Homeowners across America are seeing higher homeowners insurance premiums every year. These rising bills are straining budgets, forcing people to make difficult decisions about downgrading their coverage or even forgoing insurance altogether.

To solve any problem, the first step is an honest look at accurate data. But for years, insurance companies hardly made any information on their prices, claims, and coverage public. After petitions from consumer advocates, the National Association of Insurance Commissioners (NAIC) and the Federal Insurance Office (FIO) were supposed to address this gap with their data release earlier this year. But the release had a major flaw: participation from state insurance departments was voluntary.

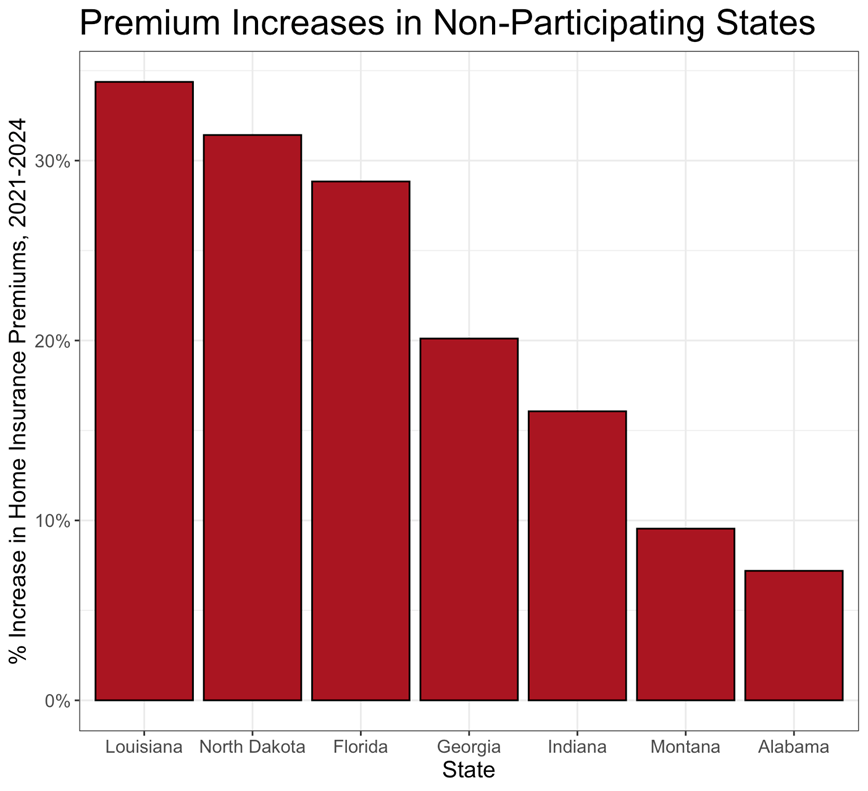

And unfortunately at least seven states did not participate in the data call: Florida, Alabama, Louisiana, Georgia, Indiana, Montana and North Dakota. This means that the data does not contain any information from insurance companies headquartered in these states, making researchers and advocates unsure of how to interpret the data and reach conclusions about rising costs. By refusing to participate in this data call, the Insurance Commissioners in these states have let down the policyholders they are supposed to protect.

To address this lack of data, we and our co-authors at the Consumer Federation of America (CFA) released a new report measuring rising home insurance premiums from 2021 to 2024 in nearly every ZIP code in the country. To make this report possible we had to spend tens of thousands of dollars on purchasing data from a private company. It should not be so expensive for consumer advocates just to measure the premium increases affecting everyday homeowners.

The results of our analysis were alarming: the typical homeowner in the United States saw their annual premiums rise by $648 from December 2021 to August 2024 to an annual average of $3,303. This is equivalent to a 24% increase, well above the (historically high) 13% inflation over the same period. Homeowners insurance became much more expensive in almost every ZIP code across the United States, not just in coastal states like Florida and California.

The seven states that did not participate in the data call were no exception to these trends. Premiums increases by an average of 23% in these states (weighting by the number of homeowners), increasing from an annual average of $4,975 to $6,249. The non-participating state with the largest increase was Louisiana (34%) and five of the seven states experienced increases greater than the rate of inflation.

Source: Consumer Federation of America

Source: Consumer Federation of America

It’s possible that these steep increases occurred because some of these states—especially in the southeast—have a higher vulnerability to climate change. However, without more information it is impossible to know for sure—and that is why consumers and policymakers need the data.

What should be done about these surging costs? Our report offers a range of recommendations, including stronger oversight by state regulators when companies want to hike premiums, and investing more in risk reduction (such as offering grants to homeowners to fortify their roofs). However, our primary policy solution is simple: make insurance data public and easily accessible.

The National Association of Insurance Commissioners has tentative plans to make their data collection and release a regular occurrence. They must do this because the increase in insurance premiums shows no sign of slowing down. Tariffs are rocking the economy and seem certain to increase construction costs, while climate change is making once-in-a-generation storms much more frequent. We cannot measure the insurance affordability crisis without accurate and reliable numbers. The next time a data call on homeowners insurance is issued, all states owe it to their citizens to participate.