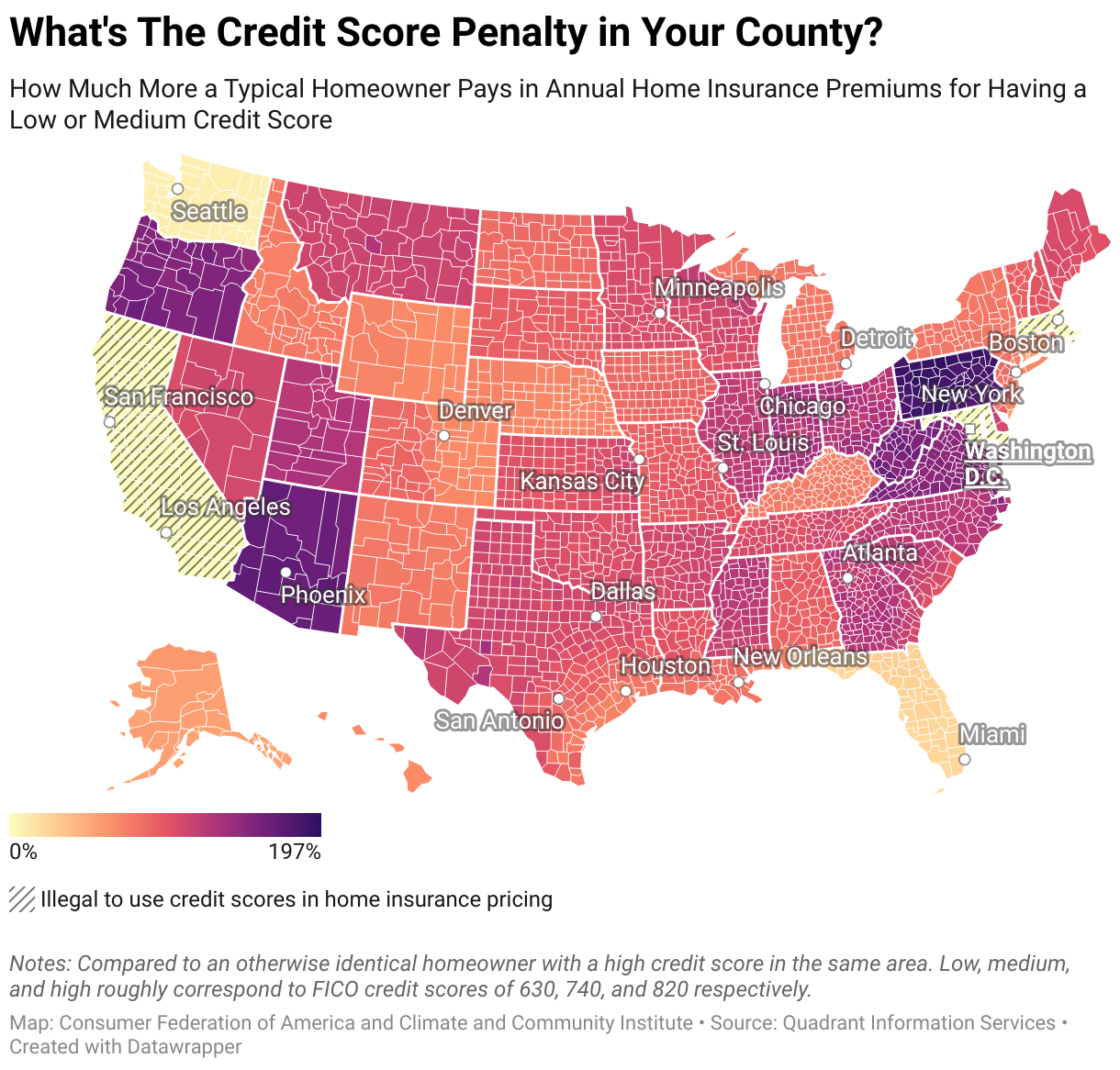

Washington, D.C. – A typical homeowner with a “low” credit score will pay nearly $2,000 more each year – or almost double the price – for their insurance premiums than their otherwise identical neighbor with a “high” credit score, according to Penalized: The Hidden Cost of Credit Score in Homeowners Insurance Premiums, a report issued today by the Consumer Federation of America (CFA) and Climate and Community Institute (CCI). The report, which calculates premiums for a typical homeowner in virtually every ZIP code in the United States, also found that it was more expensive to have a low credit score than to live in an area with high disaster risk. Average premiums for homeowners with low credit scores who live in areas with little risk of natural disasters were often higher than those for high credit score homeowners who live in high-risk communities. The report was released in conjunction with a working paper with a detailed technical analysis of the data by Dr. Nick Graetz, Assistant Professor of Sociology at the University of Minnesota and Fellow with the Climate and Community Institute.

The groups said that the skyrocketing cost of homeowners insurance is unfairly compounded for people who maintain safe homes but have credit scores that are average or worse. The report showed that even homeowners with medium credit scores -roughly equivalent to a 740 FICO score – pay an extra $792 per year, or 39 percent more, compared with otherwise similar customers who have high credit scores.

“Your credit score shouldn’t determine whether you can afford to insure your home,” said Sharon Cornelissen, Director of Housing at CFA and co-author of the report. “Homeowners who have done everything right – kept up their homes, avoided claims – are still getting hit with higher premiums just because of their credit scores. Combined with years of skyrocketing premiums, this pricing practice is pushing the dream of homeownership ever further out of reach for millions of Americans, especially younger buyers and families of color.”

Insurers claim that the price of premiums provides an effective and efficient signal to people about their climate risk and the need to mitigate that risk. These findings, however, demonstrate that insurers themselves obscure these supposed signals with the use of other — potentially discriminatory — variables in setting premium prices.

“The insurance industry is gaslighting us when it says they price homeowners insurance policies to reflect climate risk,” said Moira Birss, Senior Fellow with the Climate and Community Institute. “Climate change is driving dramatic changes that demand an honest assessment of risk and housing, but instead of proactively helping to reduce the risks the insurance companies are penalizing poverty.”

Pointing to the importance of homeowners insurance and mortgage lenders’ requirement to purchase coverage, the groups said state lawmakers and regulators should move to end the use of credit scores in homeowners insurance pricing, as has already been done in California, Maryland, and Massachusetts. According to the research, which used data purchased from Quadrant Information Services, homeowners in Pennsylvania, Arizona, Oregon, and West Virginia face the largest penalty for having a low credit score. In 23 states, homeowners with low credit – a score roughly equivalent to a 630 FICO score – pay at least twice as much as counterparts with high credit scores (roughly 820 FICO).

Among the most surprising findings is the outsized impact of credit score compared with local disaster risk in how insurance companies price premiums. On average, a typical homeowner with a low credit score in the safest part of the country (in the first percentile of disaster risk) can expect to pay the same as an otherwise identical homeowner with a high credit score who lives in a much riskier area (the 71st percentile of disaster risk). This means that it is often more expensive to have a low credit score than to live in an area with a high disaster risk.

“Charging more for having a low credit score than living in a high-risk community shows what the insurance companies truly value,” said Douglas Heller, CFA’s Director of Insurance. “The insurance industry says that increasing climate risk is driving premiums, but, actually, they slice and dice the market to make folks with low credit scores living in lower risk communities subsidize the price of the higher credit score customers the insurance companies prefer.”

The groups are calling on lawmakers and regulators to:

- Prohibit insurers from using credit scores and credit history in pricing homeowners insurance; and

- Require insurance companies to file public disclosures that provide greater transparency on their pricing models.