Major Insurance Companies Raise Premiums After Not-At-Fault Accidents

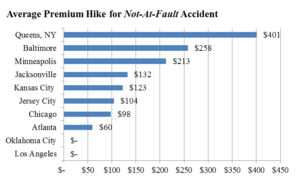

Washington, D.C. – Safe drivers who are in accidents caused by others often see auto insurance rate hikes, according to research released today by Consumer Federation of America (CFA). The research analyzed premium quotes in 10 cities from five of the nation's largest auto insurers. Among the cities tested, drivers in New York City and Baltimore pay out the most for doing nothing wrong, and customers in Chicago and Kansas City also face average increases of 10% or more when another driver crashes into them.

"Innocent drivers who don't cause accidents should not be charged more because someone else hit them," said J. Robert Hunter, CFA's Director of Insurance and the former Insurance Commissioner of Texas. "Most people know that if they cause an accident or get a ticket they could face a premium increase, but they don't expect to be punished if a reckless driver careens into them."

CFA called on lawmakers around the country to prohibit such penalties on innocent drivers. “Penalizing safe drivers hit by another car is not only very unfair; it also discourages them from filing legitimate claims,” said Hunter. “Lawmakers and regulators need to protect consumers from being punished when they’ve done nothing more than use the policy they have already paid for.”

At least two states already prohibit such penalties. While drivers in eight of the 10 cities tested by CFA can be surcharged if they are hit by another driver, CFA research found that consumer protections in California and Oklahoma prevent insurance companies from raising rates on drivers in those states when they are involved in an accident that was not their fault.

Some Companies More Unfair Than Others

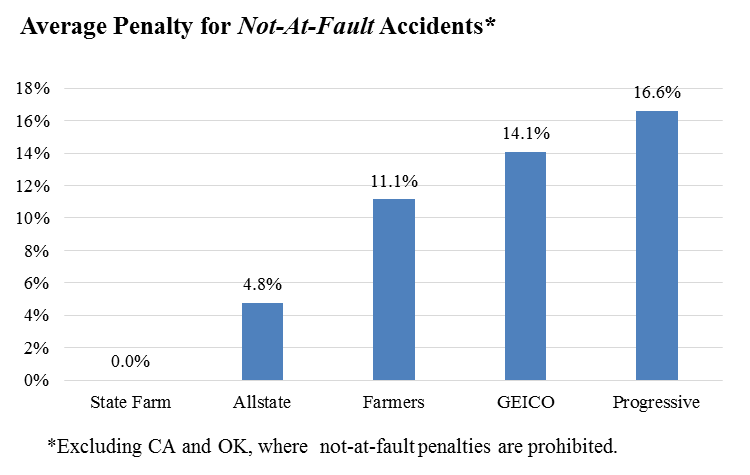

There are significant differences in the way the five companies CFA tested treat customers after accidents they did not cause. Progressive used the not-at-fault penalty most aggressively, surcharging drivers in every test where such an increase is not prohibited by state law. GEICO and Farmers sometimes raised rates by 10% or more for not-at-fault accidents. Allstate occasionally penalized drivers who did not cause the accident, while State Farm never increased premiums for these accidents.

Being Hit by Another Motorist Costs More for Lower Income Drivers

The increases charged for not-at-fault accidents vary from customer to customer even for the same company in the same city. CFA's research over recent years has consistently found that good drivers with certain socio-economic characteristics that suggest lower incomes generally pay more for auto insurance than higher-income drivers with the same driving record. This pattern holds when it comes to penalizing drivers for accidents in which they were not at fault.

Comparing two good drivers, whose only differences reflected their individual socio-economic circumstances rather than their driving safety record, CFA found the following:

- Higher-income drivers paid $78 more on average after a not-at-fault accident;

- Moderate-income drivers paid $208 more on average after a not-at-fault accident;

- Higher-income drivers faced a 6.6% penalty on average after a not-at-fault accident;

- Moderate-income drivers faced a 9.6% penalty on average after a not-at-fault accident.

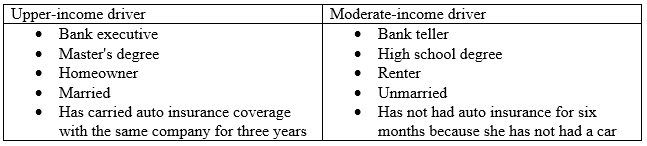

To test for the differing impact related to economic status, CFA sought quotes for two female drivers in each city who lived at the same address, were 30 years old, licensed for 14 years, and drove a 2006 Toyota Camry 10,000 miles each year. The drivers differed only in personal characteristics that are correlated with income, as described below:

Premium Hikes for Not-At-Fault Accidents Adds to the Unaffordability of Auto Insurance Identified by Recent Federal Insurance Office Study

More than 18 million residents living in 845 ZIP codes across the country face basic auto insurance premiums that have been deemed unaffordable by the United States Treasury Department’s Federal Insurance Office (FIO). For drivers living in states where insurance companies can charge more for not-at-fault accidents, some good drivers find premiums even further out of reach, despite having done nothing wrong.

The FIO report, released in its first Auto Affordability Study in January and available here, calculated the average premium charged to drivers in underserved ZIP Codes across the country for state minimum limits liability insurance, the insurance coverage required in every state but New Hampshire. More than 18 million Americans live in ZIP codes where the average premium for basic insurance is more than 2% of the median household income in that community. Because most drivers have not been involved in a recent accident, the average premiums identified in the study are lower than the actual premiums drivers are likely to face when insurance companies penalize them for having been hit by another driver who caused an accident. That would leave auto insurance even more unaffordable for many good drivers who are already struggling to comply with state insurance mandates.

“We already have a severe problem in this country, because so many Americans live in communities where auto insurance is unaffordable,” said Douglas Heller, an insurance expert who conducted the research along with CFA’s Michelle Styczynski. “State leaders should at least prevent insurance companies from punishing good drivers for having the bad luck of being in the vicinity of someone else’s bad driving.”

What Consumers Can Do to Protect Themselves from This Unfair Practice

Consumers uncertain about whether their company would charge them for not-at-fault accidents in their state should ask their insurance agent or insurance company and, if they learn they would be surcharged, inform the agent they believe the practice to be very unfair. Also, inform the agent or insurer that you know State Farm does not use such surcharges so their use is not necessary for pricing. It would also help if consumers made the same inquiry of and complaint to their state insurance department.

“Diverse states such as Oklahoma and California have banned the practice,” noted Heller. “A little push from consumers could persuade other states to do the same.”

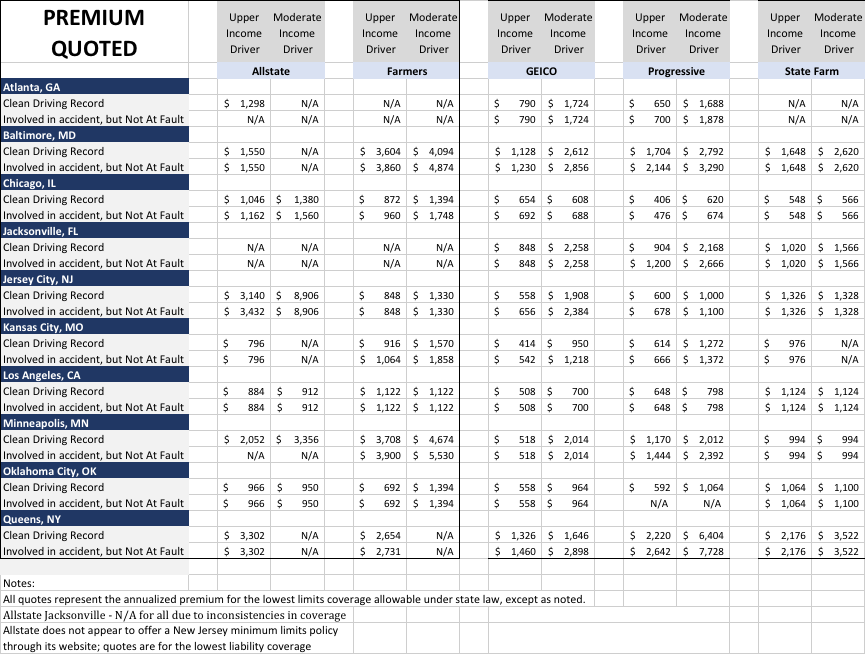

Appendix: Premium Quote Test Results

Contact: Bob Hunter, 703-528-0062; Doug Heller, 310-480-4170

The Consumer Federation of America is an association of more than 250 non-profit consumer groups that, since 1968, has sought to advance the consumer interest through research, education, and advocacy.