation of America (CFA).

“The differences between expert recommendations and actual investor behavior suggest that a comprehensive review is needed to determine how key educational messages can be delivered more effectively, whether certain messages are simply unrealistic, and how educational materials can better target specific groups of fund investors,” said CFA Director of Investor Protection Barbara Roper.

To further that goal, CFA plans to distribute the survey report to securities regulators, investor advocates and educators, industry representatives, and others in order to promote a broad-based discussion of its implications for mutual fund disclosure requirements, industry information practices, and investor education efforts.

With policymakers, investor advocates, and industry groups currently exploring how the Internet can be harnessed to promote improved fund disclosure, the survey also looked at investors’ access to and willingness to use the Internet for various mutual fund purchase-related activities. On the one hand, the survey found that the vast majority of investors have access to the Internet, and most are willing to use the Internet for at least some purchase-related activities. At the same time, it found resistance to using the Internet among certain groups of investors, particularly older investors, and for certain types of activities, including receiving disclosure documents from financial professionals.

“Clearly, there are transitional issues that must be dealt with in any policy to promote Internet disclosure,” Roper said. “We need to better understand the reasons for and intensity of this resistance to using the Internet if we are to develop policies to promote Internet disclosure that benefit all investors.”

The survey was conducted in September 2005 by Opinion Research Corporation. It was administered to a representative sample of 2,048 adult Americans, 43 percent of whom identified themselves as current owners of mutual funds. The survey is part of a CFA project funded by the NASD Investor Education Foundation exploring mutual fund investors’ information practices and preferences.

A distinguished advisory group that included representatives of the fund industry, investor advocates, state, federal, and industry regulators, and others advised the project, assisting CFA in both the development and interpretation of the survey. As a precursor to the survey, CFA also conducted a literature review examining the factors experts recommend investors consider when purchasing a mutual fund and the degree to which that information is readily available to investors.

Most Fund Investors Do Not Follow Expert Recommendations

Among the key discrepancies between expert recommendations and investors’ actual mutual fund purchase practices revealed by the survey:

- Many investors appear to give relatively little weight to factors such as mutual fund costs and risks that investor educators and regulators consider of top importance.

- Although regulators and educators typically recommend that investors carefully review the prospectus before making a fund purchase, most investors indicate that they do not find the prospectus of great value when selecting a fund.

- Those who purchase funds through a financial professional generally do not do the additional research on recommended funds that educators and regulators advise.

“In some cases, the survey findings may reveal a failure on the part of investors to take important steps to protect their interests,” Roper said. “In these cases, the challenge for investor educators is to figure out how to convey essential information more effectively. In other cases, however, the problem may be that the expert recommendations are simply unrealistic or fail to reflect the different needs of different types of fund purchasers.”

“The Securities Exchange Commission is currently engaged in a timely top-to-bottom review of mutual fund disclosure requirements,” Roper added. “We encourage the Commission to consider these survey results as they explore issues related to the appropriate content, format, and presentation of mutual fund disclosures. But our findings also suggest that a similarly comprehensive review of investor education messages is needed.”

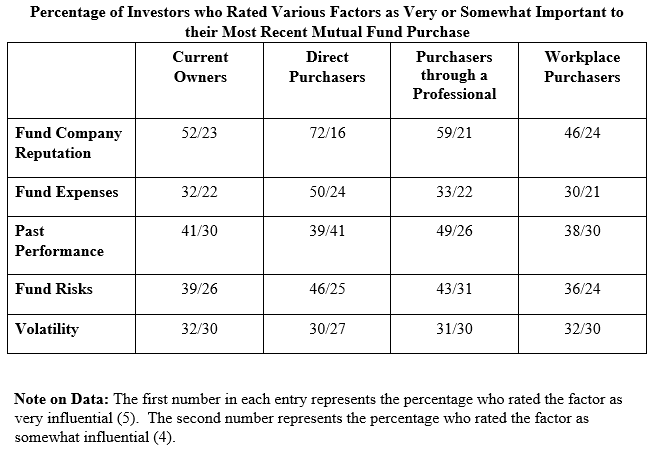

Factors Considered

Virtually all financial experts list a fund’s expenses and its risks, including the volatility of its past returns, among the key factors for investors to consider when selecting a fund. According to the survey, however, only a third of current fund owners considered either cost or volatility to be very important when making their most recent mutual fund selection, and just four in ten considered the fund’s risks to be very important. Most investors indicated they gave greater weight to fund company reputation and the past performance of the fund compared with that of other funds, factors experts often advise investors to consider, but typically relegate to a second tier of importance for evaluating funds.

“Few messages have been more consistently conveyed than the importance of comparing costs when purchasing funds, yet only a third of investors indicate they considered costs very important when purchasing a fund,” Roper said. “Since seemingly small differences in costs can result in large differences in returns over time, this suggests that more thought needs to be given to how to convey this message more effectively. Among the approaches that deserve consideration, in our view, is provision of more comparative cost information along with better information on the long-term impact of costs. Another question that should be explored is whether simplification of expense disclosures would contribute to better understanding of costs.”

Use of Written Information Sources

Experts almost universally recommend that investors carefully review the fund prospectus, or at least the information contained in the risk-reward summary, before purchasing a mutual fund. In addition, investors have a variety of written materials available to assist them in selecting mutual funds, including fund summary documents prepared both by the fund companies and by independent parties, ranking services such as Morningstar and Lipper, and newspaper and magazine articles evaluating funds. In addition, many fund companies advertise widely, often including performance information and fund ratings in the ads.

The survey asked current mutual fund owners how influential each of these documents was in their most recent mutual fund purchase. Supporting the view that mutual fund investors do relatively little research when selecting mutual funds, none of these documents was viewed as highly influential by most current fund investors.

The highest ranking was given to the prospectus, with 37 percent of direct purchasers rating it as highly influential. When those who ranked the documents as either highly or somewhat influential were combined, only the prospectus and the fund summary were rated as at least somewhat influential by half of investors in a particular purchase group. Specifically, 55 percent of direct purchasers indicated the prospectus was at least somewhat influential to their most recent purchase, and 55 percent of those who purchased funds through a financial professional rated a fund summary document as at least somewhat influential.

On the other hand, the survey did not support the conventional wisdom that many investors simply select funds from advertisements. Strong majorities (71 to 75 percent) in all three purchase categories said ads were either not very or not at all influential.

“Fund investors have a wealth of valuable information available to them from a variety of sources. In particular, both the fund industry and independent third parties have found innovative ways to use the Internet to improve the presentation of key information.

Unfortunately, most investors do not appear to be making good use of this information,” Roper said. “The SEC’s current review of fund disclosure requirements could help to make these documents more user-friendly. In addition, educators should explore better ways to direct investors to valuable resources.”

Reliance on Recommendations

Investor educators, regulators, and other experts typically advise investors to research the funds recommended to them by financial services professionals on the grounds that some professionals may have conflicts of interest that could bias their recommendations. According to the survey, however, investors typically do little such independent research.

- Nearly three in ten current mutual fund owners who purchased most of their funds from a financial services professional said they relied totally on that professional’s recommendation without doing any additional research (28 percent).

- More than a third (36 percent) said they relied a great deal on the recommendation of the financial services professional, but reviewed some written material about the fund before the purchase.

Another 28 percent said they relied a fair amount on the recommendation but did a significant amount of research on their own before making the purchase. Women were more likely than men to say they relied totally on the recommendation of a professional, while men were more likely to say they relied a great deal on the professional’s recommendation.

“One of the chief reasons investors choose to work with a broker, financial planner, or investment adviser is so that they won’t have to research their own investment selections,” Roper said. “Telling these investors to compare costs, risks, investment strategies, and past performance of the funds they are considering may be sound advice, as the recent mutual fund sales scandals make clear, but it is advice that seems unlikely ever to be widely heeded.

“A far more realistic approach, in our view, is to educate these investors on how to choose and work with a financial professional,” Roper said. “Unfortunately, investors currently can’t easily get the information they need to assist them in making this all-important selection. CFA urges the SEC to make it a top priority to develop a uniform, plain English up-front disclosure document that investors can use to determine the nature of services provided, the method of compensation, the potential conflicts of interest, the legal obligations, and any disciplinary record for brokers, investment advisers, and financial planners alike.”

Better Targeting of Education Materials Needed

As the above example illustrates, one issue raised by the project is the degree to which investor education materials fail adequately to distinguish between different types of mutual fund purchasers. “People who purchase funds through workplace-based retirement plans, through financial services professionals, or directly from the fund company do so under very different circumstances,” Roper said.

- For workplace purchasers, who rarely have more than a few funds in each category to choose among, the most important information will likely relate to how to choose the right fund categories, rather than the best fund of a particular category, CFA noted.

- Those who purchase through professionals are more likely to profit from information that helps them to make a sound choice of professionals, according to CFA.

“Only the tiny proportion of fund investors who invest directly are well served by the current approach, and even they seem largely unwilling to conduct the extensive research experts advise,” Roper said. “Rather than continuing to swim against the stream of what investors are willing to do, we should consider how we can both develop education materials that better focus investors on the key issues that are likely to be most important to them based on their purchase method and ensure that disclosure documents make that information easily accessible and understandable.”

Use of the Internet

As they explore ways to improve the effectiveness of fund disclosures, regulators and others have increasingly looked to the Internet as a means of accomplishing that goal. “The survey offers a mixed message of hope and caution for those who see the Internet as the ultimate means of providing effective disclosures at relatively little expense,” Roper said.

- On the one hand, the survey found that the vast majority of investors have access to the Internet and would be willing to use it for at least some mutual fund purchaserelated activities. Among current owners, 87 percent of workplace purchasers, 80 percent of direct purchasers, and 73 percent of those who purchased most of their funds through a professional indicated that they would be willing to use the Internet in some fashion.

- Current fund owners expressed greatest willingness to use the Internet to obtain general information about mutual funds (66 percent), to research individual funds (65 percent), and to receive periodic reports and documents from a financial services professional (56 percent).

- Those who identified themselves as future fund owners, a younger population, expressed even greater willingness to use the Internet than current owners. Three quarters (74 percent) indicating they would use the Internet to obtain general information about mutual funds and research individual funds. More than two-thirds (67 percent) said they would use an Internet-based cost calculator; 63 percent said they would use the Internet to receive period reports and documents, and 56 percent said they would do so to communicate with their financial services professional.

However, the survey also revealed a widespread reluctance to use the Internet among certain groups and for certain purposes.

- More than two in ten survey respondents (a group that includes both investors and non-investors) and 16 percent of current fund owners indicated they would not use the Internet at all.

- This lack of willingness to use the Internet was particularly marked among investors 65 and older. The survey found a consistent and significant drop-off in willingness to use the Internet after age 65 for each type of use listed except fund purchase, which had strong negatives across virtually all age groups

- Even among the youngest three groups of survey respondents, significantly fewer were willing to use the Internet to communicate with a financial services professional or to purchase funds than for other purposes.

- Among current investors who purchased most of their funds from a financial services professional, fewer than half indicated they would be willing to receive periodic reports or disclosure documents over the Internet for the funds they own, and just over one third indicated they would be willing to use the Internet to communicate with their financial services professional.

“While the Internet holds great potential to improve mutual fund disclosures, these findings suggest to us that we must proceed with caution,” Roper said. “Before we forge ahead with proposals to provide information primarily in an electronic format, we would do well to learn more about the reasons behind investor reluctance to use the Internet and the intensity of that reluctance and to explore what factors may help to overcome that reluctance. In addition, we must ensure that those who either do not have ready access to the Internet or who are not comfortable with its use are not forced to overcome new barriers in order to continue to receive documents in their preferred printed format.”