Black and Hispanic Homeowners Pay Hundreds of Dollars More Annually for Homeowners Insurance

“Racial Premium Gap” Adds Up to $15,000 in Additional Insurance Costs for Black Consumers and $28,500 for Hispanic Consumers Over a 30-Year Mortgage

WASHINGTON, D.C. — Black and Hispanic consumers pay hundreds of dollars more on average each year in homeowners insurance premiums, according to Redlined: The Persistence of Racial Inequality in the Cost of Homeowners Insurance, a new report issued today by the Consumer Federation of America (CFA).

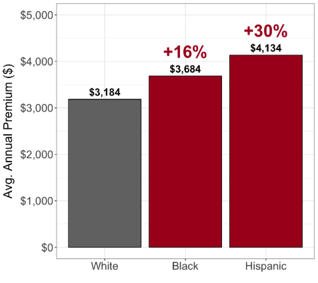

The report, which examines homeowner insurance premiums and racial demographics in every ZIP code in the United States, found evidence of a substantial racial premium gap—a major upcharge for certain consumers. On average, homeowners in Black communities pay a 16% higher premium, or $500 more per year, compared to homeowners in white communities. Homeowners in Hispanic communities pay a 30% higher premium, or $950 more per year, compared to homeowners in white communities. Over a 30-year mortgage, this gap results in at least $15,000 in additional insurance premiums for Black homeowners and $28,500 in additional premiums for Hispanic homeowners.

“Black and Hispanic homeowners are being unfairly charged higher premiums for their home insurance coverage,” said Sharon Cornelissen, Director of Housing at CFA and a co-author of the report. “This racial premium gap hurts their ability to afford housing, to become homeowners, and to build generational wealth.”

“Insurance companies should be changing their pricing models to end the redlining-by-overcharging that we see in the data, but since they seem unwilling to self-correct, state regulators should be stepping in to demand change," said Douglas Heller, CFA’s Director of Insurance and co-author of the report. “Buying insurance is required of every homeowner with a mortgage, which creates a special obligation on policymakers to scrutinize this market. But this pattern of racial discrimination by insurance companies has not gotten the scrutiny it needs from the lawmakers and insurance commissioners who are supposed to protect consumers and communities.”

“Hispanic households fueled the nation’s net homeownership growth last year," said Cristy Villalobos-Hauser, Housing Policy Advisor at UnidosUS. “At a time when housing affordability remains a top concern, Hispanic homeowners are paying disproportionately higher homeowners insurance premiums compared to their neighbors. Rising insurance costs threaten housing stability, undermine wealth-building, and make it harder for families to achieve the promise of sustainable homeownership. UnidosUS commends CFA for highlighting these disparities and urging policymakers, regulators, and insurers to reform the insurance market to be more fair, transparent, and affordable, so that all families can continue to build wealth regardless of their Zip code.”

The report controls for various factors and shows that this gap is not explained by differences in the characteristics of homeowners, their home, or what people opt to insure. Even after accounting for a wide range of factors that shape insurance risk and that are commonly used by insurance companies, homeowners in Black communities still pay a 10% higher premium on average, and homeowners in Hispanic communities pay an 11% higher premium on average.

Based on our analysis, the racial premium gap is larger in certain states, meaning that homeowners in Black and Hispanic communities can pay thousands of dollars in additional insurance costs. The Black premium gap is especially large in Michigan, where homeowners in predominantly Black neighborhoods are charged on average $1,768 a year more, or 74% more, for the same coverage. And Florida has the largest Hispanic premium gap: homeowners in predominantly Hispanic neighborhoods are charged 58% more—an average of $5,014 more each year—for the same insurance coverage when it is offered to homeowners in predominantly white ZIP codes.

The study concludes with three policy recommendations:

- First, states should enforce fair housing laws regarding insurance companies and require regular company testing and disclosures to prevent disparate impacts—disproportionate harm to certain groups of consumers.

- Second, states should prohibit insurers from using ZIP code or smaller geographic territories when setting premiums.

- Third, insurance companies should make their transaction-level homeowners insurance data public every year in a manner similar to the Home Mortgage Disclosure Act (HMDA) Database.