Washington, D.C. – As the House Education and Workforce Committee held a hearing today on “Principles for Ensuring Retirement Advice Serves the Best Interests of Working Families and Retirees,” a new analysis from Consumer Federation of America (CFA) demonstrates that none of the major financial industry alternatives to the Department of Labor conflict of interest rule meet these basic principles. “Of all of the proposals that have been offered, the DOL proposed rule is alone in meeting this basic standard of ensuring that retirement investment advice serves the best interests of the recipients of that advice,” said CFA Director of Investor Protection Barbara Roper.

A bipartisan group of House Members have said they plan to sponsor legislation based on this and other innocuous sounding principles in order to fix problems with the Department of Labor rule proposal. Predictably, industry lobbyists testified in enthusiastic support of that effort at today’s hearing. “Members should ask themselves why groups that have clearly demonstrated their interest in preserving the status quo are now coming out in full-throated support for a ‘legislative fix,’” said CFA Financial Services Counsel Micah Hauptman. “The answer is clearly that their preferred ‘fix’ will achieve their goal of a best-interest standard in name only, to the detriment of Members’ constituents who are saving for retirement.”

The CFA analysis identifies two key factors that any proposal must meet if it is to provide the assurance that retirement advice serves the best interests of working families and retirees:

- The best standard must apply to the full range of services perceived and relied on as objective investment advice by retirement savers.

- And, to ensure that it is not a best interest standard in name only, it must be backed by restrictions on compensation and other practices that encourage and reward advice that is not in the customer’s best interests.

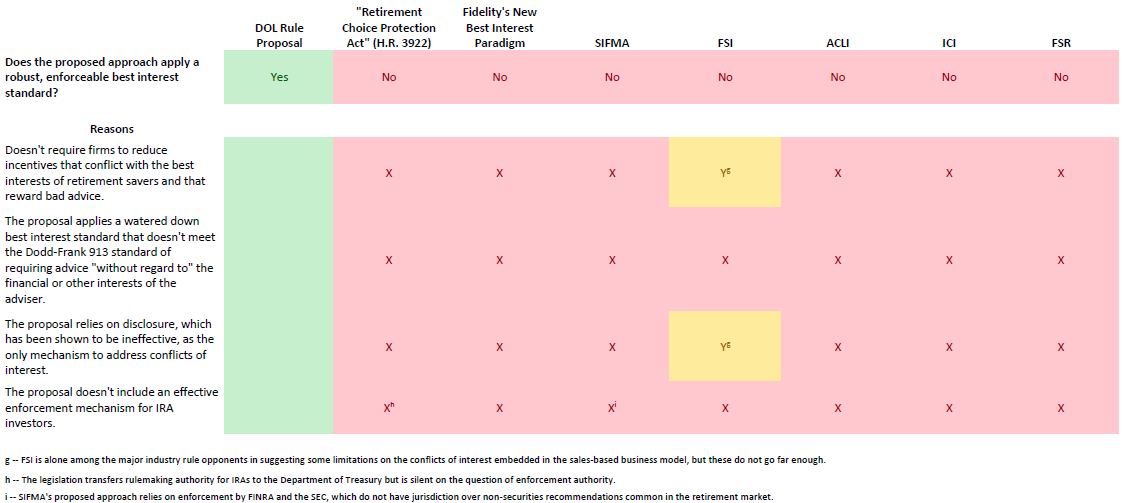

CFA analyzed alternative proposals put forward by the leading industry opponents of the DOL rule to see how they measured up against these standards. While each of the alternative proposals takes a slightly different approach, all fall well short on both these key points. (See chart.)

On the crucial issue of whether the proposals cover the full range of retirement investment advice services, Roper said, “Either the proposals retain existing loopholes that allow the firm to use disclaimers to evade the best interest standard, or they provide a broad seller’s carve-out, which deprives retirement savers of protection when the conflicts are greatest, or they allow the firm to contract out of its fiduciary obligations. At best, these alternatives would preserve the status quo, but some go further by expanding the existing loopholes that allow financial firms and their ‘advisors’ to evade their fiduciary obligations.”

None of the proposed alternatives take meaningful steps to address the toxic conflicts that pervade the business models of many financial firms, she added. “Instead of reining in conflicts, they rely exclusively on disclosures to manage conflicts, an approach that has been shown to be ineffective.” The principles outlined by Representatives Peter Roskam (R-IL) and Richard Neal (D-MA) appear to suffer from the same basic short-coming, she said.

In contrast, the Department of Labor’s proposed conflict of interest rule both covers the full range of services workers and retirees rely on for retirement investment advice and backs its best interest standard with real restrictions on common industry practices that encourage and reward harmful advice. As such, it alone fulfills this basic principle of ensuring that retirement advice serves the best interests of working families and retirees that the Roskam-Neal principles purport to advance.

“Lawmakers who are sincere in wanting to ensure that retirement advice meets this principle should throw their support behind the DOL effort and oppose any policy riders to delay, defund, or otherwise interfere with the DOL rulemaking process,” Hauptman added.

The Consumer Federation of America is a national organization of more than 250 nonprofit consumer groups that was founded in 1968 to advance the consumer interest through research, advocacy, and education.