37th Annual Financial Services Conference

December 11 & 12, 2024

Wednesday, December 11

9:00 am

Welcome

Speaker

Susan Weinstock

CEO

Consumer Federation of America

Adam Rust

Director of Financial Services

Consumer Federation of America

9:05 am

BANK MERGER REVIEW REFORM

Bank merger review guidelines require evidence that mergers benefit consumers. However, no federal banking agency has rejected an announced bank merger application in almost twenty years. Last year, an application to merge two large credit card issuing banks prompted concerns about a withering away of competition. In January 2024, the prudential regulators issued a proposed rulemaking to update bank merger review procedures. Bank merger review is one touch point of the larger effort in the Biden Administration to revisit anti-trust, but because of the unique nature of banking, there are considerations that are unique to this industry. There are four components to merger reviews: impact on competition, the needs and conveniences of the public, managerial controls, and systemic risk. Attend this panel to hear a debate on how and if the bank merger review process should be updated.

10:30 am

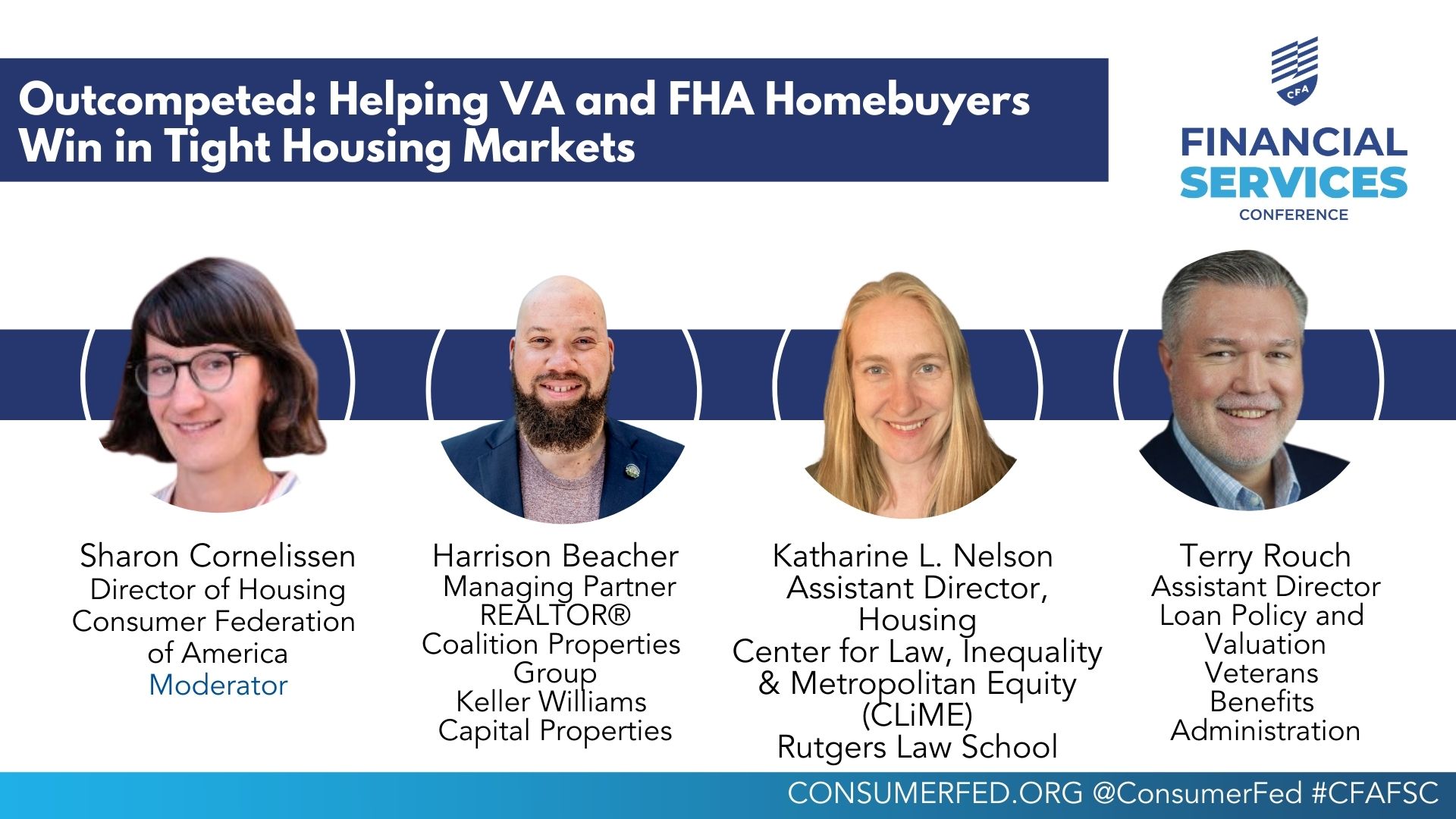

OUTCOMPETED: HELPING VA AND FHA HOMEBUYERS WIN IN TIGHT HOUSING MARKETS

Housing unaffordability continues to be at the top of the agenda. Amidst persistent housing supply shortages and stiff competition, homebuyers often compete in bidding wars to win their chance at homeownership. A troubling pattern has emerged: homebuyers using an FHA or VA mortgage unfairly lose out, and face stigma, even if they make the highest bid. Many first-time homebuyers rely on Federal Housing Administration and Veterans’ Affairs government-insured mortgages, which were meant to help level the playing field, but today too often find themselves blocked out. This panel looks closely at how common bidding wars and overbidding remain in today’s markets, and how they may shape unequal opportunity. We discuss a range of legislative and policy proposals – in the FHA and VA programs, in legal homebuyers protections, and through Realtor education – and how they may help tilt opportunity towards less well-off consumers. We will debate what a fair homebuying marketplace

looks like and how to best balance the presence of cash buyers and investors, with opportunity for first-time homebuyers.

12:30 pm

LUNCHEON KEYNOTE ADDRESS: AN UPDATE ON THE ECONOMIC STATE OF AFRICAN AMERICANS AND OTHER UNDERSERVED URBAN RESIDENTS

Speaker

Marc Morial

President and CEO

National Urban League

1:15 pm

A FIRESIDE CHAT WITH BARBARA ROPER, SENIOR ADVISOR TO THE CHAIR, SECURITIES AND EXCHANGE COMMISSION

1:40 pm

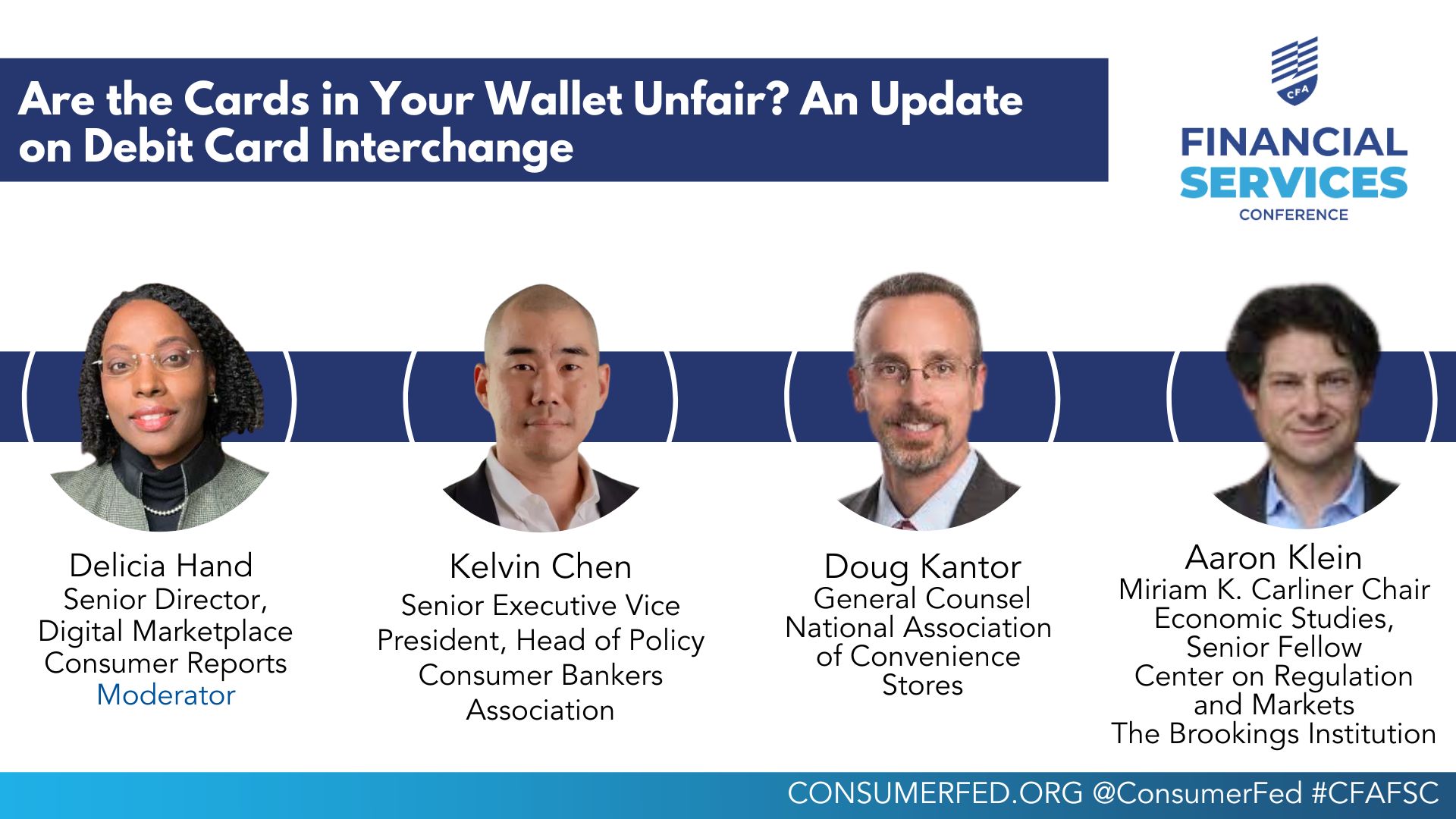

ARE THE CARDS IN YOUR WALLET UNFAIR? AN UPDATE ON DEBIT CARD INTERCHANGE

The Fed has a new proposal to lower interchange on debit cards. Regulation II says interchange costs should be close to the cost of processing payments. Given that costs for processing payments have fallen in the last decade, the Federal Reserve intends to lower the permitted interchange rate for large banks with assets of more than $10 billion. Perspectives differ on the impact of applying caps to interchange fees. Banks are sending messages that reduced debit swipe fees will impact their ability to provide basic bank accounts. From the perspective of retailers, lower interchange would lead to lower operating costs for retailers. This panel will focus on how the rule could impact consumers.

3:00 pm

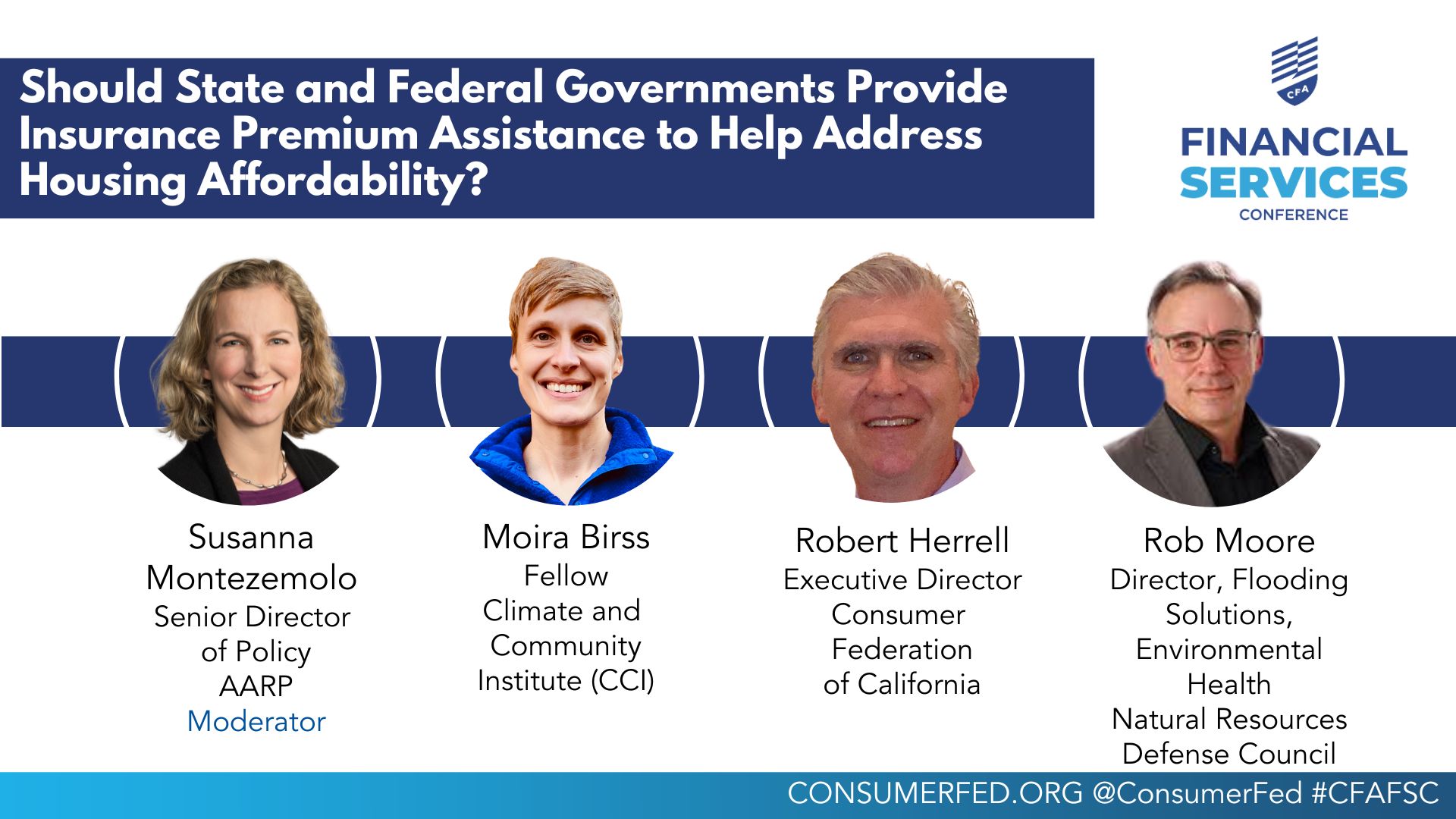

SHOULD STATE AND FEDERAL GOVERNMENTS PROVIDE INSURANCE PREMIUM ASSISTANCE TO

HELP ADDRESS HOUSING AFFORDABILITY?

As homeowners, affordable housing developers, and property owners face unprecedented increases in insurance premiums, policymakers and housing and consumer advocates are looking for new strategies to help lower-income homeowners stay in their homes and affordable housing entities continue to build and maintain the housing units needed to serve low- and moderate-income Americans. One strategy that has been discussed in recent years would provide taxpayer-funded assistance to lower-income homeowners and owners of affordable housing to cover a portion of property insurance premiums, which have increased by more than 50% in recent years. Panelists will discuss how such a program might be implemented and concerns about this approach to addressing rising insurance costs, including the possibility that it could encourage moral hazard and building in high-risk areas and that it might result in taxpayer subsidies of overpriced coverage.

4:00 pm

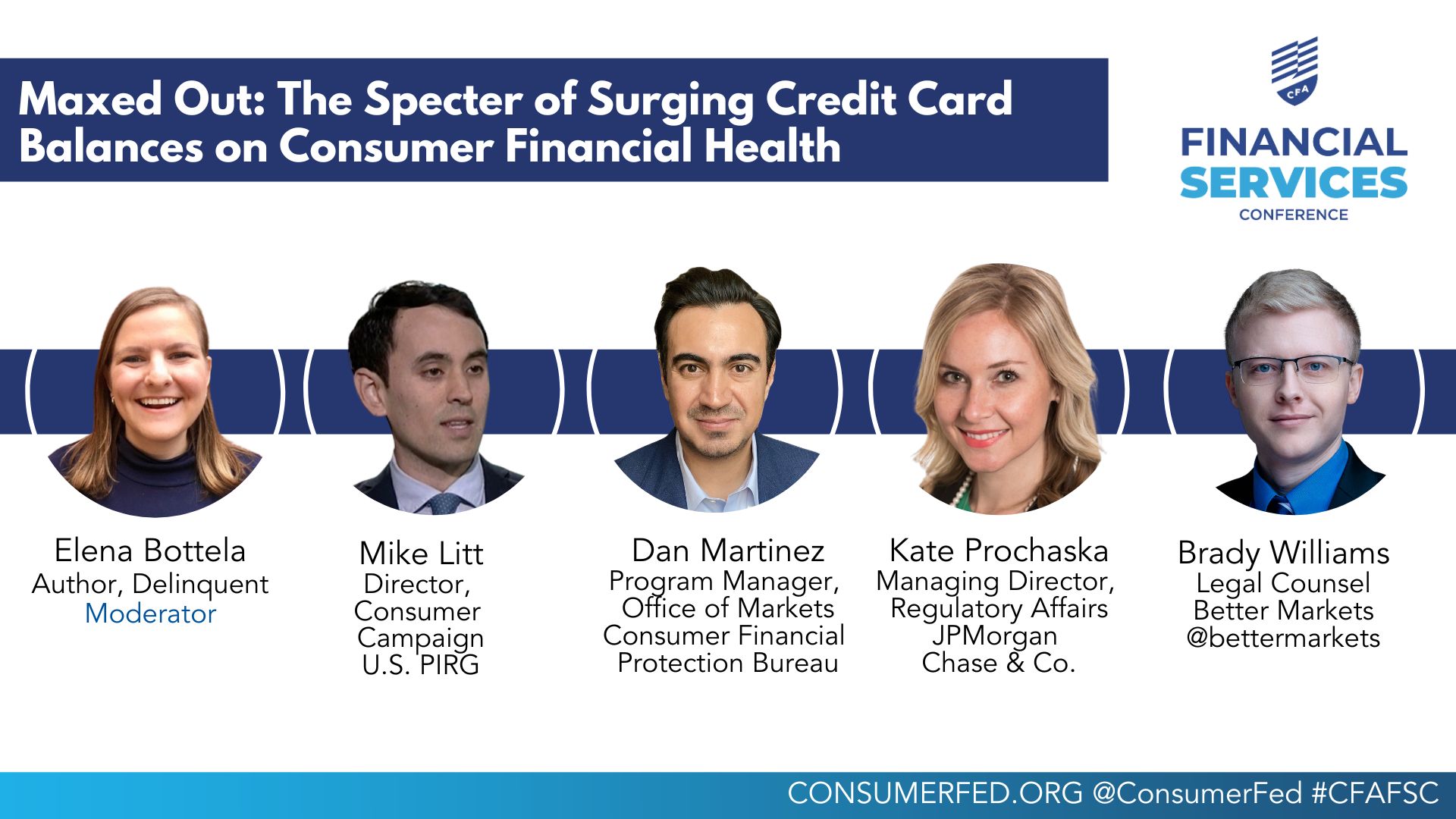

MAXED OUT: THE SPECTER OF SURGING CREDIT CARD BALANCES ON CONSUMER FINANCIAL HEALTH

Earlier this year, total consumer credit card debt surpassed $1 trillion. CFPB research has revealed that the margin between the cost of funds and prevailing credit card interest rates has grown steadily. Approximately 15 banks issue 85 percent of all cards. These issuers charge higher interest rates than less popular cards, underscoring a lack of meaningful competition. In 2022, consumers paid $105 billion in interest and $14.5 billion in late fees. Regulators and legislators have shown interest in addressing these issues. Earlier this year, the CFPB finalized a rule to reduce late fees. In the Senate, legislators from both parties have introduced bills to cap credit card interest rates. In this panel, experts will discuss the implications of credit card debt on households and the economy and consider options to correct this market.

5:00 pm

CLOSING KEYNOTE ADDRESS: TRUMP TAKE TWO

Speaker

Mark Zandi

Chief Economist

Moody’s

Thursday, December 12

9:00 am

Welcome

Speaker

Susan Weinstock

CEO

Consumer Federation of America

9:05 am

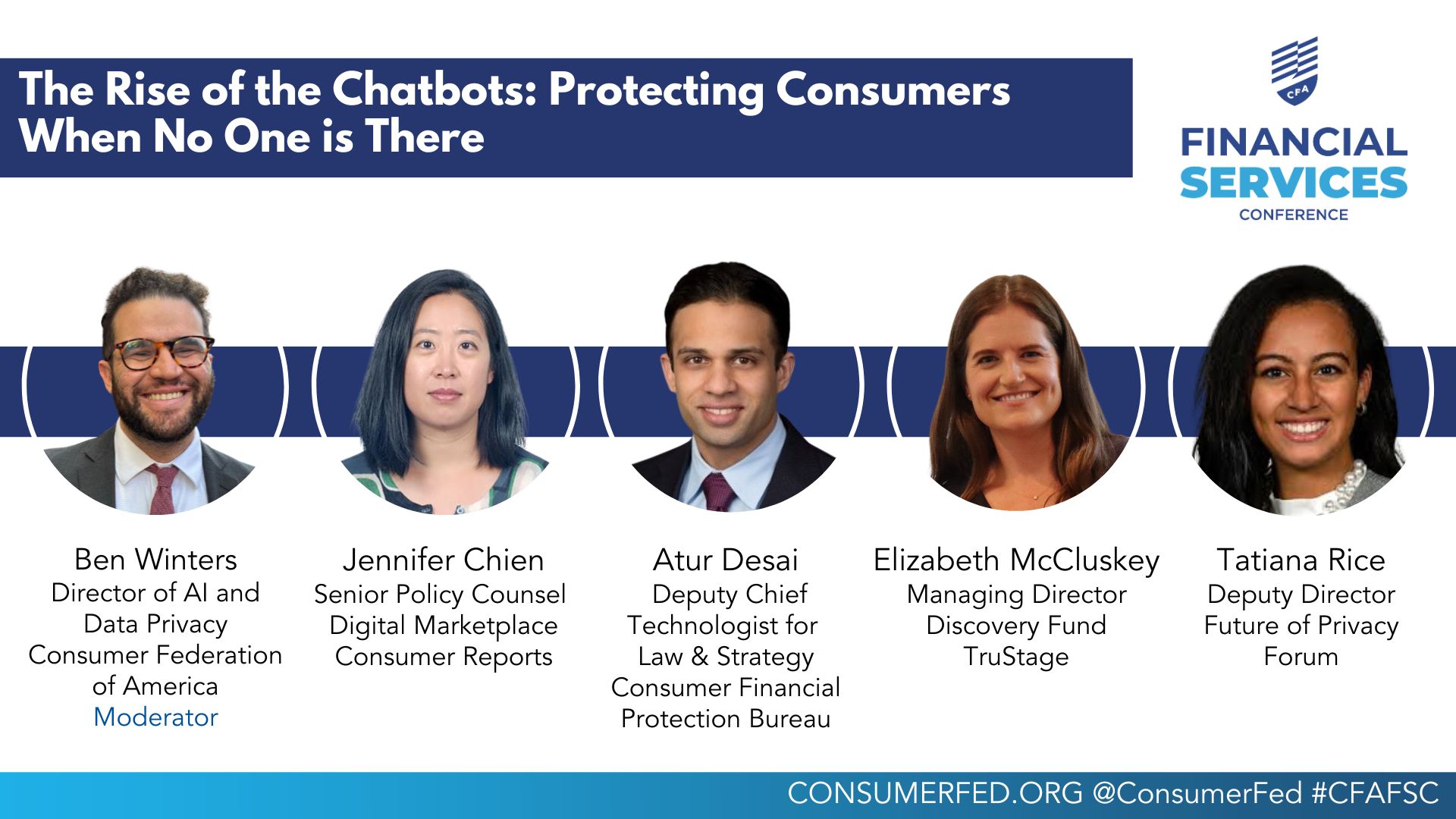

THE RISE OF THE CHATBOTS: PROTECTING CONSUMERS WHEN NO ONE IS THERE

Consumers expect a timely and well-informed response when they engage with financial institutions to resolve a problem. Increasingly, communications between consumers and their financial services providers will be conducted through chatbots. Their adoption is being driven by cost savings for banks, but what impact is it having on consumers? A 2023 report from the CFPB found that all ten largest banks have deployed chatbots and that almost 100 million consumers had interacted with one. In the last year, financial service providers have gone from using simple rule-based chatbots that only generate pre-approved answers to ones that use large language models and develop responses with generative AI. While chatbots may be useful for simple interactions, they may be poorly suited to resolve complex problems and not work equally well for all consumers. Adverse outcomes could erode consumer trust if models provide incorrect information, fail to solve a difficulty, or impede access to a real customer service person. In some cases, their performance could violate consumer protection laws, reveal private information, and make consumers vulnerable to scammers. This panel will explore the consumer

protection issues raised by chatbots and the crucial need to identify and implement potential means to address them.

10:30 am

KEYNOTE ADDRESS

Speaker

Julia Barnard

Private Education Loan Ombudsman

Consumer Financial Protection Bureau

11:00 am

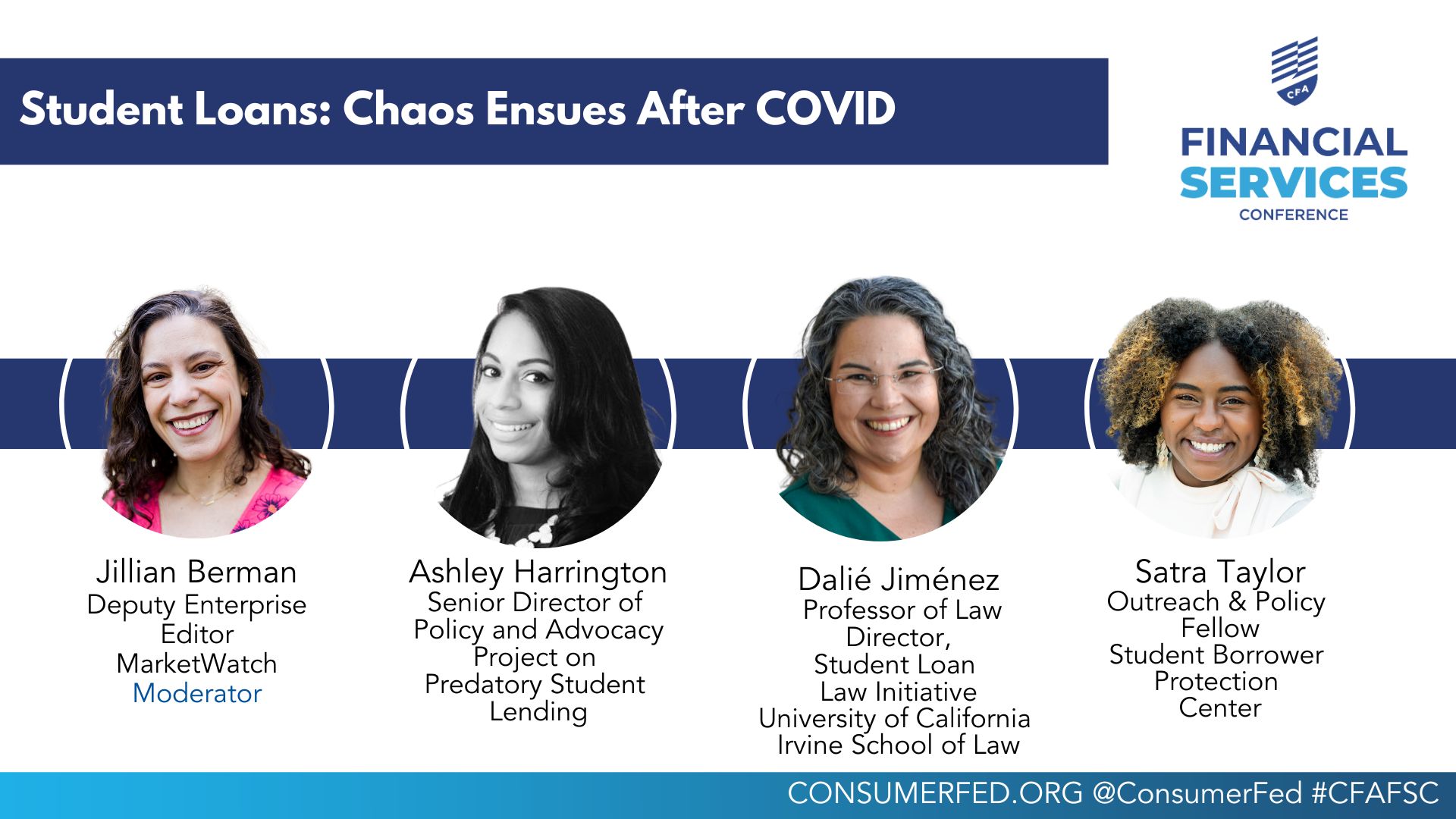

STUDENT LOANS: CHAOS ENSUES AFTER COVID

During COVID, the Administration took steps to help student loan borrowers, but those protections are ending. Several student loan borrower protections lapsed, affecting the financial lives of 43 million borrowers with $1.7 trillion in debt. Starting on October 1st, borrowers who continue to not make payments will become delinquent on their loans and will be reported to credit agencies and default 270 days after their missed payment. Going forward, consumers struggling to make payments must proactively apply for relief. However, many borrowers have reported difficulties in filing applications through online portals and evidence reveals failures by loan servicers to honor income-based-repayment plans. State Attorneys General have successfully filed for an injunction on parts of plans to implement the Saving on a Valuable Education Act (SAVE), which would have lowered payments and provided long-term debt relief to some borrowers. In September, the CFPB banned repeat offender Navient from further participation in the servicing of federal student loans and Federal Family Education Loan Program loans. Simultaneously, legislators are proposing bills to provide relief for borrowers. This panel will provide real-time updates to a market that is rapidly changing.

Download Program

Download Speaker Biographies

A message from National Urban League’s President and CEO Marc Morial

A message from Moody’s Chief Economist Mark Zandi

37th Annual Financial Services Conference

Advisory Committee Members

AARP

American Bankers Association

American Express

Bank of America

Broadridge Financial Solutions, Inc.

CFP Board

Consumer Bankers Association

FINRA

Independent Community Bankers of America

JPMorgan Chase & Co.

National Association of Convenience Stores

TruStage

Walmart

Zillow Group